Rebalancing is a simple but oft-forgotten part of portfolio management. All the work done prior to reaching an asset allocation determination is undone if portfolios are left to the machinations of markets without review.

Today, pockets of insanity suggest there is merit in contemplating weightings to high risk asset classes and considering rebalancing towards lower risk asset classes and managers.

In this column, I will look at sequencing risk and the market’s present elevated valuations to ask whether there is merit in rebalancing portfolios towards funds that can capture more of the upside and less of the downside.

Where we’ve come from

In June 2019, The Reserve Bank of Australia’s Thomas Matthews published a paper entitled A History of Australian Equities in which the total return for all Australian shares between 1917 and 2019 was calculated as 10.2 per cent pa.

The long-term returns from Australian equities are remarkably similar to those of US equities. Russell E. Palmer Professor of Finance at the Wharton School of the University of Pennsylvania, Professor Siegel, has demonstrated that the annualised return from US Equities between January 1917 and January 2018 was 10.0 per cent pa with a standard deviation of 19.7 per cent pa. This compares to the 10.2 per cent pa return and 19.2 per cent pa standard deviation from Australian equities.

If the long run return from equities is around 10 per cent than any period during which returns are much higher should be followed by a period of lower returns, such that the long-term average is maintained. In other words, higher returns today are simply borrowing from the future.

This is relevant considering that between February 2016 to October 2019, the All ordinaries Accumulation index returned 16.72 per cent per annum, and between 21 December 2018 and 15 November 2019, the market returned 29.5 per cent.

If long term annual returns continue to average circa 10 per cent per annum, the recent period of higher returns should be followed by weaker numbers.

Today’s retirees need to think carefully about sequencing risk.

Sequencing Risk

Approaching retirement or have just entered it, a much more serious consideration of risk is required.

For retirees, regular withdrawals of capital may be required where income is insufficient to meet lifestyle requirement. And in an environment of ultra-low rates, generating a sufficient income is challenging. Consequently, restricted income means many investors must decide between spending less or eroding capital to meet spending demands. And when an investor is required to make regular withdrawals, regardless of the market level, capital losses experienced early in retirement can be extremely deleterious.

Sequencing risk, which describes the pattern of returns, or the order in which they are received, looms large for retirees. And when I talk of risk here, I am not only referring to a permanent loss of capital but also volatility.

The impact of sequencing risk on retirement incomes is the opposite to that on dollar cost averaging, which can be employed to accumulate wealth. This is because dollar cost averaging involves making regular investments, while retirees in pension phase are required to take regular payments from their investment portfolio.

Typical dollar cost averaging examples involve an investor investing a fixed sum of money at predetermined regular intervals. For example, $20,000 every month. By fixing the dollar amount for every investment, a discipline is forced upon the investor; when share prices are low, more units are acquired, and when share prices are higher fewer units are purchased. For the dollar cost averaging strategy, volatility becomes an investor’s best friend. As a net purchaser of shares, lower prices can be anticipated with eagerness.

The opposite however would be true for the retiree in pension phase, who is required to receive regular fixed dollar or percentage payments from their portfolio .

While sensible financial planning may involve the quarantining of some cash, to fund more immediate spending needs, from volatile assets, regular withdrawals are often ultimately required.

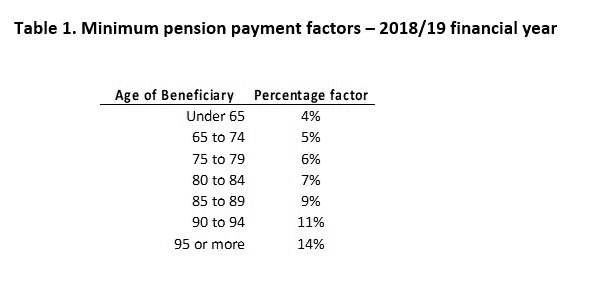

Table 1. Minimum pension payment factors – 2018/19 financial year

An investor, required to take fixed dollar withdrawals regularly from their portfolio, would experience the opposite of that which the dollar cost averager experiences. At lower prices, a retiree is forced to sell more units simply because more units are required to meet their minimum pension payment. After those units are sold, the remaining portfolio is smaller, and with fewer units, it becomes more difficult for the portfolio to recover to previous levels.

It is therefore essential that large losses or the risk of large losses, especially early in the investment journey, are avoided.

The Environment: Forgetting Risk

As a tidal wave of the world’s population enters retirement, a similar-sized avalanche of asset misallocations might be occurring. Just when retirees need their assets protected most, FOMO (the Fear of Missing Out) is resulting in the adoption of unacceptable risks. And thanks to sequencing risk, retirees adversely, and potentially permanently, altering retirement plans.

If you remember the early 90’s and Paul Keating’s recession we “had to have”, you’ll remember the aphorism ‘cash is king’. Fast forward nearly three decades and the pendulum of sentiment towards cash has most certainly swung to its opposite extreme. Today, cash, which earns less than two per cent per annum, is something that nobody wants. Cash has become a liability.

The consequence of investors’ cash ‘allergy’ has been the pursuit of higher returns and a migration into riskier assets such as property, profitless listed companies, private equity, venture capital and collectables such as art, cars and even low digit number plates. Even US$1.1 trillion of corporate bonds are trading at negative yields!

At the time of writing, one of history’s longest bull markets and most benign periods in terms of volatility has rendered the ‘migration trade’ both successful and confidence-building. But investors are forgetting two basic tenets of investing, and in the past, whenever these basics are rejected in the hope for better returns, the consequences have been painful.

The first tenet is; the higher the price you pay, the lower your return. The second is; when risk appears lowest, it is usually highest.

What to do? Rebalance

If it’s true that sequencing risk combined with the obligation to make super payments puts retirees at a greater risk of permanent capital loss, and if it’s true that there are pockets of irrational exuberance in markets today, advisers need to think carefully about rebalancing client portfolios away from higher risk asset classes or high risk subsectors of equities and towards lower risk, ‘stable-compounder’-type portfolios.

Alternatively there may even be merit in rebalancing away from fully invested index funds to active managers that have the flexibility to hold cash.

Clearly it makes sense, as it always has, to quarantine near-term financial needs from volatile assets. Advisers might, for example, suggest two or three years of spending needs are separated from volatile assets.

But there are also alternatives.

A million dollars invested for the last 27 years in the S&P/ASX 200 Accumulation Index has grown to $11.9 million but that would not be the experience of a retiree today who must make regular withdrawals from their portfolio.

A retiree who invested a million dollars today into an index fund that tracked the ASX 200 Accumulation index, and who experienced over the next 27 years the same pattern of returns as the last 27 years, would end up with a portfolio valued at $1.9 million after $10.1 million had been withdrawn through super payments (of course, no tax has been figured into these comparisons).

But a more conservatively managed fund, perhaps with the ability to hold cash, and one which captured more of the upside and less of the downside could produce a superior outcome.

We ran a model that captured just 80 per cent of the upside in any month that the market rallied, and only 60 per cent of the downside in any month that the market fell, and discovered a retiree would end up, after 27 years, with a portfolio balance of $2.6 million after taking out super payments of almost $13 million – a superior outcome to being 100 per cent exposed to the upside and downside vagaries of the market.

Elevated market prices suggest that sequencing risk is more relevant for retirees than it has been for many years. Advisers need to carefully consider the discipline of rebalancing and keep in mind that active management that emphasise capital protection and downside risk provides an important role in that rebalancing.

Leave a Comment

You must be logged in to post a comment.