Cheaper, lower-cost funds are outperforming their higher-priced compatriots, showing the higher fees are not correlated to higher returns, according to research from Morningstar.

The researcher released a report showing that across four asset classes – multisector growth, global large caps, Australian large caps and fixed income – funds in the lowest fee quintile achieved both higher success ratios and stronger average total returns than funds in the highest fee quintile.

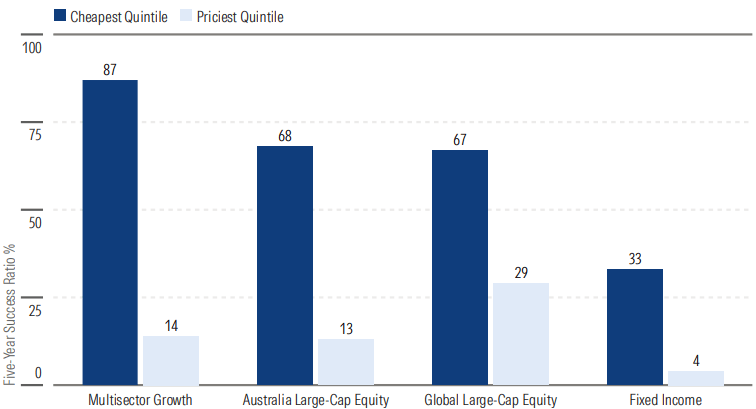

“This pattern can be clearly seen within Australian large-cap equities, where success ratios decline steadily as fees increase, indicating a simple yet consistent inverse relationship between costs and investor outcomes,” the Morningstar report says.

The divergence between the highest and lowest cost funds was most pronounced in the multisector growth category – funds in the cheapest fee quintile achieved a success ratio of 87 per cent, compared to 14 per cent for funds in the most expensive.

“This result is consistent with the well-documented difficulties active managers face in adding value through dynamic asset allocation, given the inherent challenges of reliably forecasting market regimes,” the report says.

“It was unsurprising that the most successful, lowest-cost quintile was dominated by multisector strategies employing significant passive components.

“By contrast, the weak outcomes observed among the most expensive funds were further exacerbated by the prevalence of secondary fund distributions encumbered by inefficient legacy fee structures.”

In the case of global large-cap equities, the researcher argued the results reflected a concentrated market dominated by the major US Silicon Valley tech providers.

Funds in the cheapest fee quintile recorded a success ratio of 67 per cent, compared with just 29 per cent for those in the most expensive quintile, while funds in the intermediate quintiles produced similarly weak results.

“Over the five-year period ended December 2025, this market environment posed significant challenges for active managers, particularly those employing high-conviction, fundamentally driven strategies,” the report says.

“Despite elevated volatility during 2025, low-cost index funds and a small number of inexpensive systematic active strategies emerged as clear beneficiaries within the global large-cap grouping.”

However, fixed income strategies avoided the same impact, where funds employing passive strategies – which were unable to take active decisions, including the ability to trim duration in a rising-yield environment or to go overweight credit exposure as spreads narrowed – achieved a low success ratio of 33 per cent even though they were in the cheapest fee quintile.

However, higher-fee fixed-income strategies do not necessarily get better performance with a success ratio of 4 per cent.

“Broadly, these findings align with our view that active fixed-income managers can deliver stronger outcomes over a full economic cycle, primarily through a persistent overweight to corporate credit relative to benchmark indexes,” the report says.

“That said, while active managers frequently outperform fixed-income indexes on a gross-of-fees basis, these gains do not always translate into superior net outcomes once fees are accounted for.”

Leave a Comment

You must be logged in to post a comment.