The estimated FY24 ASIC levy figure will remain largely in-line with the revised FY23 figure released six months ago, but advisers will still be on the hook for another costly bill.

ASIC announced on Monday the projected FY24 levy will be $1500 per licensee, plus $2878 per adviser.

For now the figures are only a guide, as final levies are announced towards the end of the year and firms will be invoiced at the start of the 2025 calendar year.

A year ago, the regulator projected a $3217 per-adviser levy, which was reduced to $2818 later that year.

The industry has argued fervently against increases in the levy, particularly as Minister for Financial Services Stephen Jones campaigned heavily on reducing the cost of advice.

The minister has instead relied on the experience pathway and the Delivering Better Financial Outcomes legislation to lower the cost of advice, conceding the government had other priorities to focus on.

The new levy figures come a week after Coalition Senator Andrew Bragg’s review into ASIC’s operations recommended another review of the IFM with the suggestion more funding be derived by the proceeds of regulatory fines and penalties rather than a broad-based levy.

The industry has also been critical of having to pay for the fallout from enforcing unlicensed advice, which Treasury argued benefits the advice profession.

The Coalition government froze the ASIC levy in 2021 due to a reduced number of advisers having to cover a higher proportion of the regulator’s cost recovery.

The freeze meant the industry continued to pay the FY19 rate of $1142 per adviser, but after the conclusion of the review of the Industry Funding Model, Treasury recommended ending the levy freeze.

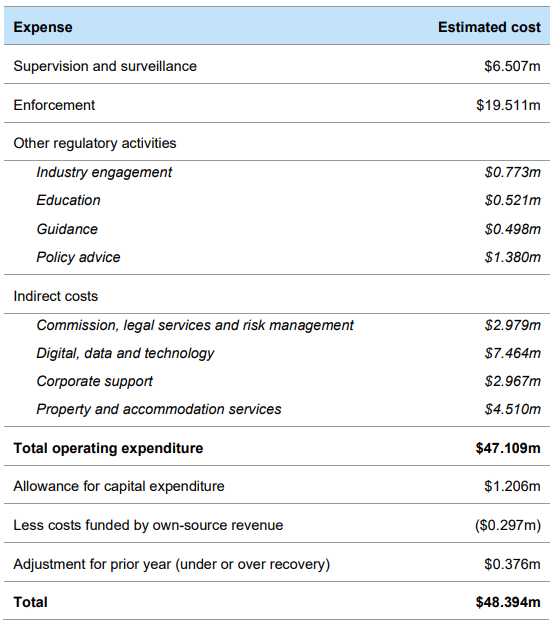

The estimated cost recovery amount for FY24 was $48.39 million, to be paid by 2766 AFSLs and 15,371 advisers. ASIC calculated the number of advisers based on how many were authorised to provide retail advice at the end of the financial year.

Licensees that provide general advice only will pay a levy of $2721, which equates to cost recovery of $2.99 million across 1097 advisers; while wholesale-only licensees will pay $976, recovering $1.88 million of costs from 1931 advisers.

Breakdown of ASIC costs for advice sector

ASIC cited enforcement action against unlicensed advice and superannuation switching cold-callers, the latter of which led to the Super Members Council’s infamous “dodgy advisers” media campaign, as the key initiatives for which it is recovering costs from the advice sector.

It also published Report 779 ‘Superannuation choice products: What focus is there on performance?’ and commenced its review into SMSF advice, launched the new adviser registration system, and persisted with its cyber and operational resilience project.

For ongoing work, it manages the financial adviser exam, the Financial Services and Credit Panel, and annual reporting of the reportable situations regime (otherwise known as breach reporting).

It also noted its work investigating non-responses to Australian Financial Complaints Authority, and supporting the establishment of the Compensation Scheme of Last Resort.

Leave a Comment

You must be logged in to post a comment.