The government’s plan to change advice opt-in periods from 24 to 12 months actually stretches out to a 15-month span and should be extricated from the FDS process entirely, according to the Association of Financial Advisers’ head of policy, Phil Anderson.

Presenting at the AFA’s Sydney Roadshow this morning, Anderson said the proposed annual renewal arrangements before parliament aren’t even annual.

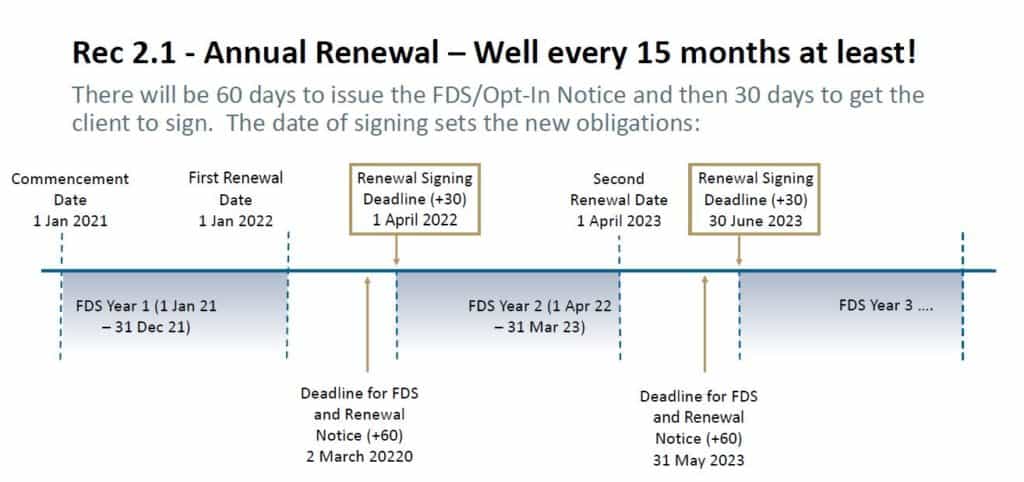

“That is because you’ve got the 12-month period and then you’ve got 60 days to issue the FDS and the opt-in notice, and then the client’s got 30 days to sign the opt-in,” he said. “That’s 15 months, and then it resets and a new period starts. So effectively they’re giving us a 15-month renewal outcome.”

The AFA’s preferred solution, he outlined, was for clients to be able to opt-in at any time between the ninth and fifteenth month. “Give them not a 30-day window of opportunity but a six-month window of opportunity and we continue to work off a fixed anniversary date,” he said.

Anderson took exception to the fee disclosure statement process in general, revealing that the AFA believed the FDS should be repealed entirely. “The information is already included in product statements,” he argued, adding that there was “no great consumer benefit” in the document.

“The FDS is a most remarkable exercise,” Anderson said, before highlighting anomalies around remuneration accountability, GST inclusivity and the tax deductibility of fees. “FDS is a fundamentally flawed process,” he concluded.

Tying the new annual opt-in to the FDS was a mistake, Anderson said. “If you disconnect FDSs from opt-in then all of a sudden you can take a much more sensible approach to opt-in,” he added.

Alongside the annual opt-in change, the government is proposing that FDS documents be extended to include services and fees for the following year. If estimates are given, explanations must also be provided. This is on top of ‘lack of independence’ disclosure and other changes in line with recommendations out of the Hayne royal commission.

Anderson said the current draft Bill, if passed in its current form, would win the “gold medal for red tape”. Unless fixed, he warned, the changes “will add a huge amount of red tape for no benefit.”

The policy head also took aim at the government’s handling of the Financial Adviser Standards and Ethics Authority, particularly the way Standard three of FASEA’s Code of Ethics treats conflicts of interest. He compared the standard – which says advisers can’t “advise, refer or act” where a conflict exists – to the political machinations of the people that mandated the changes.

“It’s a bit like telling a political party that they can’t support a project in an electorate they’re targeting at the next election,” he said. “I don’t think the term ‘pork barrelling’ started in the financial advice sector. We all know that politics is based on doing deals where conflicts come into play…”

Leave a Comment

You must be logged in to post a comment.