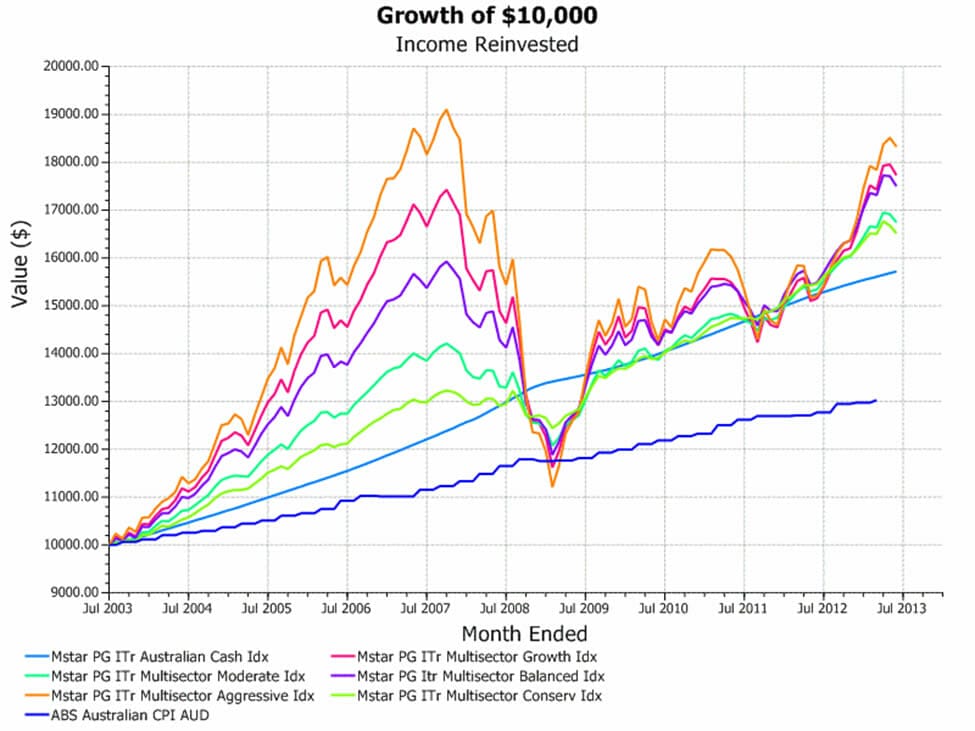

Many investors question the validity of the strategic asset allocation models that the investment industry recommends. Those investors are less keen to move up the risk spectrum, even when they have long investment horizons, and the chart below demonstrates why.

When looking at ten-year performance numbers, the returns for each broach asset allocation profiles inch ahead of cash but the difference between returns from the more aggressive and more conservative models remain modest.

Chart: Growth of $10,000 over 10 years. Source: Morningstar

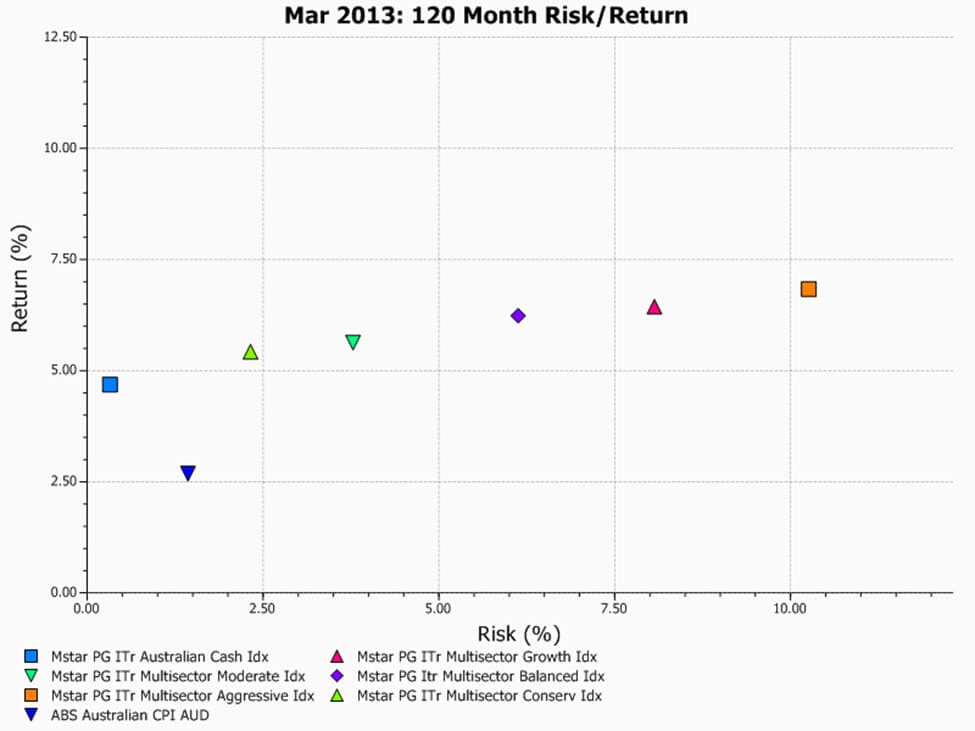

The idea that investors have not been rewarded for following traditional investment theory, with significantly greater risk taking rewarded with only slightly higher returns, is supported by the next chart. However, the chart also shows that even the most aggressive investors have managed to keep well ahead of inflation and, in real terms, outcomes across the risk spectrum have at least been positive.

Chart: Risk vs Return for different asset allocation models over the last 10 years. Source: Morningstar

There was a time not very long ago, where the information encapsulated in the above chart was routinely plugged into the software used to derive optimum asset allocation models in the belief that over the long term at least the future would look similar to the past. Unfortunately if enough people believe that to be the case then it is less and less likely to be true because markets do not stand still, but rather are constantly discounting investor’s views of the future.

The investment industry is more forward looking now and a valuation-based view of the capital markets is more prevalent. The final chart uses a simple model of valuation-based risk premiums to come up with a theoretical expected return for different domestic asset classes over time.

Chart: A simple model of forward looking risk premiums. Source: Bloomberg, Morningstar, RBA

The chart shows that risk premiums for Australian equities remain robust relative to defensive assets but that further down the risk spectrum quantitative easing and investors’ extreme risk aversion have created anomalies. Achieving decent real returns from traditional defensive assets will be challenging while, perversely, government bonds might still hold some appeal for longer term investors as a portfolio diversifier. Maybe a more rational response by conservative investors with nearer term real return and capital preservation goals would be to hold a bit more cash to meet shorter term needs while also increasing equity exposure.

This reality calls into question how diversified portfolios have traditionally been constructed – in particular, the tendency to start with a balanced portfolio and merely vary the proportion of defensive assets versus growth assets according to the investor’s return objectives and time horizon. Markets have made it abundantly clear, if there was ever any doubt, that every asset needs to be considered on its individual merits and its current valuation.

Leave a Comment

You must be logged in to post a comment.