The Australian Financial Complaints Authority closed more investment and advice complaints that it received last financial year, reducing its backlog.

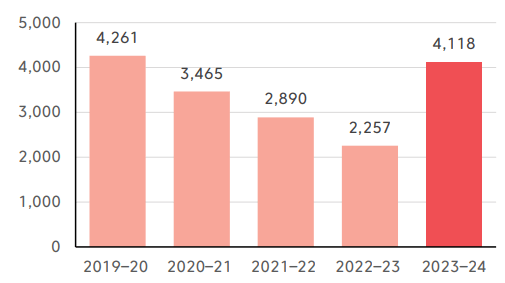

Publishing its annual report this week, AFCA closed 4118 investment and advice complaints in FY24, an 82 per cent increase compared to FY23.

Investments and advice complaints closed

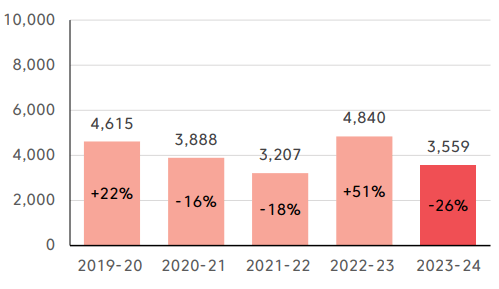

AFCA received 3559 complaints in the investments and advice sector, a drop of 26 per cent compared to the previous year.

“This reflects the positive impact of enhanced education standards and increased professionalism within the industry, leading to fewer disputes,” the authority said.

Excluding complaints about the much-maligned Dixon Advisory, advice complaints reached an “all-time low” of 2709 complaints, according to AFCA.

During the AFCA annual member forum on Friday, lead ombudsman for investments and advice Shail Singh noted that not all Dixon complaints have ruled in favour of the complainants, pointing to one case where the claimant wasn’t worse off after taking conflicted advice.

AFCA senior ombudsman for investments and advice Patrick Hartney said the case still found a breach in terms of conflict of interest and potentially inappropriate asset allocation, but no compensation would be rewarded.

“When that was compared to what AFCA or the panel had considered to be appropriate advice the complainant was actually better off with the conflicted advice from a result perspective,” Hartney said.

Hartney said that even with a “cookie cutter advice” approach from an adviser that may have been the wrong thing, the application and implications of that can differ from complainant to complainant.

“It may actually have been appropriate for one or two people, it’s not just a blanket rule that this one piece of advice is bad and it’s bad for everyone,” Hartney said.

“There could be certain people where it could be okay for or in other cases there may not have been a loss.”

Investments and advice complaints received

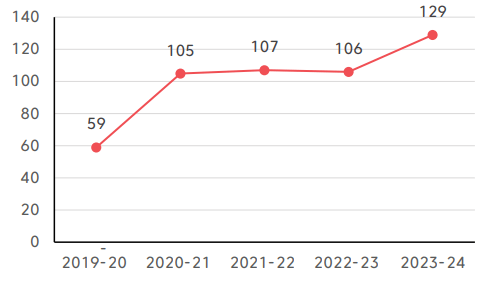

The annual report showed 44 per cent of complaints – which AFCA described as a “significant portion” – were resolved at the “rules review” stage, where complaints are assessed against the authority’s jurisdiction and procedural rules and typically requires complex decision-making.

But AFCA noted this complexity is why the average time to resolve complaints has risen to 129 days.

Average time to close advice and investment complaints in days

Industry challenges

Despite the decrease in advice complaints, inappropriate advice remains the top issue accounting for 706 complaints (20 per cent of the total).

Issues with retail and wholesale classifications continue to be one of the biggest challenges for AFCA; the authority has no jurisdiction over wholesale complaints but can step in if a complainant has been inappropriately considered a wholesale client.

However, the authority noted there has been ongoing confusion regarding the classification of SMSFs as wholesale investments with some advisers incorrectly applying the $2.5 million in net assets or $250,000 annual income threshold usually applied to establish a wholesale investor, rather than the specific $10 million threshold for superannuation products.

AFCA senior ombudsman for investments and advice Alex Sidoti said the $2.5 million/$250,000 rule doesn’t relate to financial services provided in relation to a superannuation product.

“It’s pretty clear that actually doesn’t apply in circumstances where advice is given to a trustee to an SMSF,” Sidoti said.

“In order for a trustee to be treated as a wholesale client, the SMSF has to have $10 million in assets to be wholesale otherwise it’s a retail client.”

The authority also had concerns about SMSFs being opened for low balance clients, usually involving inappropriate recommendations and a lack of investment diversification.

AFCA also noted issued complaint trends based on market volatility, particularly with upcoming elections in the US and Australia.

Top five investments and advice complaints received by issue

| FY20 | FY21 | FY22 | FY23 | FY24 | |

| Inappropriate advice | 585 | 534 | 241 | 1662 | 706 |

| Failure to act in client’s best interests | 469 | 525 | 281 | 534 | 565 |

| Failure to follow instructions/agreement | 575 | 229 | 332 | 951 | 304 |

| Service quality | 380 | 674 | 570 | 371 | 298 |

| Interpretation of product terms and conditions | 76 | 100 | 654 | 116 | 223 |

Source: AFCA

AFCA senior manager Eunice Sim said only 18 per cent of advice complaints closed at the registration referral stage which was largely due to the complexity of the complaints.

“Personal advice that’s given can be a little more involved, and also the amount of compensation that has been claimed can be substantially higher than transactional types of complaints we see,” Sim said.

AFCA becomes battletested in the war on scams

The government announced on Thursday evening it would nominate AFCA to operate the External Dispute Resolution scheme for the first three designated sectors under the Scams Prevention Framework, part of the “war on scams” launched by Minister for Financial Stephen Jones.

These three sectors are banks; telecommunication service providers; and digital platforms providing social media, paid search advertising and direct messaging.

Scam victims will be able to seek compensation through this single EDR if they have been unable to reach a satisfactory outcome through internal dispute resolution, even if the complaint is against multiple regulated industries.

The government announcement pointed as an example a person that might be the target of a scam on social media who loses money from their bank account – the social media company and bank would both be liable if it was found they didn’t have adequate protections in place.

Currently, social media companies have no internal or external dispute resolution mechanism.

Leave a Comment

You must be logged in to post a comment.