*This article is produced in partnership with PIMCO

Following four-plus decades of decline, bond yields (which move in the opposite direction to bond prices) have spiked sharply over the past year. This reflects a surge in inflation, driven by factors such as the Ukraine war, global supply-chain problems caused by pandemic lockdowns, and rocketing demand as those lockdowns have eased. It also reflects sharp hikes in interest rates as central banks have reversed the loose monetary policy of the pandemic and post-global-financial-crisis era in an effort to combat inflation. The sharp rise in bond yields (meaning bond prices have fallen) has left many investors understandably wary. However, we believe that the rate-hiking cycle, which contributed to last year’s volatility across asset classes, is coming to an end in most developed markets.

Opportunity knocks as the outlook improves

The outlook for fixed income has become much more positive. Following central bank moves in 2022 and 2023, bonds now offer more attractive yields than they have in several years. Importantly, higher yields mean greater potential returns for investors. Historically, starting yields are very closely linked to prospective returns. So, if you invest in a high-quality bond with a 4 per cent yield today, your average annual expected return on that bond should be approximately 4 per cent.

Critically, bonds tend to perform well in times of financial turbulence: they have typically delivered positive returns and outperformed equities during recessionary periods. Given the uncertain geopolitical and economic outlook and the prospect of recession this year, equities, by contrast, appear vulnerable.

While further increases in yields (beyond current market expectations) could lead to short-term losses, they would improve the reinvestment opportunity and could lead to higher returns over the long run.

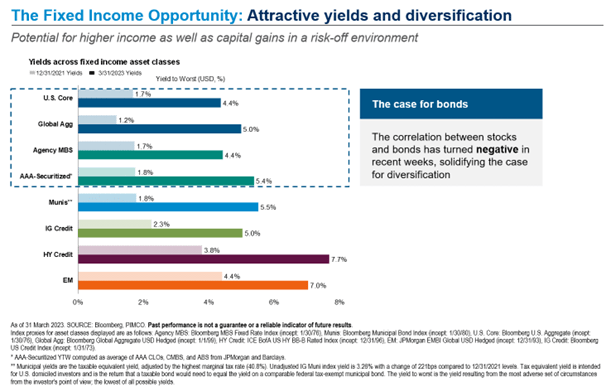

Figure 1: Attractive yields and diversification

The portfolio diversification benefits of investing in bonds

Bonds issued by governments and large, healthy companies are generally regarded as being among the safer investments. Moreover, you can diversify risk by investing in bonds issued by a broad range of issuers. Since bonds tend to be less volatile than equities over the long term, investing in fixed income can act as an anchor in your portfolio and help cushion it against potential downside risks when markets encounter volatility. And because prices for bonds and equities tend to move in opposite directions during periods of economic stress, the two investments, when combined, help to create a well-balanced portfolio. The ability of bonds to improve a portfolio’s resilience is enhanced during a period when interest rates are rising sharply – as is the case now. That’s because the hike in borrowing costs means there is significant scope to cut rates when the economy slows.

The advantages of an active approach

PIMCO has over 50 years’ experience in successfully navigating the complexities of the vast global fixed-income asset class. We believe that taking an active approach that aims to beat the benchmark, rather than a passive approach that simply aims to track it, can lead to attractive additional returns. We use various strategies to generate these returns.

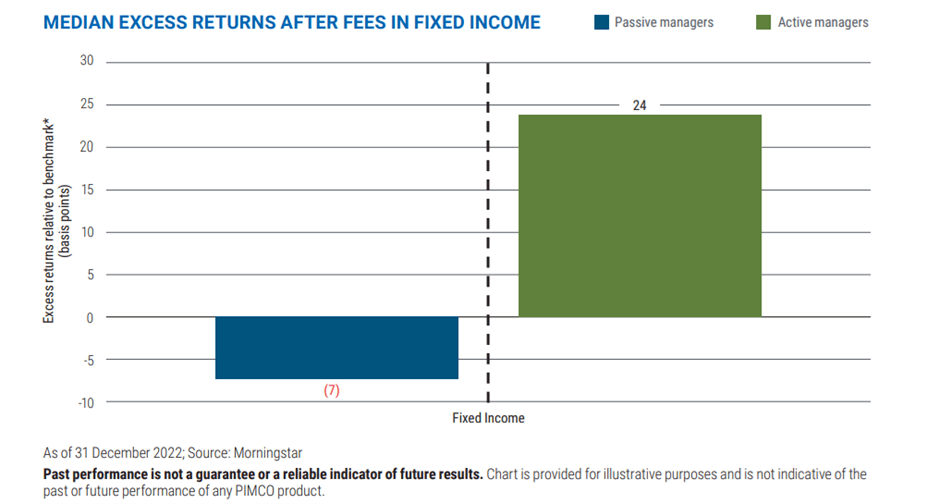

The chart below shows that active bond managers have outperformed their passive peers, generating higher returns than the benchmark after fees. Even when you factor in the extra cost of active management, you are still potentially earning more.

Figure 2: An active approach to fixed income can potentially generate excess returns

The time to consider bonds is now

For those who’ve been sitting on the sidelines of the bond market, we see a strong case for investing in fixed income today. At current yield levels, bonds can provide an attractive balance between income generation and a cushion against downside economic risks. Taking an active approach should further enhance returns. Moreover, given bonds’ traditional role as a portfolio diversifier, exposure to fixed income should boost a portfolio’s overall resilience and its ability to preserve capital.

Disclaimer:

Performance results for certain charts and graphs may be limited by date ranges specified on those charts and graphs; different time periods may produce different results. Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product.

Diversification does not ensure against losses.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

The material contains statements of opinion and belief. Any views expressed herein are those of PIMCO as of the date indicated, are based on information available to PIMCO as of such date, and are subject to change, without notice, based on market and other conditions. No representation is made or assurance given that such views are correct. PIMCO has no duty or obligation to update the information contained herein.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

Leave a Comment

You must be logged in to post a comment.