APRA expects that by now every superannuation fund in Australia should have formulated and published a retirement income strategy. The overarching themes of personalisation and the need for advice shine through some of the more progressive funds’ strategies. Why? No single Australian’s retirement is the same—the notion of the “average” client simply doesn’t exist. But advisers know that. After all, the advice industry has been providing personalised strategies for years and helping retirees answer the big question: How much should I spend each year? But if personalisation is the way forward, is it time to consider the role of minimum drawdown rates in superannuation?

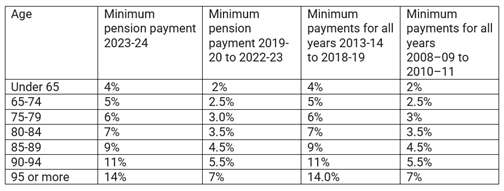

A retiree’s annual expenditure informs their comfort level in retirement, not to mention whether they will run out of money or rely on the age pension more heavily or sooner than anticipated. But determining a safe level of annual income in retirement to avoid running out of money is the nastiest, hardest problem in finance, according to Nobel laureate William Sharpe. Many pension streams are subject to a minimum amount to be withdrawn each year, and the consequences of not complying are serious— your super pension could lose its tax-free status. The legislated minimum drawdown rates were introduced in July 2007, and the rates have varied through time, particularly in response to very poor market conditions (Table 1). After all, in severe market selloffs, withdrawing less from superannuation enables more to remain invested for the inevitable rebound.

Table 1: Minimum percentage factor for certain pensions and annuities (indicative only) for each age group

Source: Australian Taxation Office – Key Superannuation Rates and Thresholds.

The concept of variable spending levels (that is, spend less in weak markets and more in strong markets) is relatively well-documented. A Morningstar study demonstrated that a more flexible withdrawal strategy could sustain a higher withdrawal rate compared with other strategies. But, clearly, some retirees may not like the annual spending variability, and it also tends to lead to lower final balances. So, depending on bequest preferences, this may be appropriate for some and not for others. Vanguard also believe a “dynamic spending” approach has merit. But both agree these more-flexible approaches work best when the investor can receive guidance to help determine the optimal level of spending each year. In a period like FY22, where many diversified portfolios across the risk spectrum have lost money and the consumer price index has jumped, there is a lot to balance when determining the “right” level of expenditure for financial year 2023.

No one-size-fits-all solution

Clearly the legislated minimum rates pose a barrier to flexible withdrawal approaches. And the evidence presented to date reveals that many Australians acceptingly use these rates as a rule of thumb. An empirical study of 44,000 Australian retirees found that almost half of the sample closely followed the minimum drawdown rates. It’s not apparent what is compelling these individuals to follow the minimums—anchoring, balance preservation, soft compulsion (default options), financial advice, or some other reason. What is apparent is that these withdrawal rates are providing guidance to a considerable proportion of Australians, making it a delicate decision for policymakers to tinker with them.

As you would expect, the study also found that there is a lot of individual variation hidden in the detail of the respondents. For example, the study found that individuals with higher account balances typically draw less in excess of the minimum rate compared with a retiree with a lower account balance and women draw more slowly through their account balances than men. Further, around one third of the retirees surveyed took advantage of the lower minimums introduced following the global financial crisis.

What is clear is that the optimal level to be withdrawn each year is contingent on so many individual factors: age and life expectancy; market conditions; wealth levels; gender; bequest preferences; spending preferences; balance preservation; aged-care living options—the list goes on. But what is not clear is how we are going to empower Australians to optimise their retirement income level while ensuring that super is being used for its intended purpose.

Perhaps the Retirement Income Covenant will be the birth of some useful digital tools that will give retirees the confidence to set an annual income level that is right for them, suits the prevailing market conditions, and reflects the objective of super. However, to help advisers and investors properly tailor a personalised retirement income strategy, policymakers should carefully reconsider the legislated minimums and the level of member data available to super funds. Neither support the provision of fully personalised solutions. And then there’s the issue that many members would like to “chat” with someone who can provide them comfort around the complex trade-offs they are trying to make. Let’s leave that to the Quality of Advice Review.

Annika Bradley is director, manager research ratings, Asia-Pacific for Morningstar.

Leave a Comment

You must be logged in to post a comment.