I’ve been ruminating on an article published in Professional Planner by Robert MC Brown, Time to stop the financial literacy lip service. I recommend you read the article. In it, Brown raises the legitimate question of whether the time, effort and resources being put into improving the nation’s financial literacy were likely to work and, if they were not, whether diverting that energy to better regulation and enforcement might product better consumer outcomes.

I was recently privy to a conversation relating to the article, which was fairly lively. Both participants are supporters of financial literacy programs, but only if they are delivered to consumers effectively – and, crucially, not delivered by those whom higher financial literacy might disadvantage such as unscrupulous financial services providers – and as long as they are not seen as a substitute for good laws and robust enforcement of those laws.

Our conversationalists agreed that financial services providers have to be held to account for their actions irrespective of how well or how poorly informed consumers might be. This is especially true of financial advisers – it is the role of the professional, after all, to use their superior knowledge, skill and experience on behalf of a client, not against the client.

Using these questions we wanted to start exploring whether consumers themselves think improving financial literacy is a step towards arming them to recognise and avoid financial scams, poor advice or misconduct by financial services providers.

Earlier this year, CoreData included some questions about financial literacy in a survey of consumers, conducted in the wake of the Hayne royal commission.

Commissioner Hayne made it clear that ultimately, consumers are responsible for their own actions. That’s fine, but when someone is in a game of cards against a player who’s stacked the deck, or who only half-explains the rules of the game, or worse, misrepresents the rules or changes them mid-game, it’s a bit of a stretch to expect them to necessarily recognise what’s going on. That’s why Hayne ran an inquiry into financial services companies’ misconduct, not into consumers’ lack of financial literacy.

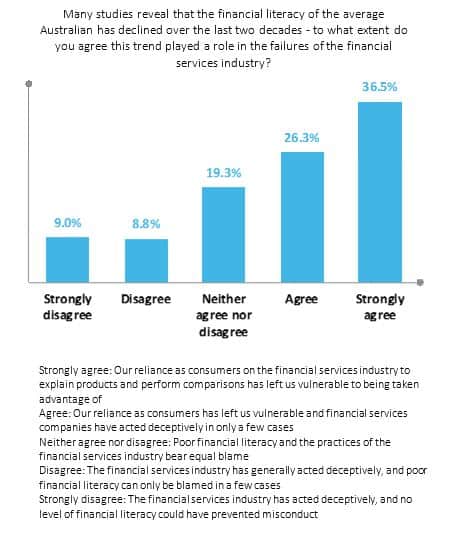

The subtext of the research was to explore just what responsibility consumers should take for their own actions, or lack of actions, when financial services providers go bad. The message that came back was fairly clear. Just over a third (36.5 per cent) of consumers said declining financial literacy over the past two decades and their resultant reliance on the financial services industry to explain products and perform comparisons has left them vulnerable to being taken advantage of.

The subtext of the research was to explore just what responsibility consumers should take for their own actions, or lack of actions, when financial services providers go bad. The message that came back was fairly clear. Just over a third (36.5 per cent) of consumers said declining financial literacy over the past two decades and their resultant reliance on the financial services industry to explain products and perform comparisons has left them vulnerable to being taken advantage of.

About 20 per cent thought poor financial literacy and the practices of the financial services industry were equally to blame for the failures of the financial services industry. Less than 10 per cent thought that no level of financial literacy could have prevented misconduct.

There’s a recognised psychological phenomenon, which we discuss often our office – and usually about each other – called the Dunning-Kruger Effect, which says, essentially, that the less someone knows about a particular subject, the less likely they are to recognise how little they know. Forbes magazine personalised the concept thus: “If you’ve ever dealt with someone whose performance stinks, and they’re not only clueless that their performance stinks but they’re confident that their performance is good, you likely saw the Dunning-Kruger Effect in action.”

One of the propounders of the effect, Professor David Dunning, says the knowledge and intelligence that someone needs to be good at something are often the exact same knowledge and intelligence they need to recognise they are not good at it.

There’s an element of this in the way consumers have been asked to interact with financial services providers.

Consumers who lack the knowledge – I won’t say intelligence, because some people who are victims of misconduct are not stupid people – to know how financial products and services work and what they’re supposed to do lack the very knowledge they need to realise when they don’t work as they should.

Consumers themselves recognise that declining financial literacy levels make them vulnerable to predatory financial services practices. Raising financial literacy might be a step towards counteracting this issue but only, as Brown wrote last month, if programs are well structured and not delivered by those who have a vested interest in them not working.

Leave a Comment

You must be logged in to post a comment.