BT Financial Group has attempted to refute a Bell Potter research report that found the highly publicised fee changes to its Panorama platform didn’t stack up against its competitors, especially for lower balances.

The research, led by Lafitani Sotiriou, compared similarly structured platform offerings across three categories. It concluded that Panorama’s new fee package – which featured a 15-basis-point asset-based administration fee – “performs below average overall”.

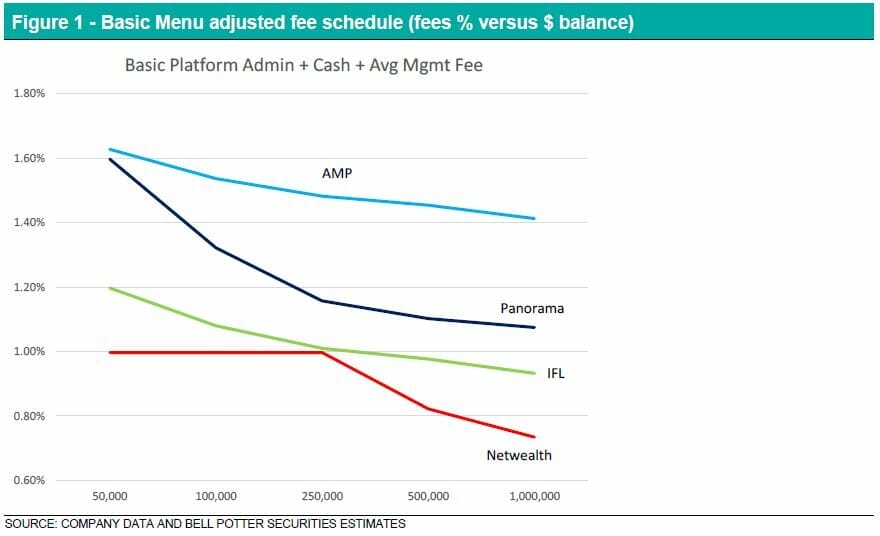

Among basic menu platforms, Bell Potter revealed (Figure 1), Panorama Compact and AMP’s MyNorth have “adjusted fee schedules” – including the basic platform fee, cash account fee and cost recovery fee – that perform comparatively poorly across both low-balance and high-balance accounts.

BT described the report’s findings as misleading and inaccurate.

“We note the report but disagree with the analysis and some calculations,” the BT spokesperson said.

Hype and hoopla

BT announced the new pricing structure for Panorama on July 23, along with the launch of its Compact platform, which offers lower pricing for a stripped-back investment selection.

While the 15-basis-point asset-based administration fee dominated the headlines, the new prices also included a $540-a-year flat account fee for wrap (super and non-super) platforms and a $180-a-year account fee for the Compact version.

Bell Potter’s report, published in July, highlighted that hidden fees are a factor in Panorama’s comparatively poor performance. In particular, the report noted that BT separates the $80-a-year cost recovery fee from the asset-based administration fee, while other platforms generally include it.

“Only Panorama splits the cost recovery fees from the administration fees,” the report stated, “which helps the company report a lower headline admin fee (15bps).”

Unflattering results

In the basic platform comparison, BT’s Panorama Compact offering is pitched against Netwealth Supercore, AMP MyNorth Super Select and IOOF Pursuit Focus Personal Superannuation.

Sotiriou’s analysis took average management fees into account, “to avoid a platform appearing to have a low administration fee, only to capture it elsewhere through an unusually high management fee”, which is crucial given that many of the basic menu options include expensive internal products.

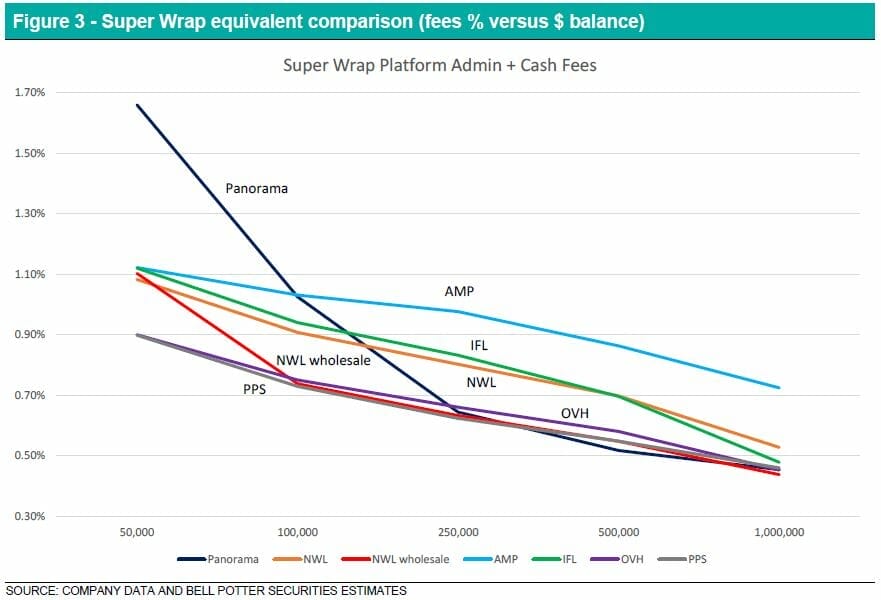

For super wrap platforms, BT’s fees fare much better on accounts with balances over $250,000, with charges comparable to competitors’, but the report stated that they remain “price uncompetitive” for low balances (See Figure 3).

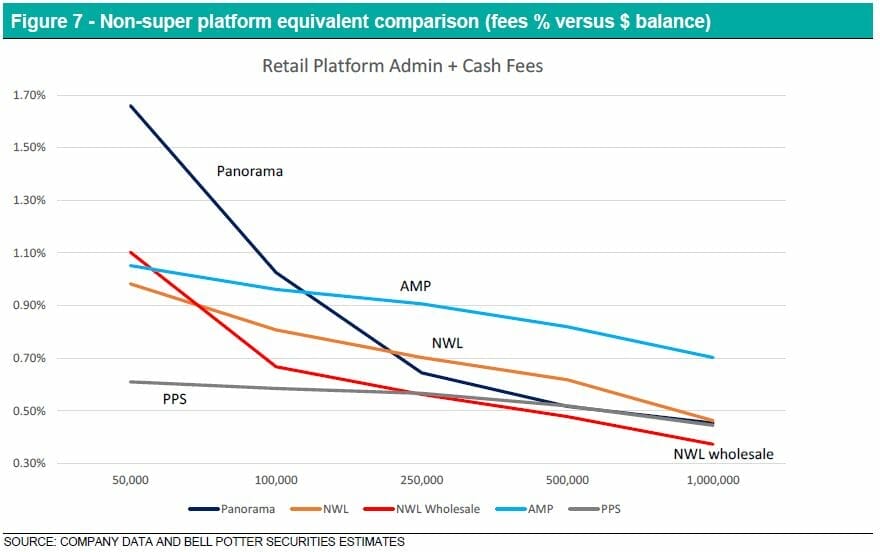

The review of non-super platforms (see Figure 7) paints a similar picture, with Panorama proving expensive for low-balance accounts and competitive on the higher-balance end. Sotiriou’s analysis showed AMP as the “most expensive” platform overall, and picked up on a pricing anomaly.

“We note that AMP’s fees [shown for non-super platforms] are only for new clients,” Sotiriou’s report stated. “Existing clients, incredulously, are charged at a higher rate.”

Inconsistent comparisons?

BT stated lower client fund balances used in the comparison aren’t relevant to a full wrap offer.

“For example, the $50,000 balance comparison would be more relevant to a MySuper product or a limited menu ‘Compact’ product,” BT’s spokesperson said. “We believe a more appropriate basis of comparison would be from $250,000 to $1 million in client portfolio balances.”

The report noted the product analysis “doesn’t cover all fees, like switching or exit fees, or trading fees”, due to the added complexity. The report also does not account for varying levels of functionality across the platforms, despite attempting to group products that are largely similar.

King of the hill

BT enjoys a strong position at the top of the platform hierarchy, with almost $150 billion in funds under administration. AMP is second on $143 billion, with CBA/Colonial ($120 billion) and NAB/MLC ($115 billion) completing the top four. PP broke down the platform landscape in this recent feature.

Macquarie led the so-called second tier, with $76 billion under administration, followed by ANZ, IOOF, Mercer, StatePlus, Netwealth, Hub24, Praemium and OneVue, rounding out the list of significant players in the market.

The Bell Potter report concluded that while the incumbent providers still dominate the market, the second tier – in particular the newer platforms such as Praemium and Netwealth – will continue to chip away market share.

Leave a Comment

You must be logged in to post a comment.