For investors, this is perhaps the quietest start to a financial year in years. Of course there are problems, like possible trade wars and the US-North Korea relationship to consider, but these are minor compared with problems front of mind in most years just gone by. Nevertheless, it is important to structure a portfolio to try to make the best of expectations – even if they are largely benign.

In recent issues, I have written about needing to blend different strategies and allocate to stocks within those strategies. My flagship model portfolio has been generating more than 7 per cent a year over the ASX 200 Accumulation Index since inception (February 2014). It is weighted 100 per cent to the conviction-style portfolio and 0 per cent to the high-yield portfolio.

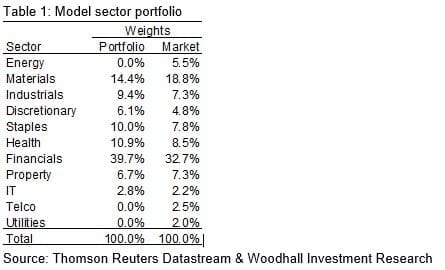

In stage one of my allocation modelling, expected risks and returns are optimised. The latest portfolio did not allocate any weight to the Energy and Telecommunications sectors. At the second level, the algorithms couldn’t find any stocks in the Utilities’ sector that fit the criteria for inclusion. These three sectors account for about 10 per cent of market capitalisation. Therefore, the other eight sectors must then be overweight, on average.

I show the portfolio’s sector weights alongside the sector market capitalisation weights in Table 1. Given the consequential bias for overweight in the included sectors, it is noteworthy that Materials is quite underweight (14.4 per cent vs 18.8 per cent). Property is the only other underweight sector.

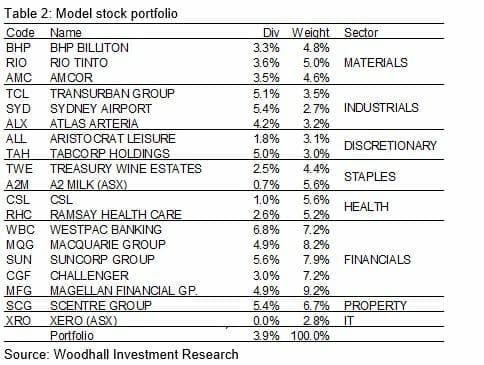

Given my comments in recent issues of Professional Planner about investing in Financials, one might at first question the slight bias to Financials in Table 1. However, when we drill down to the stock level in Table 2, we can see that there is only one big bank in that allocation (Westpac). CGF and MGF are fund managers. Suncorp (SUN) has a dominant insurance focus and Macquarie is not like any of our big banks. This portfolio has only a 6.8 per cent weight in big banks.

Given my comments in recent issues of Professional Planner about investing in Financials, one might at first question the slight bias to Financials in Table 1. However, when we drill down to the stock level in Table 2, we can see that there is only one big bank in that allocation (Westpac). CGF and MGF are fund managers. Suncorp (SUN) has a dominant insurance focus and Macquarie is not like any of our big banks. This portfolio has only a 6.8 per cent weight in big banks.

If we turn to the Industrials sector, the three included stocks are all what are normally referred to as ‘bond proxies’. TCL and ALX are road infrastructure stocks with stable incomes. SYD is an airport monopoly infrastructure project. With the beginning of a stable hiking policy on interest rates in the US, the real issue is not whether investors will view bonds with a slightly higher rate as an alternative investment, but whether the higher interest rates will reduce the profitability of such highly geared infrastructure companies.

There is no doubt that a prudent investor should keep an eye on these stocks but we depend heavily on broker forecasts of earnings and dividends. That is what has helped achieve a 7 per cent outperformance. What I find interesting is that, after many years of no allocation to IT stocks, XRO has joined the team. No dividend is expected (column 3, Table 2) but recent capital gains have been stellar.

The expected dividend yield of the model portfolio is 3.9 per cent, which is a little shy of the average yield for the ASX 200. But if my capital losses would otherwise swamp my yields, I will happily accept a 3.9 per cent yield with reasonable franking credits and some capital gain.

With the whole of 2018-19 ahead of me, I am happy to accept most of the computer’s recommendation for the Australian component of my self-managed super fund. But I have a soft spot for Cochlear (COH). I’ve made so much money from that stock over a decade or two and I think I will do the same in the future – in spite of the consistently poor consensus recommendations for the stock. It’s a past and future captain’s pick.

With the US Fed’s plan for normalising rates, China’s growth prospects, and the EU being at least stable, I feel happy. My only big worry is that our recent euphoria over our 3.1 per cent economic growth was misplaced. It was fuelled by household savings going close to zero again – just like in 2008.

Dr Ron Bewley is a principal of Woodhall Investment Research and a regular columnist for Professional Planner.

Leave a Comment

You must be logged in to post a comment.