For all of 2017, we were less sanguine than many others about rising market prices, which began more meaningfully detaching from valuations in late 2016. A strict adherence to ‘absolute’ value and quality has put us out of step with a strongly rising market, fuelled by momentum and enthusiasm for the internet’s ability to change the world.

Despite arguably attractive relative valuations, compared with US 10-year Treasury bonds, we have been unwilling to hitch our barrow to an argument that vaporises if US interest rates start to climb.

And they have.

In my last Professional Planner column, I noted; “The S&P 500 Total Return Index has risen 258.72 per cent over the nine years since December 31, 2008. During this period, US 10-year Treasury bond rates averaged just 2.54 per cent. For the nine years prior to that period, 10-year notes averaged a higher 4.23 per cent, and for the nine years prior again, an even higher 6.26 per cent. The steady decline in bond rates has been a strong tailwind for asset prices…”

That tailwind is now easing, however, with rates on US 10-year Treasuries having risen from a low of 1.36 per cent in mid-2016 to 2.92 per cent today.

The supportive influence of lower interest rates has led to booms beyond the traditional asset markets of equities, bonds and property. Record prices have been seen in many non-income producing assets, such as collectible cars, stamps, wine, coins, art and low-digit licence plates, along with cryptocurrencies. These record prices, especially in assets that produce no income, have always been associated with the last stages of a credit cycle.

Irrational exuberance and the heavily crowded buying of a narrow subset of stocks are also typical of the late stages of a boom, and this time it has been the US technology sector that has been the focus of investor amore. Don’t forget the observations from last month’s column of 300 per cent to 400 per cent share price increases over a few days for listed companies that had simply changed their name to include the word ‘Blockchain’.

Of course, as is typical in the late stages of a boom, equity investors have been blissfully unaware of, or complacent towards, the dangers of paying high prices after a long period of ultra-low volatility.

In mid-March this year, investors injected $3.3 billion into the biggest exchange-traded fund tracking the Nasdaq 100 index, the PowerShares QQQ Trust Series 1 – the most in any single week since the dotcom boom. JPMorgan states that investors also poured $34 billion into equity ETFs in the week ending March 16 – the biggest weekly inflow ever.

The question of whether the boom will end is easy to answer, the more challenging query is when.

The answer to that question is perhaps being written now.

In the past, one signal that a shift in sentiment is approaching has usually been when investors in one market reverse sentiment sharply, even as investors in another, related market continue to demonstrate unbridled enthusiasm.

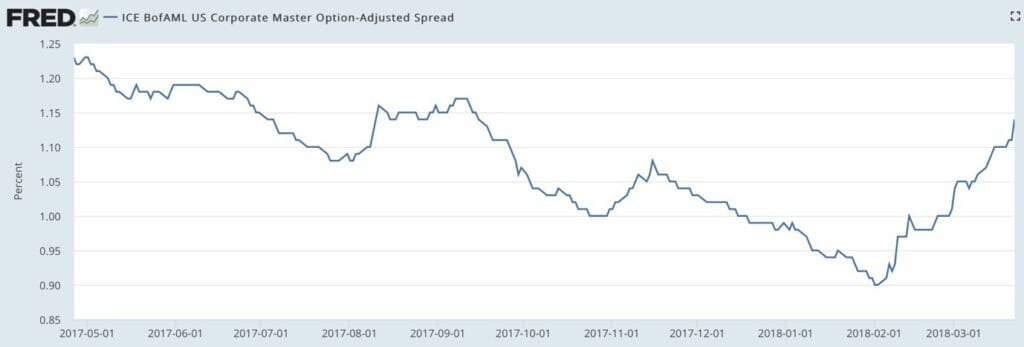

And so, it is bond investors who are rapidly repricing corporate credit markets, even as equities attempt to surmount record highs. Investment-grade bond spreads now sit near their widest in six months (see Figure 1) and yields have risen to their highest in more than six years.

Figure 1: Corporate Bond Spreads

Source: St Louis Fed

Sooner or later, the boom will end.

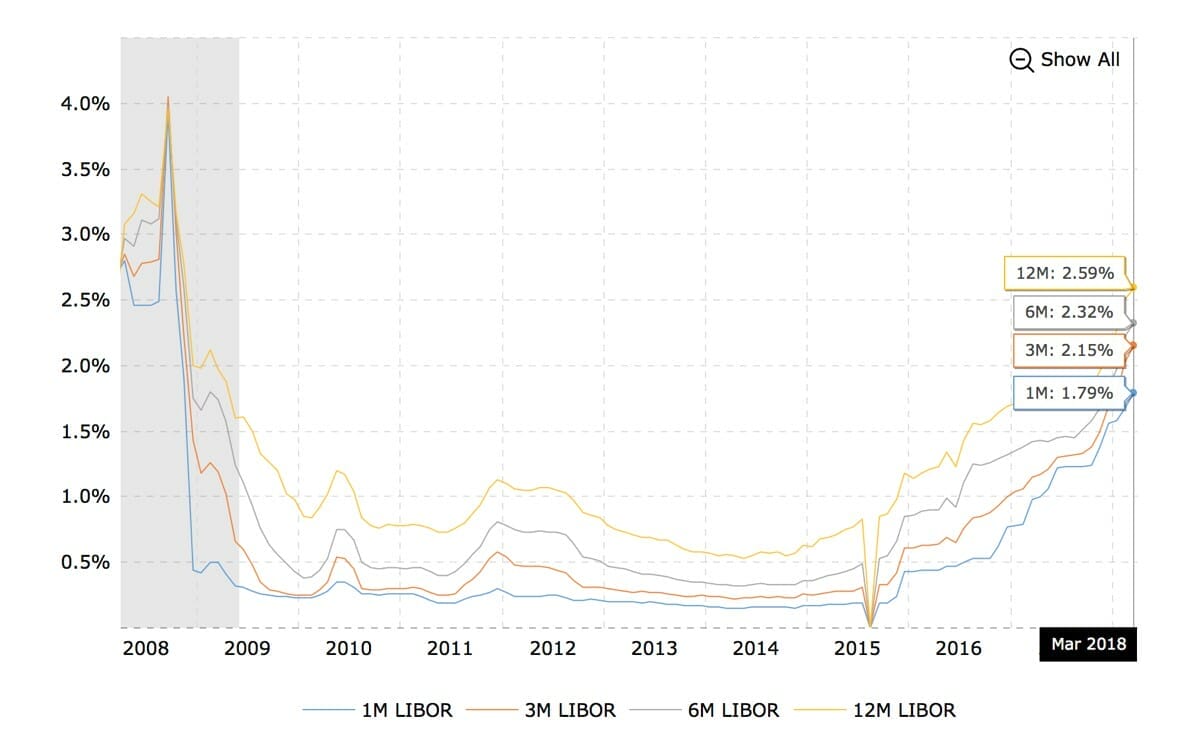

Alarm bells should be triggered by recent moves in the Treasury Inflation-Protected Securities (TIPS) market and the recent blowout in the London interbank offered rate (Libor) and the Libor-Overnight Index Swap spread, which has more than doubled since January, to levels last witnessed during the GFC. These are signs that monetary policy has tightened considerably and that rising rates for private borrowers may be a bigger concern than the more hawkish, but well-flagged, stance many central banks have adopted.

The three-month London interbank funding rate, which some of the world’s leading banks charge one another for short-term loans, rose to 2.27 per cent recently, the highest since 2008.

Putting aside the impact on investor sentiment, the rise in LIBOR will make funding more expensive, including for Australian banks which are on track to experience their biggest monthly funding cost increase in nearly eight years.

Growing nervousness in credit markets will add to the stress associated with trade tensions and talk of inflation and tightening monetary policy.

Figure 2: Five-Year TIPS

Figure 3: Libor Rates

Could it be that reversing quantitative easing (via quantitative tapering) triggers considerably more volatility in both stocks and bonds in the months ahead? It’s certainly true that as cost-of-capital assumptions increase, opportunity-costs rise, earnings multiples contract and highly leveraged businesses confront credit stress.

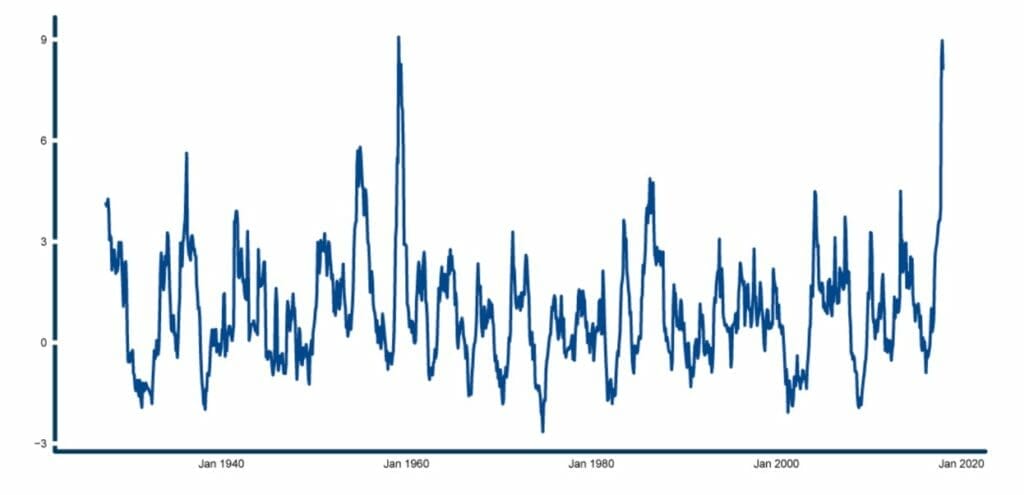

Figure 4 shows the 12-month annualised Sharpe Ratio and reveals that the recent extreme version of high returns combined with low volatility in the S&P 500 is an anomaly that has been seen only once previously, in the 1950s. In any event, the chart shows that a combination of higher volatility and lower returns is more normal and is likely to return.

Figure 4: 12-month annualised S&P 500 Sharpe Ratio to Dec 31, 2017

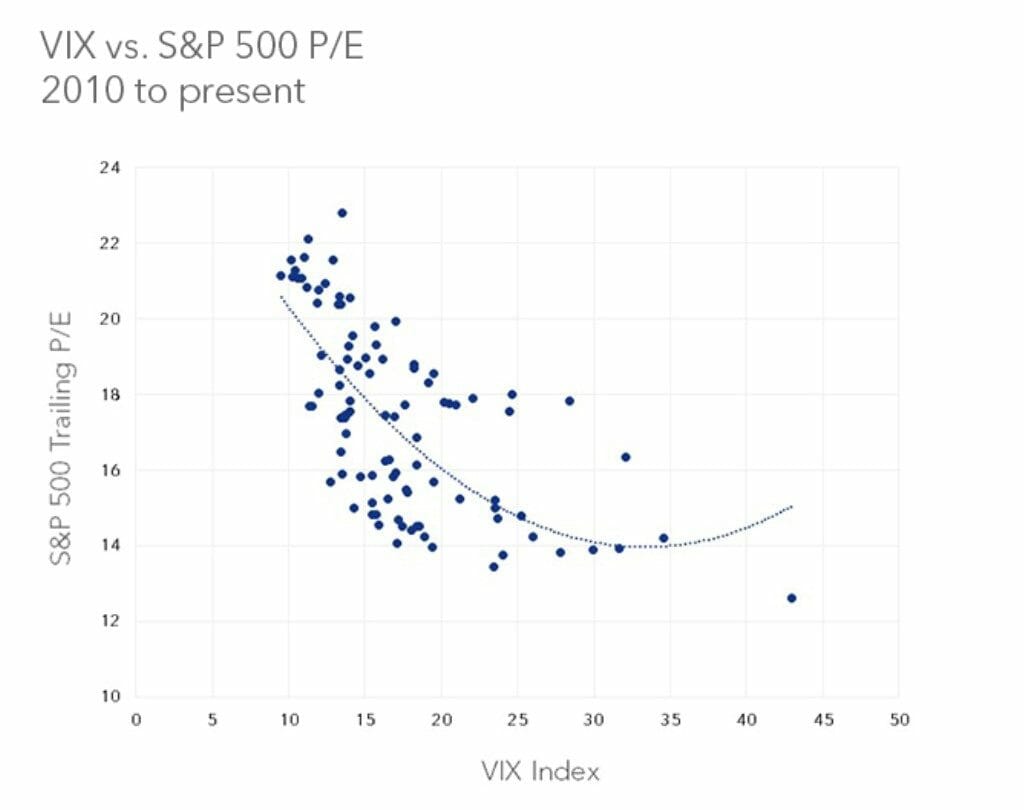

Finally, Figure 5 shows that when volatility (risk), as measured by the VIX, picks up, price-to-earnings multiples contract. Investors are simply less willing to make optimistic assumptions about a company’s prospects, and are, therefore, less willing to pay higher multiples, when fear of loss replaces the fear of missing out.

Figure 5: Volatility vs P/E Ratio, S&P 500

The evacuation of bond investors from corporate credit markets is, at the least, likely to produce an increase in volatility in equities. This elevates the compensation investors require, which is reflected in lower earnings multiples. If funding costs continue to rise, a reappraisal of required returns may lead to even further volatility, which feeds a cycle that produces the kinds of market action for which many investors aren’t prepared.

Value investors may find the baton of superior returns handed to them from higher-risk momentum investors.

Leave a Comment

You must be logged in to post a comment.