Anyone who has been involved in markets longer than 10 years has seen this before – stocks just going up.

Typically, in a bull market, we hear the refrain ‘Buy the Dips’. But even that’s impossible at the moment because there are no dips! Each morning, every morning, we wake to the news that the Dow Jones is up a quarter of a per cent…again.

As Chart 1 and Chart 2 reveal, since October 2016, the S&P 500 has displayed only one-way traffic. The index rises interminably and volatility continues to decline, and that’s despite fake news at Facebook, the incineration of cash at Tesla, Russian interference in US elections, Chinese debt issues, the threat of nuclear attack and even missiles flying over Japan. Every day, the market just keeps going up.

There are more than a dozen companies on the Nasdaq 100 – companies like Netflix, GoDaddy, Yelp and Salesforce – that are trading on multiples of more than 200 times earnings. The Bank of International Settlements (BIS/Oxford) has observed that there are now more margin loans supporting the US sharemarket than there were during the technology boom of 1999/2000. The collective market value of Tesla, Uber and Twitter is US$140 billion, yet their collective profit is zero. In Australia, when I have asked analysts to explain their reaction to seeing that a loss-making company with an app that helps individuals move their electricity bills over when they move house has a market cap of almost $750 million, they simply shrug their shoulders and point out it’s “pre-revenue”.

Bear market history

But perhaps most concerning is the warning from Robert Shiller, whose recent essay for Project Syndicate titled The Coming Bear Market? asks, with the US sharemarket characterised today by a seemingly unusual combination of very high valuations, following a period of strong earnings growth, and very low volatility, “What do these ostensibly conflicting messages imply about the likelihood that the United States is headed toward a bear market?”

After defining a bear market as a decline of 20 per cent or more within a year of the prior peak, Shiller observes there have been 13 bear markets in the US since 1871. Shiller noted market peaks followed by bear markets in 1892, 1895, 1902, 1906, 1916, 1929, 1934, 1937, 1946, 1961, 1987, 2000, and 2007.

Shiller then compared current market conditions to those that existed prior to the historical bear markets.

He observes that the CAPE (cyclically adjusted price earnings) ratio tends to rise before a bear market. Since the year 1871, the CAPE ratio has exceeded today’s level of 30 only twice – once in 1929 and again in 1997-2002. And in the peak months before 10 of the previous bear markets since 1871, the average CAPE ratio was higher than the overall average, as it is today.

Analysts and market commentators note that today’s historically high CAPE ratio is probably due to the strong earnings growth of 13.2 per cent from the second quarter of 2016 to the second quarter of 2017.

Any comfort gleaned from this strong earnings growth is quickly dispelled, however, by Shiller’s observation that, “peak months before past bear markets also tended to show high real earnings growth: 13.3% per year, on average, for all 13 episodes” adding “the market peak just before the biggest ever stock-market drop, in 1929-32, [recorded] 12-month real earnings growth [of] 18.3%.”

And those analysts who point to near record-low levels of volatility as protection against a bear market should heed Shiller’s observation that “stock-price volatility was lower than average in the year leading up to the peak month preceding the 13 previous US bear markets”. He adds, at “the peak month for the stock market before the 1929 crash, volatility was only 2.8%.”

Shiller concludes “…my analysis should serve as a warning against complacency. Investors who allow faulty impressions of history to lead them to assume too much stock-market risk today may be inviting considerable losses.”

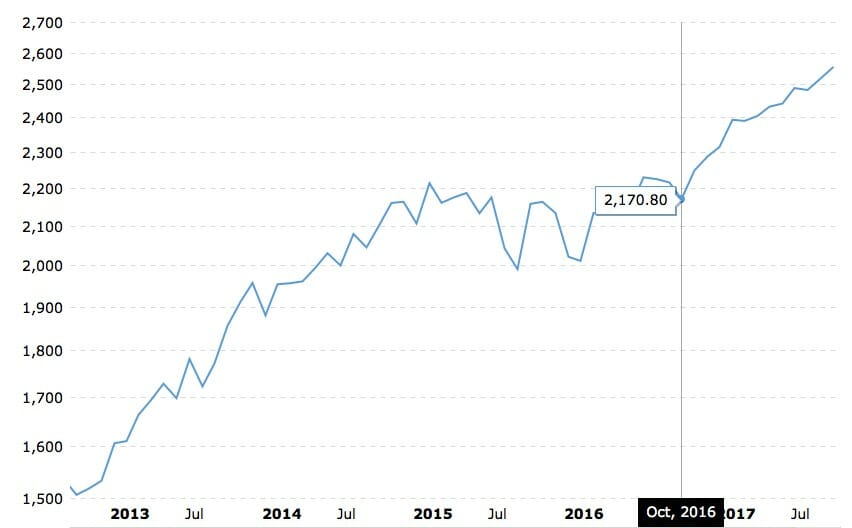

That the market has a head of steam about it is best revealed by a simple picture of the S&P 500’s advance.

Figure 1. S&P 500 melting up

At its current level of 2559.0, the S&P 500 has exceeded all forecasts made at the start of the year by US analysts surveyed by CNBC. Indeed, at the end of 2016, RBC senior equity strategist Jonathan Golub was the most bullish, with a forecast of 2500 points by the end of 2017. In June, Golub raised his forecast to 2600 points and Morgan Stanley now has an estimate of 2700.

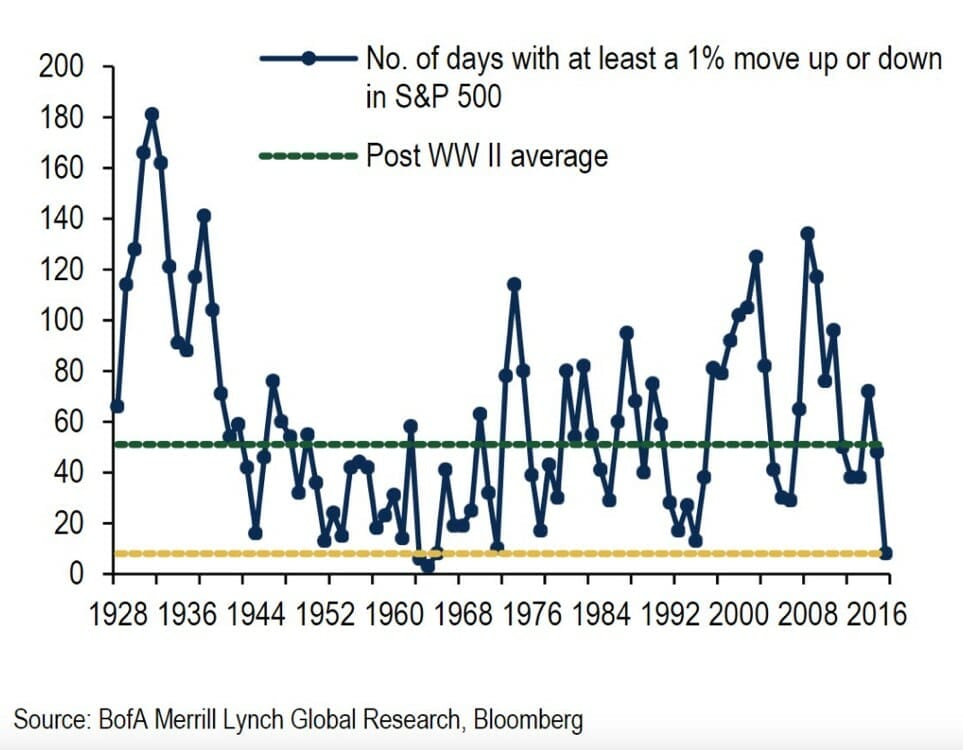

Figure 2. Volatility crashes (number of days in a year S&P 500 moves more than 1%)

Another curious observation is the rapidity with which the market recovers from major macroeconomic setbacks or catalysts. JP Morgan observed that while the market took 65 days to recover from the 2015, exchange-traded fund-inspired flash crash, the market took only five days to recover from Brexit and just 16 hours to recover from Trump’s victory.

The incessant rises and the absence of any meaningful pullback have also produced a curious, if not welcome, giving up by value investors.

Throwing in the value towel

In June 2017, Goldman Sachs issued a report titled, “The death of value?” It noted the strategy’s declining effectiveness, noting that implementing a value investing approach that went long the stocks with the lowest valuations and short those with the highest valuations would’ve resulted in a cumulative loss of 15 per cent to investors over the last 10 years. Following the release of the report, CNBC proclaimed, “The investment strategy pioneered by Warren Buffett is in crisis”.

Even Warren Buffett and Charlie Munger appear to have changed their value investing tune and seen the error of their ways! In an interview at the Daily Journal Corporation’s annual general meeting, in March this year, Munger answered a question about Berkshire Hathaway recently buying airlines, Exxon and Apple. He observed: “Do you know why Warren bought Exxon? As a cash substitute! He would never have done that in the old days! That’s a different kind of thinking from the way Warren came up. He’s changed…And I think he’s changed when he buys airlines and he’s changed when he buys Apple. Think about the hootie we’ve done over the years about buying high tech: ‘we just don’t understand it’; ‘It’s not in our circle of competency’; ‘The worst business in the world is airlines’… and now we appear in the press with…Apple and a bunch of airlines! I think we’re adapting to a business [investing] that has gotten much more difficult.

Another feted value investor who appears to have thrown in the towel is Jeremy Grantham, who voiced his concerns about value investing in his first-quarter 2017 letter to investors. In it, he stated: “This time seems very, very different,” admitting that the rules of value investing may no longer apply.

Finally, I have observed an increasing incidence of comments, from otherwise moderate market observers, that interest rates and inflation may not emerge again. If such forecasts prove prescient, lending your money for 100 years to Argentina (a country that has defaulted several times in the last 90 years) at 7.29 per cent – or just a few per cent above the rate at which you would lend money to the US Government – makes perfect sense.

There’s only one problem. It only makes sense in a world of relative value. By that, we mean, for example, stocks in aggregate are cheap, only when compared with bonds.

To explain, follow this example: Buying a US 10-year Treasury bond that is yielding 2.33 per cent a year, is the same as paying 43 times earnings. And because a bond coupon does not grow, the investor is, in effect, paying 43 times earnings for an income stream with no growth. Therefore, any stock that offers growth, with a PE of less than 43 times, is deemed cheap.

But in a world of attractive relative value, the value is ephemeral. If interest rates climb, the ‘value’ vaporises!

FOMO usurps fear of loss

Having interest rates close to zero for an extended period of time fuels a migration out of cash and into income-producing assets. Unsurprisingly, in Australia, we have seen strong rallies in ‘bond proxy’ stocks in the infrastructure sector, such as those for airports and roads.

Like a plague of locusts feeding on a field and moving on, investors chasing yield continue to suffer at the hands of classic yield traps such as Seven West Media, David Jones and Myer between 2012 and 2014, Monadelphous and WorleyParsons in 2015, BHP, Woolworths and Origin in 2016, and Telstra in 2017, all of which cut their dividends on migratory yield chasers.

As those investors suffer burns, or prices move even higher, investors move further up the risk spectrum. By way of example, Howard Marks described the boom in tech stocks as “the pursuit of the new, untrammelled by knowledge of the past”. In other words, investors buy that which has no history. If you cannot see the risk, it cannot be priced in. So just when risk seems the lowest, and investors fear only the fear of missing out (FOMO), risk is actually the highest.

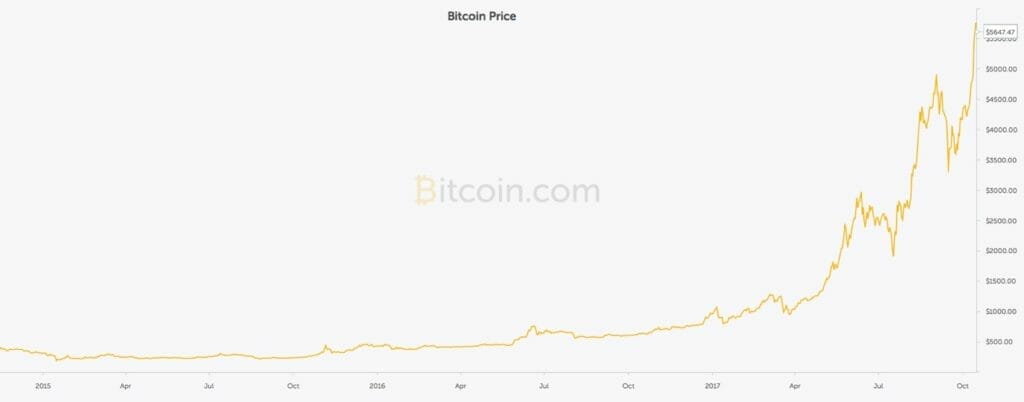

And even further up the risk spectrum is the cryptocurrency Bitcoin. While Jamie Dimon says central banks will “crush it”, and news reports suggest exchanges can be hacked and that they’re the preserve of cowboys and drug smugglers, others suggest digital currencies have all the characteristics required to be considered money, including uniformity, divisibility, portability, durability, limited supply and acceptability. Regardless of who is right, the price ascent, shown in Figure 3, is another sign that investors/speculators are willing to risk everything to make a dollar – even if it’s a cryptodollar!

Of course the icing on the cake must be the taxi and Uber drivers asking me whether they should invest in Bitcoins!

Figure 3. Bitcoin’s ascent

If interest rates remain low for long enough, as they have, the fear of missing out usurps the fear of loss, and rising prices feed on themselves. To some extent, that is what appears to be happening now, and the record prices for assets that produce no income, such as the new highs for collectible cars, works of art, and even diamonds and watches, is symptomatic of that.

While conditions remain benign, volatility, inflation and interest rates stay low, and the market continues to surmount all concerns, those troublesome factors can be ignored and thus cease to exist. But when the market reverses (and keep in mind that could be some years away), those concerns will be remembered as harbingers of something dire. Commentators will look back on today and note all the precedent conditions were ‘obvious’. They may also represent a lesson lost on those who chose to ignore them completely.

Leave a Comment

You must be logged in to post a comment.