We’ve all heard more about fake news than we ever wanted to, but is there something similar circulating in economic news? At the end of August, the important US Confidence Board consumer confidence reading was released. As on most days, I checked my apps for Bloomberg and CNBC – two business services for which I have much respect.

One had a header something like ‘Second best consumer confidence level in 12 months’. That sounded quite good, but not special. The other service led with ‘Second best consumer confidence level since 2000’. A real attention grabber! Both headlines were true. It’s just that the best happened to be a little earlier this year. So did the best “in 12months” lead deliberately set out to underplay the economy’s hand?

Then I got to thinking about how one of these services a month before called a China PMI of 91.3 as a ‘miss’ because 91.4 was expected. Well the 91.4 was subject to sampling error if nothing else. Isn’t that just an ‘on expectations’ result? After all, a number greater than 50 shows that growth expectations – and not levels of output – are improving. I think headlines have started to get worse as we’ve started to run out of big headlines to do with major problems such as the European Banking Crisis, predicted US recessions, etc. Can news wires not just sit quietly without muddying the waters while we take a few months of no bad news?

In Chart 1, I show the ASX 200 reaction to whatever has been going on in FY17 and since. I’m not one to talk about so-called technical analysis. The arbitrarily selected dotted lines at 5650 and 5850 I have added show that the market has been stuck in a rut for some months. To be more rigorous, I checked back from the start of the S&P/ASX 200 index in 1992 and the latest run is the tightest range (in percentage terms) on record – defined by a trailing three-month window’s difference between the maximum and minimum (in logs). It is a new phenomenon. But will it continue?

Chart 1: S&P/ASX 200

Source: Thomson Reuters Datastream

At the time of writing, we’d just finished the August reporting season and newswires wrote of lacklustre results and the like. We did have a few major casualties in Telstra, Commonwealth Bank of Australia and Harvey Norman inter alia, but most companies (58 per cent) reported on expectations. I found that my calculations on broker-based forecasts of earnings and dividends made for some far more interesting study. The individual company broker forecasts are not attention grabbers and are guided by company statements that follow continuous disclosure rules. I think they are unbiased.

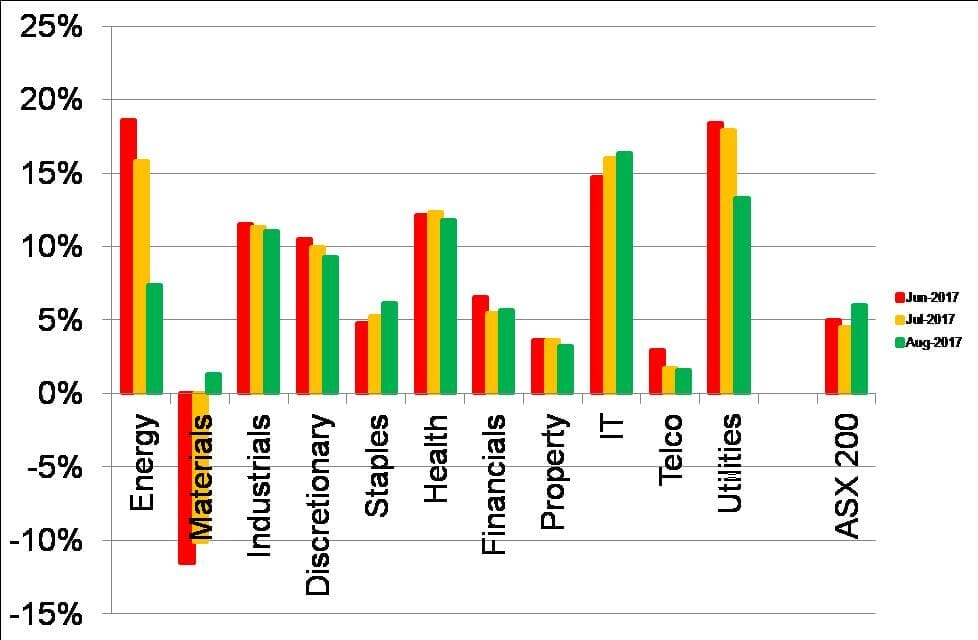

In Chart 2, I’ve shown the end-of-month, 12-month-ahead forecasts by sector. I calculate for each of the last three months. The end of June and July forecasts are reasonably similar mirroring the lack of key news during July. The end-of-August forecasts incorporate what the brokers made of the August reporting season.

Chart 2: Sector 12-month capital gains forecasts for the ASX 200

Source: Thomson Reuters Datastream & Woodhall Investment Research

The forecasts tend to evolve slowly in between releases of big bites of information. Materials forecasts had been negative for all of 2017 up until August. Did it just take them that long to realise that, yet again, people read too much into commodity price volatility and over-react?

The Energy forecast more than halved during August and Materials turned slightly positive. Prices in the Energy and Materials sectors had already jumped the gun, with capital gains of +5.0 per cent and +4.1 per cent in August.

The Utilities forecast also came down but the other August forecasts are largely in line with those made in June and July. Of course, with reporting season having just finished, further updates might continue to take place during September. The October forecasts will produce a good platform on which to consider a major rebalance of at least my portfolios.

The net result is that the ASX 200 forecast improved from 4.5 per cent to 6 per cent based on August reporting. I believe that investors – whether because of being bombarded with fake news or not – have not yet been game to attack 6000 again. Eventually, the underlying strength of the market must be recognised. It seems to me that the next change will be up and strong – unless, of course, North Korea does something stupid.

Leave a Comment

You must be logged in to post a comment.