It seems that whenever markets hit new highs, someone starts talking about bubbles. The story du jour seems to be about the IT sector on Wall Street; which gave rise to a dotcom bubble that burst around the turn of the millennium. The sector, however, was a different beast back then. Now we have IT giants such as Alphabet (Google), Amazon, Facebook and Netflix – the so-called FANGs – dominating the scene.

It is hard to value any company and it is even harder when it has been on a steep growth trajectory. If these companies continue to deliver, there should be no risk of a new bubble. But how do we know if they haven’t already got so far ahead of themselves that danger lurks around the corner?

Since 2005 I have been calculating a measure of mispricing, called exuberance, for the ASX 200 and its 11 sectors. In 2010 I expanded the list to include the S&P 500 and its 10 sectors. The basis of all of the mispricing signals is to compare actual growth in the indices to my forecasts based in turn on broker forecasts of dividends and earnings. If actual growth is running faster than projections, the index is growing over-priced and vice versa.

I established a rule in 2006 that 6 per cent was a trigger point. That is, if any sector’s exuberance exceeded 6 per cent in overpricing, a correction of 6 per cent to 10 per cent was imminent – or there would be a prolonged sideways movement until the fundamental price implicit in these calculations grew to erode the overpricing.

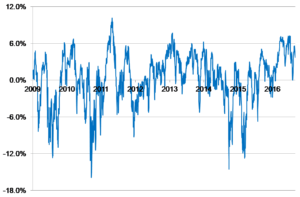

I have often written on this topic over the years for this magazine. This time I shine the spotlight on the IT sector of the S&P 500. The mispricing signal is shown in Chart 1. Note that exuberance rarely exceeded 6 per cent for more than a few days at a time. The one time it was above the trigger point for an extended period (from February 9, 2012 to April 17, 2012), the IT index fell from a high of 502 points to a low of 437 points on June 1, 2012 for a 12.8 per cent correction. All of these calculations are made at the close of each day’s trading and not subsequently revised

Source: Thomson Reuters Datastream and Woodhall Investment Research.

More recently, exuberance went above 6 per cent on February 16, 2017 and, except for two short dips below 6 per cent in April and May, stayed there until June 8, 2017. By the time the exuberance reached fair value (at 0 per cent) on July 3, the sector had corrected with a fall of 5.4 per cent.

So I agree that, from time to time, the Wall Street IT sector runs a bit hot but it behaves in a similar fashion to other sectors in the S&P 500 and those in the ASX 200. But are these bubbles? Strictly speaking, the short-term exuberance I show in Chart 1 is indicative of a bubble but most people would, at least implicitly, distinguish between mini-bubbles that burst with, say, a 5 per cent correction and those that end in tears. I see nothing in current conditions to make me nervous. However, if we were to get an extended period above 6 per cent exuberance like we witnessed in 2012, I might exercise some caution.

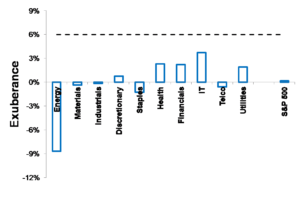

In Chart 2 I show a snapshot of exuberance across sectors at the end of July 2017. No sector, and certainly not the broader index, gives me any cause for concern. So would I buy the index at these prices? Well, I did put my harvested dividends to work in mid July in an ETF for the iShares Global 100 (IOO) but I wouldn’t have bought the IT sector on that day.

Chart 2: Exuberance across sectors in the S&P 500 at end of July 2017

I prefer to use my mispricing measure to avoid buying when a sector is expensive and to buy when a sector is cheap. Of course, if I am rebalancing by selling one stock to buy another, it is fine to do so if both are similarly overpriced. Better still is to sell overpriced sectors to buy underpriced when that is consistent with one’s bigger plan. It doesn’t always work but this method seems more reliable than taking a shot in the dark.

Leave a Comment

You must be logged in to post a comment.