While nobody enjoyed the recent sharemarket sell-off, Ron Bewley thinks his June 30 index forecast is still solid.

There is no doubt that September was not a good month for share investors in Australia. Fuelled by crises in Ukraine and Iraq-Syria, weaker iron ore prices, and talk of changing the regulation of banks, the ASX 200 fell about 6 per cent. So are we back to the bad old days?

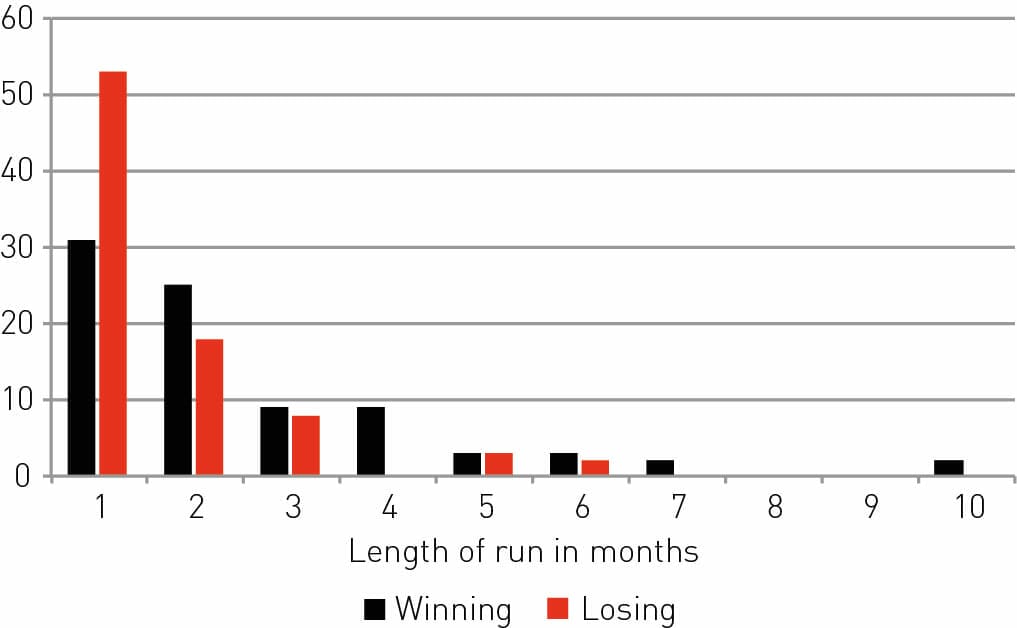

To put September into perspective, I took monthly data on the index since mid-1985 to the end of September this year (351 months) to see how long past “losing streaks” have lasted.

In 60 per cent of the months, the monthly return was positive and in 40 per cent of the months the return was negative. In Chart 1, I show the losing and winning streaks in different colours. A losing run (red) ends when a sequence of losses is followed by a gain – so it can be seen, for example, that in 53 (left-most red bar) of the 351 months, there was a losing streak of one month followed by a positive month. On the other hand, in 31 cases, there was a winning streak (black) of one month followed by a loss.

The average length of a winning streak is 2.5 months and the figure for losing streaks is 1.7 months.

Clearly, the two 10-month winning streaks (ending in 2005 and 2007) have a big impact on the average durations.

August this year was slightly negative, and July was positive, making the current run (August-September, at the time of writing) a two-month losing streak.

From Chart 1, I calculated that 58 per cent of losing streaks lasting two or more months were exactly two months, so only 42 per cent extended beyond two months. If October also turns out to be negative, the probability of the sequence being extended is 38 per cent – based on past data.

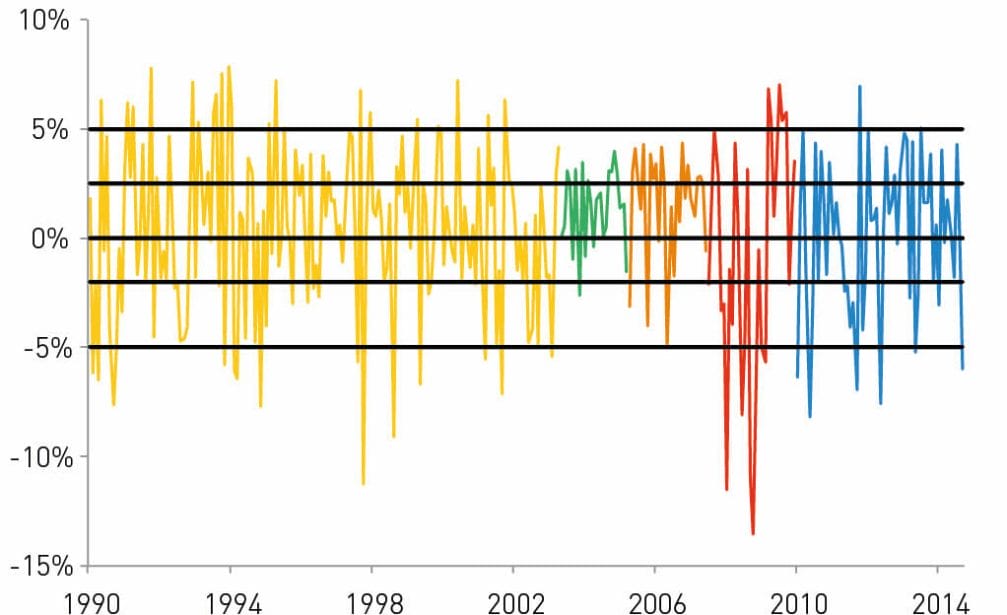

The length of the sequence tells us nothing of the extent of the gains or losses. In Chart 2, I show the monthly returns.

I start the chart in 1990 to eliminate the massive loss in October 1987. I have colour-coded the returns into different regimes that I have used in the past. Red denotes the global financial crisis (GFC) and brown a particularly benign period in 2003-2005. The horizontal black lines (arbitrarily) denote ±2.5 per cent and ±5.0 per cent for visual reference.

While nobody (except short sellers) enjoyed the recent sell-off, it is quite clear from Chart 2 that nothing unusual is happening. Market volatility and the S&P/ASX VIX index (ASX code XVI) are at the low end of normal.

Our broker-based forecasts for the market are strong. Barring major escalations in geopolitical situations, an orderly return to a good market might be expected. Our June 30 forecast for the index is solid at 5900.

Leave a Comment

You must be logged in to post a comment.