Angus Crennan says the twin challenges for advisers are articulating investment opportunities while managing client fear and greed are more complex than ever before.

“It may be that buying the 10-year US bond at 4.5 per cent right now turns out to be one of the best trades for years to come.” A great quote from Rory “Rate Cut” Robertson at Macquarie Group’s internal debt markets’ morning meeting in mid-2007.

How far we have come since 2007. The US 10-year bond has been bid up so much that its yield reduced to 1.76 per cent at the end of 2012. Investors who went against the grain in early 2007 and took some money from strongly performing equity markets and shifted to more defensive bonds would have done well.

Early this year we have seen “rotation thinking” come back into play, with investors rightly questioning their portfolio allocations and many commentators asking whether a rotation from defensive asset classes back to equities was looming. According to Bloomberg, even some central banks, concerned with extreme valuations for traditional reserve assets, are now considering adding a sleeve of equities to official reserve investments.

Rotation thinking

Here is a simplified version. Unprecedented monetary stimulus from the world’s most powerful central banks has significantly benefited fixed interest investors and prices have increased to the point that bond yields have fallen to generational lows. Would the removal of that stimulus see the high price of bonds fall? If so, in order to capture and lock in the gains to their bonds, investors would be incentivised to sell bond investments and shift the funds into other investments.

Those who have worked with brokers know that pitching transactions to a client that already believes they need to do something is often successful. This is because it’s at market extremes that behavioural finance comes into its own. We are human and our capital markets are products of our fears and greed.

Of course it’s very hard to do better than a herd when you’re part of that herd. Taking capital away from glamour sectors, especially when they have done well, and investing where capital is scarce (when those sectors have been sold off) is emotionally hard because it usually either feels like you are leaving gains on the table or catching a falling knife.

Opportunity in Australian small companies

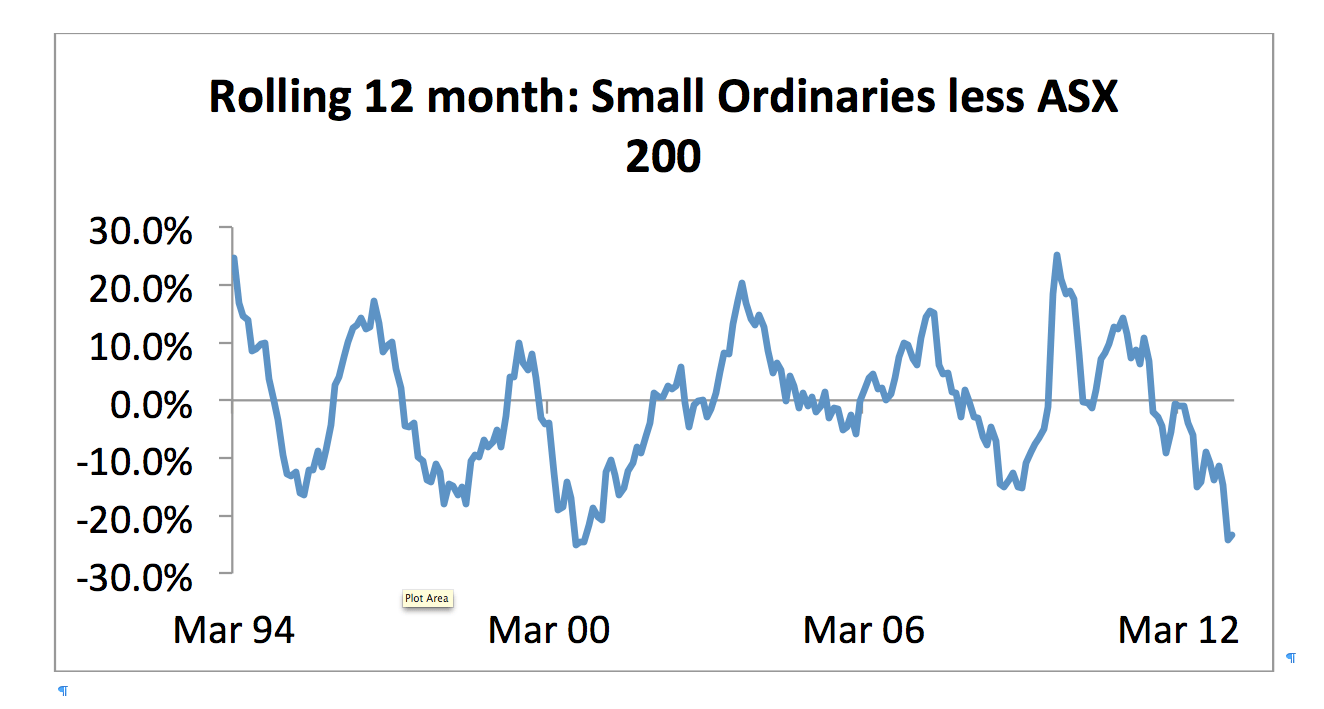

One sector that has been out of favour with investors recently is small companies. Looking at the chart below, it’s immediately apparent that the lag in 12-month performance of small companies versus the ASX 200 is historically as extreme as it gets. Diving deeper into the data reveals even more information, such as the market’s broad disregard for small resources, even the best placed ones.

Source: Bloomberg

This history is telling. Not only have small caps “caught up” their relative performance deficit to large caps, they usually then go on to outperform in a relative sense. Further, the sector seems to do this with a surprising degree of regularity. If you were a technical trader looking at this graph, you would be smiling.

For advisers, the twin challenges of articulating investment opportunities while managing client fears and greed have always come with complexity.

Tactically, the market has largely ignored smaller companies while pushing some of our large caps to all-time highs. Yet history makes it hard to have a view that divergence of performance will be maintained.

For forward-looking investors the message is clear. While going against the grain might feel difficult, for investors with a reasonable time horizon, history tells us there is an opportunity here.

When small companies do start to close their performance deficit, whatever the catalyst for that change in sentiment is, having exposure via a quality manager has the potential to contribute significantly to the portfolio achieving the client’s investment objectives.

Angus Crennan is an investment specialist at Zurich Investments

Leave a Comment

You must be logged in to post a comment.