Van Eyk’s Jonathan Ramsay recently warned that new guidelines for financial products could potentially lead to big losses for investors if they encouraged the industry to take a shallow approach to risk management. He argues that ASIC’s Regulatory Guide 175 could result in poor outcomes if it encourages the industry to fall back on investment benchmarks as justification for putting clients in particular asset classes. Professional Planner asked Ramsay what regulatory reform means for balanced fund investors.

At van Eyk’s annual conference in March, we polled an audience largely consisting of financial advisers on whether their investment promises to clients were absolute or relative. That is, were they promising to target returns better than inflation or were they promising the investments they recommended would perform well compared to their peer group? The implicit assumption in the latter approach is that the peer group moves in a way that matches investor risk preferences with a suitable asset mix.

Interestingly, the audience was pretty much split down the middle on the question.

Depending on investment goals

Either approach can be legitimate depending on the investment goal. On the one hand, absolute outcomes are ultimately the most important for individuals, with capital preservation becoming ever more important as more people enter the retirement phase. On the other hand, changes to industry regulation (specifically ASIC Regulatory Guide 175) can only increase the emphasis on benchmarking and peer group comparisons.

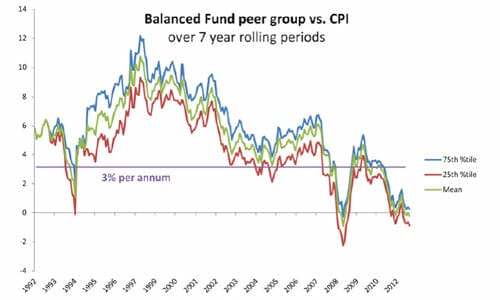

During some market periods, the difference between the two approaches is not great, however, sometimes they can be very much at odds. The chart shows that the experience for balanced fund investors has swung between feast and famine, with the whole peer group running well ahead of inflation through the early 1990s, while the last decade has been a story of persistent disappointment in absolute terms.

This suggests that, as an adviser you may spend long periods either soothing clients’ nerves (when returns fall behind inflation) or trying to keep up with the Joneses (when the peer group performs strongly in real terms). Our research indicates that your starting point is very important and that an equity-heavy mix of equities of bonds can be expected to outperform inflation by 3 to 4 per cent –only if starting yields for equities are reasonable.

Intelligent diversification

From that perspective, the prognosis for the next 10 years is actually OK for balanced investors, although bond-heavy conservative portfolios could still struggle to meet their more moderate and shorter-term objectives.

Source: van Eyk

Yet, if we are moving towards a world where the performance against the peer group and absolute returns will both be imperatives for advisers and investment managers, how are they to be reconciled?

One way is to smooth out the gyrations in portfolio performance through more intelligent diversification (including the use of alternatives) and a rigorous monitoring of valuations so portfolios can be positioned realistically given the yields and growth prospects on offer. This has been a strong focus in portfolio construction at van Eyk.

Jonathan Ramsay is head of asset consulting and strategic research at van Eyk Research

Leave a Comment

You must be logged in to post a comment.