Super Consumers Australia has identified significant discrepancies in the results provided by retirement calculators offered by super funds and has called on the government to step in and deliver free and independent information that members can rely on.

Despite promises by super funds to help consumers prepare financially for retirement, research from the consumer advocacy organisation found retirement calculators have been failing members by providing flawed guidance.

SCA chief executive Xavier O’Halloran and deputy director Katrina Ellis will explain in a column in the inaugural Retirement Magazine, a sister publication of Professional Planner, how they believe this problem can be rectified.

The solution to the issue of poor retirement guidance by super funds lies in the hands of the government, SCA says.

O’Halloran and Ellis claim that, while the super funds are responsible, the government must take responsibility for the flawed and complex retirement system it has created.

While funds could certainly focus on making improvements, it would likely be a slow process with no guarantee of success. Instead, the government should introduce high quality retirement guidance which could include a more accurate calculator.

“Imagine if all the scattered government resources were brought together to form a one-stop-shop to assist Australians with retirement planning,” O’Halloran and Ellis say.

The pair suggest this could involve improving upon ASIC’s existing Moneysmart website, an already popular and trusted resource with consumers. At this year’s Retirement Conference, a joint initiative of Retirement Magazine publisher Conexus Financial and The Conexus Institute*, ASIC reported Moneysmart’s super and retirement section was accessed by over two million Australians.

The average person needing to figure out how much money they will need for retirement, but not able to afford the services of a financial adviser, might turn to digital options such as retirement calculators to assist them.

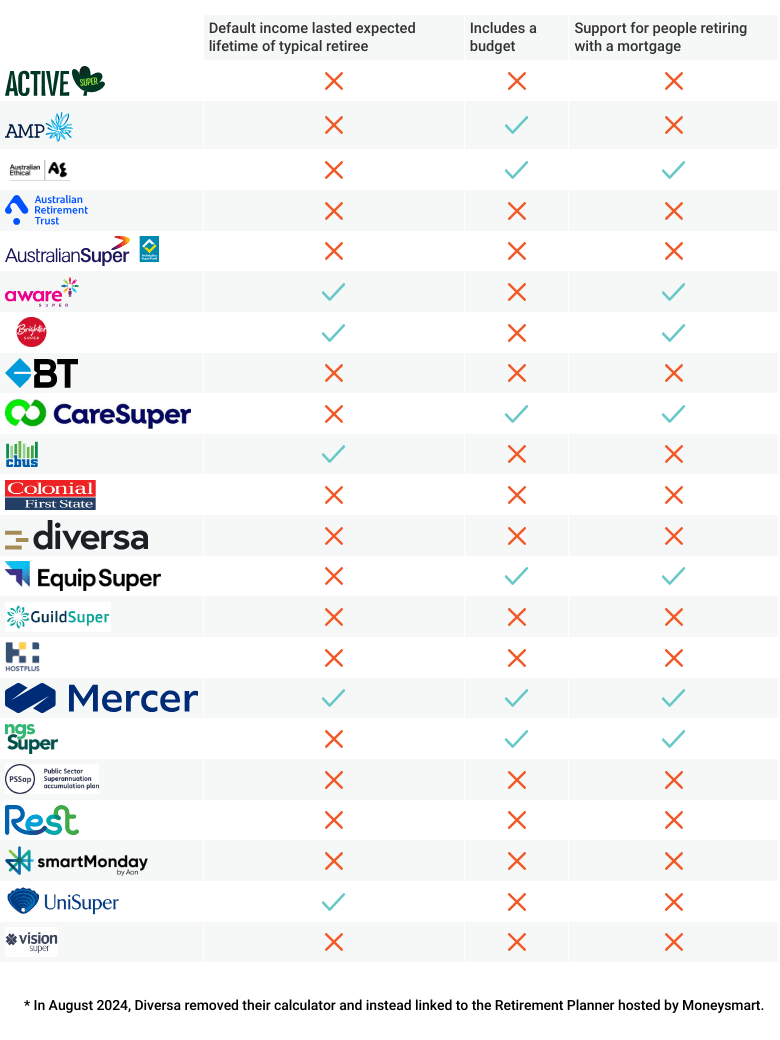

To understand the failings of retirement calculators, SCA put funds’ current offerings to the test and discovered that only half of the 50 biggest funds had publicly available calculators and a further eight simply sent people to the ASIC Moneysmart calculator.

Breakdown of super fund retirement calculators

Source: Super Consumers Australia

Some 77 per cent of calculators were found to have adopted a one-size-fits-all model and to make arbitrary in-built assumptions. As a result, the calculator recommends a default income that is either too high and runs out before the expected life expectancy of the member; or too low, leaving a substantial sum untouched at the time the member reaches 100 years of age.

O’Halloran and Ellis refer to this range of outcomes as “dud guidance” and “out of line with the purpose of super” for anyone except children, who will inherit what’s left in a find, or for those few members who live to 100.

The calculators fail to recognise differences between people’s personal situations, which have a huge impact on what retirement will look like for them.

“People’s circumstances are different, and these differences have big impacts on their capacity to save and their spending needs in retirement,” SCA says.

This is especially clear when it comes to the home and the difference between ownership and renting, with renters having higher spending needs.

“Some will own a home outright, be paying down a mortgage or renting, some will be single, some in couples,” SCA says.

Despite this, 73 per cent of retirement calculators did not ask if the person had a mortgage.

Medical and care expenses are also a major factor as well as life expectancies.

Retirement calculators do not account for these personal differences and hence provide inappropriate and inadequate guidance for retirement.

O’Halloran and Ellis describe the flaws of the retirement calculators as “concerning” and displaying a “complete lack of personalisation”.

*The Conexus Institute is an independent think-tank philanthropically funded by Conexus Financial, the publisher of Professional Planner.

For more information, follow Retirement Magazine on LinkedIn or sign up to our mailing list.

Leave a Comment

You must be logged in to post a comment.