It wasn’t that long ago that employers had all the power.

They dictated employment terms and conditions with little regard for the satisfaction and preferences of employees and potential employees.

But the tables have turned. Today, employees are in control.

The Covid-19 pandemic has prompted people to re-evaluate their life, resulting in many changing the way they work.

In the United States, this has led to the economic phenomenon known as the great resignation, where employees voluntarily quit their jobs en masse in 2021, citing hostile conditions, limited career opportunities and lack of meaning.

Australia is experiencing its own version of the great resignation. Almost 10 per cent of Australian workers, or 1.3 million people, quit their job in 2021, according to the Australian Bureau of Statistics.

An ABS survey conducted in mid-2022 also found 31 per cent of businesses are struggling to find staff.

And it’s not just cafes and airlines being impacted.

Accounting and financial advisory businesses are experiencing challenges too.

CPA Australia Chief Andrew Hunter recently described the skills shortage crisis in accounting as “critical”, citing a 34 per cent increase in job ads for accountants in FY22.

Since the Hayne Royal Commission, job ads for financial advisers, paraplanners and compliance staff have also exploded, coinciding with tougher regulatory requirements and new education and training standards.

For the fortunate few who, whether by good luck or good management, are yet to suffer the loss of key personnel or the frustration of trying to hire a replacement on the same money, their dream run may soon be over.

Two million Australians are poised to quit their jobs in the next six to 12 months, according to a report by Allianz Australia.

Needless to say, every accounting and financial advisory business must have a strategy for recruiting and retaining talent. This is especially important for businesses with ambitious plans to be a fast growing firm of the future.

Growth hinges on a company’s ability to increase its capability and capacity to reach and serve clients.

Better systems, processes and technology play a role but people ultimately determine if a company achieves its goals and mission.

Hence the corporate cliché; employees are a company’s most valuable asset.

There are four main ways that businesses can access labour:

- Buy a business and acquire staff;

- Recruit staff either directly or via an agency;

- Home grow talent; and

- Outsource.

Inevitably, most SME business do all of the above. Regardless of your people strategy, at the heart of any HR and people strategy is a compelling employee value proposition (EVP).

This isn’t about big salaries and fancy titles; employers must take a holistic approach.

Good pay, fair entitlements and safe conditions are a given. Employers must also meet demands for flexibility, education and training, wellbeing, collaboration, access to management, career progression and fulfilment.

Increasingly, employees expect their workplace to be diverse, inclusive and socially responsible.

They want to be proud of where they work and they expect to their leaders to live by the company values they ascribe to. Brand is important.

Less important are perks like retail discounts, gym memberships and in-house catering, although they are considered nice-to-haves.

Across the spectrum of employee benefits, large companies have the jump on smaller firms.

Small businesses often talk up their close-knit, family culture and lack of bureaucracy but, in reality, they struggle with the same people and culture issues as larger companies only larger companies are in a stronger position to compensate.

They have a greater capacity to pay, offer bonus leave like mental health days and parental leave, and manufacture career opportunities.

Larger organisations also offer greater employee protections through formal systems, processes and policies.

While financial planning has successfully shed the cottage industry image, there are still only a small number of businesses of notable size and scale.

To compete effectively against other professions and industries for the best and brightest, advice businesses need to get much bigger.

To attract talent and secure growth, businesses inside AZ NGA are beefing up through a combination of M&A and organic growth, as part of a broader future firm strategy.

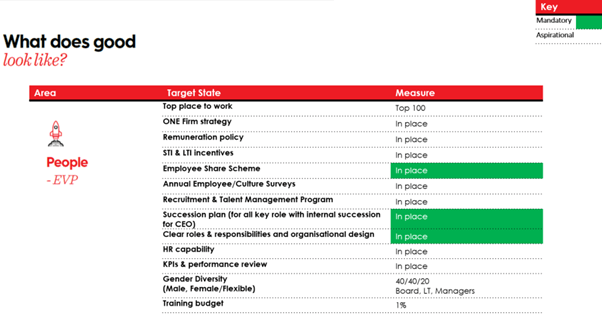

We believe leading advisory firms of the future must have five key components, starting with a cracking EVP. They also need a compelling shareholder value proposition, client value proposition, a defined enterprise architecture and a strong culture.

As part of future firm strategy, the table below outlines the components of a compelling EVP.

Source: AZ NGA

Advice and nightclubs

The war for talent isn’t a short-term trend.

Good people have always been hard to find and even harder to hold onto.

In the long-term, the introduction of higher professional, education and training standards will help the industry attract talent.

Ironically, higher barriers to entry may aide recruitment because the sector is more desirable.

On the other hand, low barriers to entry act as a deterrent for the skilful and ambitious.

It’s the reason why clubs with strict dress codes, steep cover charges and pricy drinks have the longest queues to get in.

High professional, ethical and education standards will see more of the right people enter the industry in the long term.

This applies not only to advisers but to every role from support staff to marketers to compliance professionals. There will be a contagion effect.

Firms of the future are getting ready to seize the opportunities.

Leave a Comment

You must be logged in to post a comment.