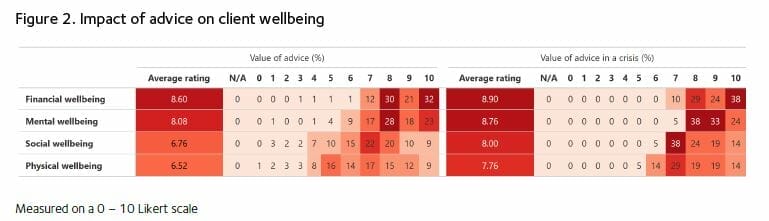

A ongoing study being undertaken at Griffith Business School has revealed how financial advisers see their role in crisis intervention, with most rating their advice as providing a positive impact across the financial, mental, social and even physical wellbeing of their clients.

The report, called The value of professional finanical advice for consumers in a crisis, involved surveys and interviews with advisers to understand their perceived role in helping clients through crises. Using the pandemic as a backdrop, the report sttes that the “crisis intervention” aspect of advice helps people when “familiar coping strategies” may be ineffective.

Helping temper clients’ reaction to market volatility is only the tip of crisis management iceberg for advisers, who routinely guide multiple clients through various crises simultaneously according to the report.

“Financial advisers regularly find themselves working with clients experiencing multiple crises simultaneously (both personal and market-wide), and often multiple times over the course of their client-adviser relationship,” the report states, adding that the advisers involved carry on this work without the benefit of social or medical training.

“Their role is complex, particularly when financial advisers may not be trained to face health crises like nurses, doctors and first responders, or social crises such as divorce, death of a loved one or loss of employment, like psychiatrists, psychologists, counsellors, and social workers.”

Another key finding in the report was that existing advice clients have a far better experience during a crisis than non-advised or those that are approaching advice for the first time.

Another key finding in the report was that existing advice clients have a far better experience during a crisis than non-advised or those that are approaching advice for the first time.

While strategic advice during a crisis is valuable on its own, trust within an existing client/adviser relationship means the “application, conveyence and assimilation” of technical information is quicker and more readily undertaken. This was especially so in the pandemic, when new clients seeking advice were perceived as “more anxious” and requiring more support than existing ones.

According to the report’s co-authors, research fellow Ellena Loy and program director Kirsten MacDonald, the report is part of a larger project designed to quantify the value of financial advice through academic rigour.

“There are many independent advice government documents and reports out there but none have done anything that’s more formal in terms of empirical research,” MacDonald says.

“A lot of those studies have a narrow focus on areas like returns but we wanted to take a holistic approach,” Loy adds.

The report is the second part of a three-part project that should take about seven years to complete. The first part focussed on the current framework of literature on the topic of financial advice, while the second part looked at advice through from the advisers’ point of view. There are five years left on the project, which Macdonald says will be dedicated to the third stage – client perspectives – and collating data.

While the data so far has been more qualitative, the authors reckon this third stage will result in more hard numbers linked to the value of advice.

“The numbers are going to come from the advisers and the clients,” MacDonald says. “At the moment it’s quite qualitative but the intention is to collect quantitative data over time.”

According to Loy, the standout finding so far has been that while the pandemic has brought the crisis management role in advice to the fore, it’s a part of the job that never really goes away.

“It was conducted during the first wave of the pandemic in 2020 so there was a focus on Covid, but we also spoke to advisers about personal crises their clients have experienced, including the loss of a job or a loved one, and a comparison to the GFC crisis,” she says.

“One thing that came out of that was advisers are always dealing with clients in crises.”‘

Leave a Comment

You must be logged in to post a comment.