It’s often the case in markets that the least expected occurs. At the market’s March nadir, for example, nobody predicted that even while the pandemic continued to worsen, within four months many stocks would not only have recovered but be trading at new all-time highs.

Much of that strength has been driven by optimism for technology companies. In many cases the thesis for buying technology makes sense; Microsoft for example will benefit from the increasing number of people working from home. The strength in many reputable and profitable technology companies is therefore confirmation of the belief that this pandemic will be around for much longer than current mainstream commentary seems to suggest.

But if that’s the case, is the stock market’s enthusiasm rational?

While the thesis for buying technology might be rational, paying any price to gain exposure to that theme is irrational.

Keep in mind that all booms start with a legitimate and credible thesis. As that thesis gains momentum, many less sophisticated investors jump aboard and eventually investors pile in not on the basis of the original thesis but simply because the shares keep going up. Eventually prices become so extreme they bear no relationship to reality and a bubble has formed. I believe we are there today, not for all stocks but for many in the technology space.

There is little doubt the rally in technology stocks has also been extended by a veritable tidal wave of debutante retail investor buying. In the US, for example, when shares in Hertz went on a five-fold tear after the company had announced it had entered Chapter 11 Bankruptcy, retail investors demonstrated either ignorance about the standing of an equity holder in the capital structure of a company, or indifference to it amid a desire to simply bet on the next day’s share price move – as one might bet on a cockroach race.

The rise in US technology stocks, and in particular Amazon, Tesla and Netflix, has seen Australian technology peers rise in sympathy. Today they are trading on revenue multiples that dwarf the levels seen during the tech boom of 1999 and early 2000.

For an insight into the real and present madness of crowds just take the Buy Now Pay Later leader, Afterpay. Its share price is up almost eight-fold since March, thanks in part to COVID-19 accelerating online and cashless retail sales, while government employment support programs both here and in the US ensured millennials were able to meet their repayment obligations to the company. Share price support was also aided by speculation of a takeover with the appearance of the Chinese company Tencent on the register.

Afterpay now has a market capitalisation of $19 billion, which is high for a company generating $230 million of revenue and a bottom line loss. At the time of writing Afterpay is the 18th largest listed company in Australia – bigger than Cochlear, Sydney Airport, Aristocrat, Brambles or shopping centre owner Scentre Group. It’s bigger than Bluescope, Qantas and Lendlease combined. I am sure its two founders never envisaged this kind of reception when they were pitching the idea. Indeed, that’s perhaps why they recently sold $270 million worth of shares in their second sell down in 12 months – that’s more than the revenue the company generated. And if they’re selling now it makes you wonder how convinced they are of a takeover by Tencent at current or higher prices.

As I have said before, Afterpay is a factoring company. It buys a retailer’s receivables or debtors for a fee and then collects the amount owing directly from the debtor. Factoring businesses make small margins which partly explains why this company will have to keep raising money and diluting shareholders to fund its expansion. It has been raising money since Sir Ron Brierly’s ASX-listed Mercantile Investment Company bankrolled an $8 million raising for Afterpay in 2015 prior to its 2016 listing and it just raised another $800 million.

Highlighting the irrational exuberance in technology shares is not the only reason for mentioning Afterpay.

The company’s exposure to millennials, many of whom are without jobs, and recipients of government lifelines, raises the question of how long these government programs might continue. And that of course depends on the vagaries of the pandemic.

In the US, where for example California is reversing it reopening agenda after skyrocketing coronavirus cases, companies went into the crisis with record levels of corporate debt. Many are taking on more and the inevitable period of deleveraging that follows will mean lower levels of employment.

So we have an economic crisis and a health crisis. Can it only be the absence of a financial crisis that is justification for such high stock market multiples? Recessions have a negative impact on company revenues and profits and I fear history will show there is nothing unique about this recession’s impact on the stock market. Companies go broke and the equity in those companies becomes worthless.

Government support programs are going some of the way to support consumption but one must question the sustainability of the fiscal support needed just to keep the economy gasping for air, given massive government debt.

Meanwhile central bank conventional and unconventional monetary policy can only keep a company’s interest rates low. Monetary policy at the zero bound cannot bring a failing company new customers. It cannot deliver revenue. Consequently, it is reasonable to expect much higher levels of bankruptcies and defaults than we have already seen. As these businesses begin to fall over, many employees who currently expect to go back to work will not have a job to return to.

Some of those collapsed businesses will be purchased by private equity, but even then they will run a fraction of the stores that existed in 2019 or a fraction of the routes flown in 2019 (see Virgin Australia).

As I have warned at the beginning of this crisis, the market’s definition of a recovery is anything better than the bottom, but the real world’s definition of recovery is a return to previous levels of income. Returning to 2019 levels of revenue and profits for the hospitality, travel, tourism (overseas arrivals to Australia for June were down 98 per cent, year-on-year), and retail sectors, for example, is going to be a very long, drawn-out and bumpy process. Just consider how relatively easy it is to fire 1000 workers – these days it can be done with an email referring staff to the HR support line. Now imagine how much longer it would take to rehire 1000 people. And that’s for a business that survives. Many won’t.

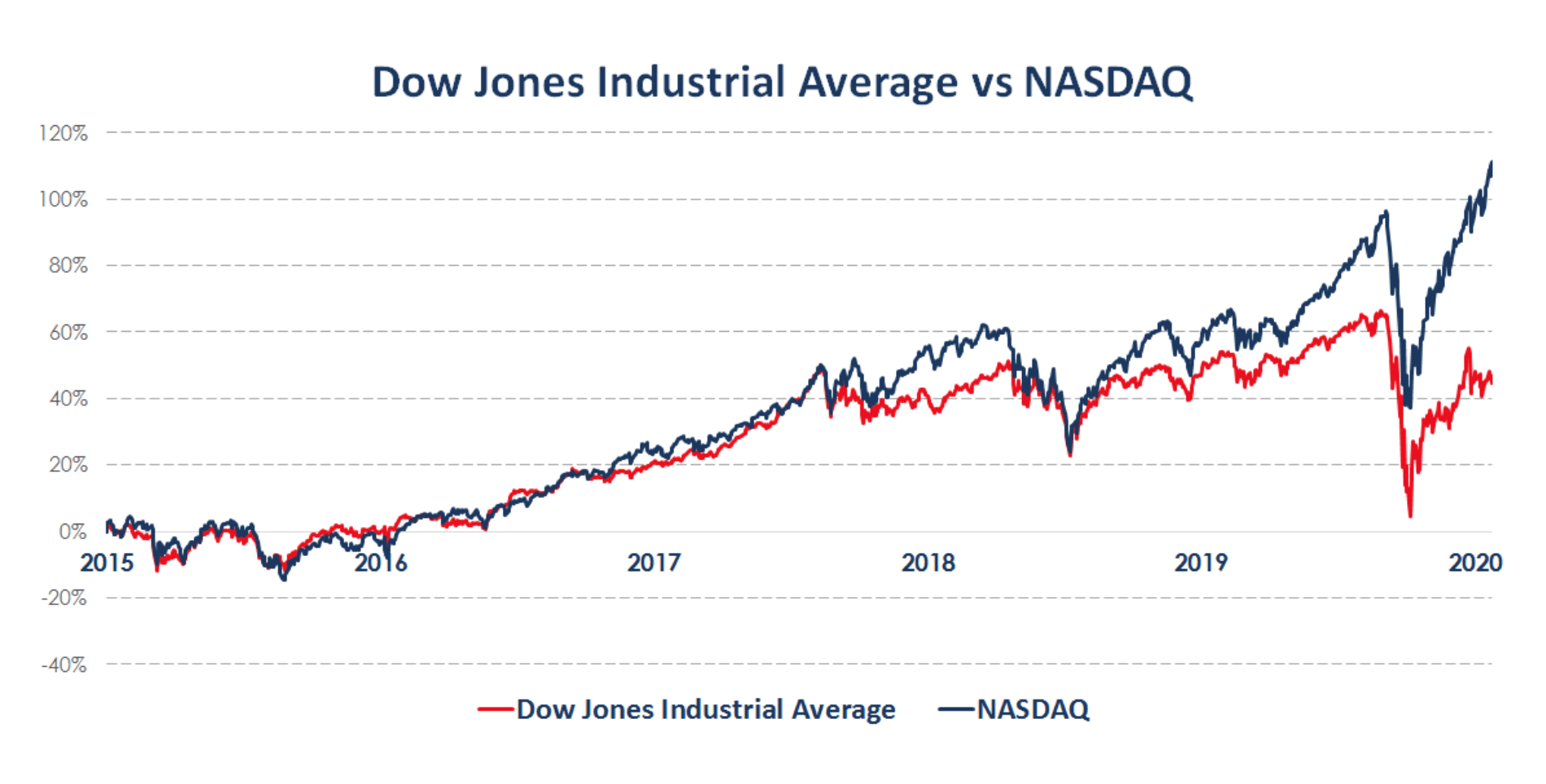

Figure 1. Nasdaq vs Dow Jones

For professional investors it is time to be cautious. No fund manager or analyst can see the shape of employment and therefore consumption because government largesse in the form of wage subsidies has replaced wages of those furloughed. Spending patterns must and will therefore change. Predicting those changes while government handouts remain in place is next to impossible.

For professional investors it is time to be cautious. No fund manager or analyst can see the shape of employment and therefore consumption because government largesse in the form of wage subsidies has replaced wages of those furloughed. Spending patterns must and will therefore change. Predicting those changes while government handouts remain in place is next to impossible.

Raising cash might make sense, and so does missing some of any further upside given the mounting downside risks. Reducing the beta of portfolios also makes sense. The gap between growth and value has never been greater. An almighty mean-reversion is entirely possible. It is also quite likely that the gap between traditional industrial stocks and technology stocks (Figure 1.) will close but perhaps not through the industrials’ rising. Both may fall with industrials falling less.

Investors would be wise at this juncture to consider whether expectations of an imminent end to the pandemic are premature. If first and second Covid-19 waves send cities and countries back into lockdown and keep borders closed, then the unbridled enthusiasm currently gripping markets is equally misplaced and premature. It is therefore worth considering what is not currently expected and at least acknowledge that fat tail risk.

Leave a Comment

You must be logged in to post a comment.