As the professional standards bus trundles towards the legislative milestones government has set, there’s still time either to get on board or choose where to get off.

Management consultant and author Jim Collins is fond of telling organisations they’re like a bus and that to make the transition from merely good to great they first need to get the right people on the bus and get them in the right seats. Only then can they decide how they’re going to get to where they’re going, he says.

There’s a finite number of seats on a bus, so the corollary to getting the right people on board is that you’ve got to make room for them by getting the wrong people off. The bus simile works, for an industry such as financial planning, to a point. It doesn’t have a finite number of seats but the idea holds true that for the industry to go from good to great it needs to get the right people in (and keep them in) and get the wrong people out (and keep them out).

It can be a painful process for those whose ride is coming to an end, but it’s integral to a successful transition from an industry to something closer to a profession. By 2024, when the most controversial of all the new professional, ethical and education standards comes into force – a bachelor’s degree or higher, or equivalent qualification – a significant number of people may have already disembarked.

We’re starting to see some signs of this already.

We’re starting to see some signs of this already.

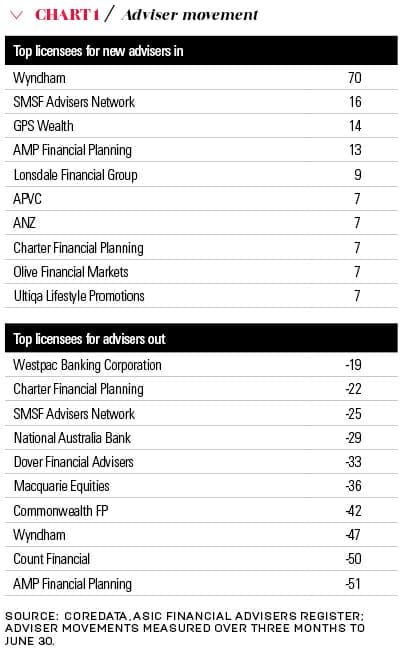

CoreData analysis of the ASIC financial adviser register for the three months to the end of June shows that advisers are leaving the industry, by which we mean their names are being removed from the register, at roughly twice the rate they’re joining, by which we WHO’S mean new names being added to the register. Three months is a short period; figures can be volatile and it’s difficult to draw hard and fast conclusions at this point, but if the trend continues, it means passengers are already getting off the bus.

The decision to leave will be voluntary for some, and, therefore, relatively well planned and well executed. But it won’t be that way for those who are pushed from a moving bus. In June, Dover Financial Advisers cut loose about 400 advisers; and in early July it was reported that another licensee was closely examining about 300 of its authorised representatives with a view to moving them on if they were found to present too great a compliance risk.

Wrong turns

Life will be difficult for some advisers whose licensees close down, or where licensees seek to cull adviser numbers. Other licensees are unlikely to take on representatives who have any whiff of compliance trouble about them. A question that arises, though, is if the situation is so dire that a licence has to be handed back to ASIC and another licensee has to cut several hundred of its representatives, why did they have so many of the wrong people on the bus in the first place?

There are a number of possible reasons, but recruitment practices must surely be questioned. And once they got the wrong people onboard, they clearly didn’t monitor them adequately, and didn’t intervene where necessary to ensure standards were adhered to, if the standards were even adequate to start with.

But no licensee with widespread non-compliance among its advisers can transition from being good, as they might be now, to great, as they will need to be to support the development of financial planning into a profession.

The saying that the standard you walk past is the standard you accept applies here. It shows what can happen when licensees are left as the arbiters of standards and are driven by factors other than the client’s best interests. Under a structure more akin to a profession, it would be incumbent upon each individual practitioner to meet the necessary professional, ethical and education standards. Meeting professional standards means meeting standards of behaviour and competence that exceed the minimum set out in the law.

Compliance would be monitored by an independent body, and the licensee’s task of authorising individuals to give advice would cease. An adviser’s ticket to practice would be issued independently of the licensee. So licensees prepared to turn a blind eye to poor compliance would not have quite the same detrimental effect on the industry as they can have now.

Licensees would still have a massively useful role to play within the emerging profession, but as genuine service providers to advisers. In effect they’d relinquish the part of their role that has created some of the biggest problems in the industry, and be left doing the things that add value.

This sort of approach is some way off yet, and for the foreseeable future we will have licensees and authorised representatives and all of the issues that structure brings with it. And as the professional standards bus continues its journey down the road, someone has to drive.

Change behind the wheel

In mid-June, FASEA announced it had appointed a full-time chief executive to replace its inaugural chief, Deen Sanders. Stephen Glenfield comes to FASEA from the Australian Prudential Regulation Authority (APRA), and brings extensive and relevant regulatory experience. He started in the job on August 1.

During the changeover, the seat was occupied by the eminently capable Mark Brimble, a FASEA board member and leading light in the financial planning education community. But as Glenfield seizes the wheel, FASEA enters a second, and crucial, phase of its work. If the development of professional standards can be thought of as having two stages – a design stage and an implementation stage – then it is now entering the implementation stage. The design stage, led by Sanders, is pretty well complete, but for various reasons that have not been fully explored, Sanders will not see the design to its conclusion.

There’s no reason to suppose the transition from Sanders to Brimble to Glenfield will be anything but smooth, and there’s nothing to suggest the original implementation timetable, as set out by Minister for Revenue and Financial Services Kelly O’Dwyer can’t or won’t be met. This bus won’t be steered down any detours.

So all financial planners have a decision to make, and some already are making it: get on the bus or get off it. There’s no right or wrong decision; each individual financial planner will make the one that’s best for them. There’s no shame in deciding to get off if the journey looks too long or too difficult, but undoubtedly it’s better to do it on one’s own terms. It’s better to get off at a stop of choice than be thrown off as the bus gathers pace.

Simon Hoyle is head of market insight at CoreData Research and a former editor of Professional Planner

Leave a Comment

You must be logged in to post a comment.