The only worthwhile reason to make forecasts of sharemarket indices is to help decision-making. There is little or no value in simply getting the forecast right or wrong. I can make this statement with more veracity than normal because the forecasts I have made and outlined in the below charts have been quite good in recent times.

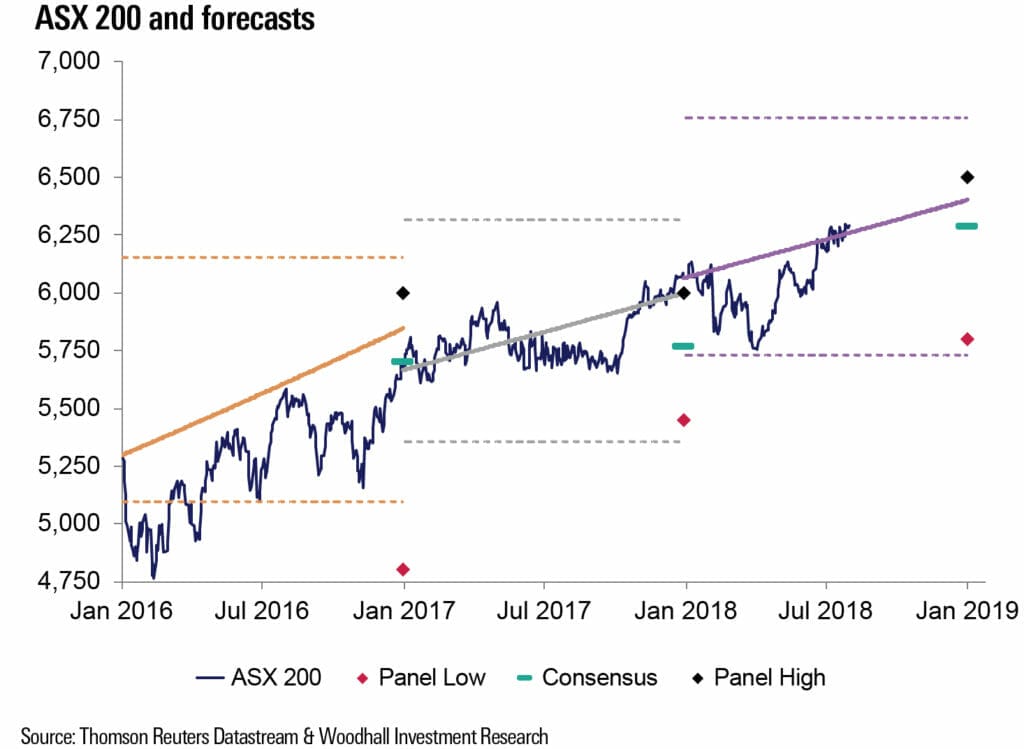

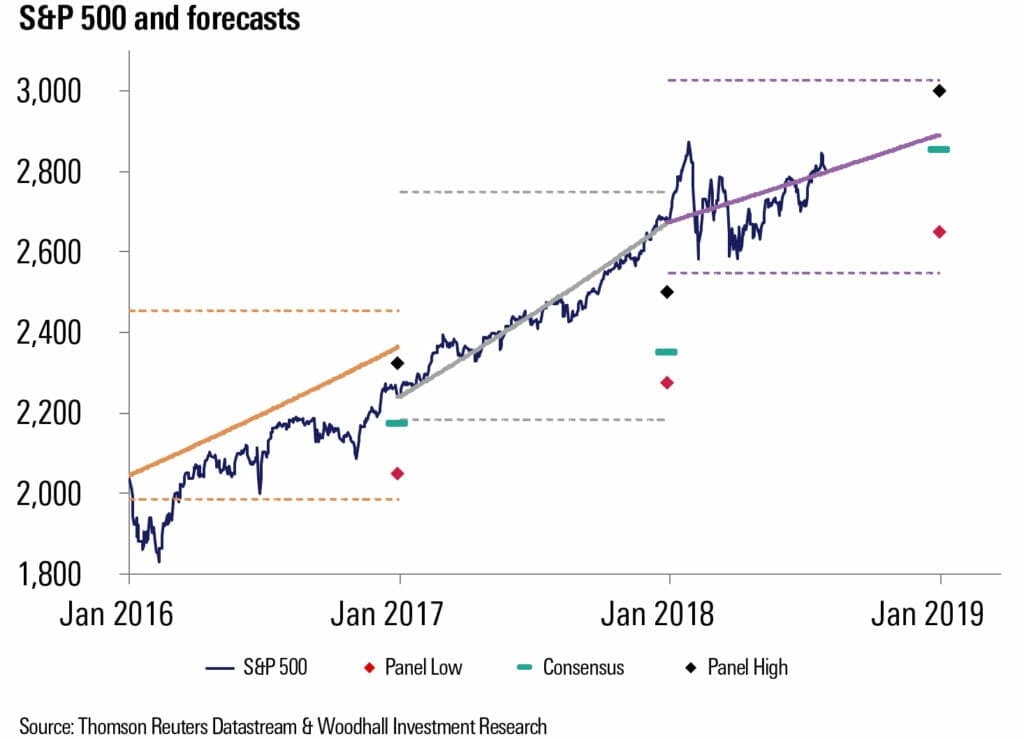

The solid-coloured straight lines in this first chart (below) show the 12-month forecasts of the ASX 200 and S&P 500 for the last two complete calendar years and the current one. These forecasts are based on my interpretation of broker forecasts of earnings and dividends for each of the constituent companies, as surveyed by Thomson Reuters. The panel high, panel low and consensus are taken from reputable publications at the start of each year. The horizontal dotted lines are my January 1 forecasts of the highs and lows for each year and index. Obviously, in a rising market, the low is more likely to occur in the early months and the high in the latter months.

On the last day of each year, the actual performance of the index might be some distance from the forecast, but if a few days earlier or later, then the forecast was close and there was good information stored in the forecast.

When the forecast is outside the range of panellist forecasts – as in 2017 for the ASX 200 and 2016 and 2017 for the S&P 500 – it allows the forecaster to bet against the market. Readers will make what they will of the quality of these forecasts. My assessments are as follows:

For the ASX 200

2016: The early dip was a buying opportunity; that would probably not have been the conclusion for the panel low (marked by the red diamond) and some others below the green consensus marker. I was fully invested for the full year.

2017: There was no sell signal for me but there possibly was one for the consensus forecasters.

2018: As I wrote in this magazine at the time, the early peak was over-bought – but not enough for me to sell. The April dip was a buying opportunity (which I took). My end-of-2018 forecast is close to consensus and the forecast is on track at just past the halfway point. It’s ears-pinned-back time for me unless new signals emerge.

For the S&P 500

2016: The early dip was a buying opportunity (which I took); that would probably not have been the conclusion for the panel low (marked by the red diamond) and some others below the green consensus marker.

2016: The early dip was a buying opportunity (which I took); that would probably not have been the conclusion for the panel low (marked by the red diamond) and some others below the green consensus marker.

2017: A simple matter of holding a fully invested position.

2018: No sell signal early on but the low wasn’t quite low enough for a new buy!

At the halfway point for 2018, my strategy seems well set. I am about 57 per cent in the ASX 200 and 43 per cent in the S&P 500 (of which 50 per cent is completely hedged against currency fluctuations).

Everyone (including me) knows that the bull run will end one day. For me, there are no signals (yet!) to walk away from a successful strategy. Whether signals will emerge in a timely fashion can be answered only in hindsight. But there are three things I am looking for:

- The simple one is if we get a bigger bubble in the markets than we did in late January/February 2018 or, even better, if the index takes out the high dotted lines. I will use my measures of exuberance to help detect such a situation and sell. Although these calendar-year forecasts do not get revised, I update them daily to look for signals that underlying expectations are changing.

- As my forecasts are based on broker forecasts of earnings and dividends, I am particularly watchful during our August and February reporting seasons for the ASX 200. There are quarterly updates in the US.

- The third (and most difficult) indicator is some global political/economic factor that causes enough concern to bail out. In time, brokers will catch onto such events and revise earnings.

Sometimes, events move too quickly to wait for these broker updates. But as they apparently used to say when soldiers faced off against each other with muskets, ‘Wait until you can see the whites of their eyes before you fire!’ If one sells too soon, when will be the opportunity to get back in for the rest of the rally? Rather than take profits too early, I’d rather wait for the start of a downturn – accepting that loss but collecting the prior gains along the way.

Dr Ron Bewley is a principal of Woodhall Investment Research and a regular columnist for Professional Planner.

Leave a Comment

You must be logged in to post a comment.