The argument that active investment produces results inferior to index investment appears to be the consensus in the press in Australia.

This also appears to be the belief of Australia’s regulators, who have enshrined reducing what providers can charge in investment fees – hence increasing index investment – as one of their primary objectives.

Given this near universal acceptance of the superiority of indexing, and the ‘proof’ that the average manager underperforms the index that is presented on a daily basis, it should be expected that the index products available to superannuation fund members would show clear outperformance of their active equivalents.

In fact, the reverse is the case.

Consider the results of Australia’s largest superannuation fund, AustralianSuper.

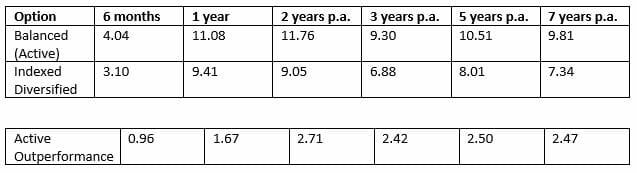

The fund offers both the actively managed Balanced option, and the passively managed Indexed Diversified options to members.

The characteristics of the two products are virtually identical when expressed in terms of the descriptors prescribed in legislation and regulation. Both have 10-year recommended investment horizons; both have the same risk of negative return (five years in 20); and both have roughly the same long-term return objective (Consumer Price Index + 4 per cent a year and CPI + 3.5 per cent for the Balanced and Indexed Diversified funds, respectively).

As expected, the indirect cost ratio of the Balanced option is higher (0.57 per cent) than that of the Indexed Diversified option (0.10 per cent).

Given that both options are offered by the same super fund, all other costs should be similar, if not identical. Therefore, the difference in overall management expense ratios (MERs) would reflect only the differences in investment management fees between active and indexed management.

Equally, the difference in returns to investors will reflect only the difference in net investment returns between active and indexed management.

Given the argument that active management reduces returns below “market returns”, then AustralianSuper’s Indexed Diversified option should outperform the Balanced option by a substantial margin – at least by the 47 basis points a year difference in investment costs.

In reality, the actively managed Balanced option has consistently and substantially outperformed its indexed equivalent.

Returns, net of fees (%)

Put simply, in the year to June 2018, the additional cost of 47 basis points in management fees produced a gross increase in members’ returns of 2.53 percentage points, leaving a return, net of fees, 1.67 percentage points higher.

Put another way, reducing the investment costs and fees in the Balanced option by $1, by switching to an indexed investment approach, would have reduced net investment returns to members by $3.55 over the last year.Put simply, in the year to June 2018, the additional cost of 47 basis points in management fees produced a gross increase in members’ returns of 2.53 percentage points, leaving a return, net of fees, 1.67 percentage points higher.

Comparing the pair

If the relative outperformance of AustralianSuper’s actively managed Balanced option over five years were to continue (the Indexed Diversified option has been available only since 2011), it would earn an additional $31,900 over 10 years.

By comparison, the outperformance by industry funds over retail funds in the ‘Compare the Pair’ ads as a result of industry funds having lower fees is only $15,000.

How can this be? How can AustralianSuper’s actively managed option outperform its indexed equivalent, given everything that we read about the supposed superiority of index funds?

The outperformance of the actively managed Balanced option is not surprising. It simply reflects the reality that institutional investors are able to select managers who add value after fees, and do not invest with the average manager.

John Peterson is the founder of Peterson Research Institute and has over 35 years of experience in the financial services and investment industry.

Leave a Comment

You must be logged in to post a comment.