In his book The Outsiders, William Thorndike analyses eight chief executives who produced extraordinary returns for investors. The secret to their success was, essentially, how well they reinvested company profits.

Rather than trying to boost short-term earnings or risking the company with a ‘transformational’ acquisition to maximise their short-term bonuses, this unique group made sensible long-term decisions that created enormous value.

Here, then, is a look at one of the chief executives from Thorndike’s book, and two other CEOs whose top-notch results demonstrate that they’re also worthy of close attention from investors.

John Malone

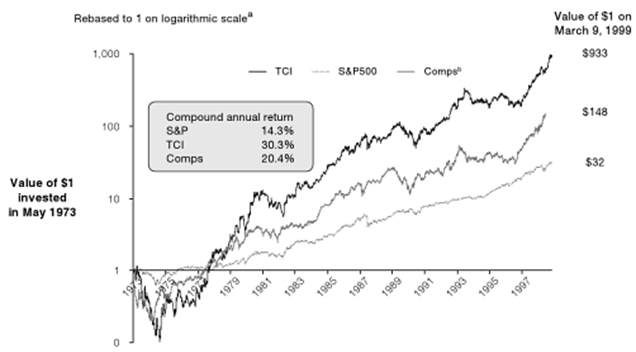

One of the chief executives in the book was John Malone. He is the doyen of the US cable TV industry and the lead protagonist in the book Cable Cowboy. He produced 30 per cent annualised returns as chief executive of TCI between 1973 and 1999 (twice that of the S&P 500 – see Chart 1) before selling the company to AT&T at the height of the tech boom.

Unlike most chief executives profiled in the book, who no longer run listed businesses, you can still invest alongside Malone. From the ashes of the tech wreck, he emerged with a large stake in Liberty Media, which spawned numerous companies with interests in cable TV content and distribution, satellite radio and broadband internet, just to name a few.

We own several Liberty names with businesses diversified by industry and geography. They don’t typically screen well due to a host of factors. For example, management focuses on maximising free cash flow to buy back shares, rather than reporting high current profits that attract high taxes, which depresses return on equity even though the company produces high returns on investment.

As complications like this keep most investors away, despite management’s remarkable track record, we’ve no problem taking advantage of the discounts others overlook.

Paul Saville

Paul Saville isn’t one of the eight chief executives in the book, but should there be a second edition one day, Saville is a prime candidate to be included. He watched the original incarnation of homebuilder NVR go broke before becoming chief executive in 2005. Unlike virtually every other listed homebuilder on the planet, he learned from the experience and constructed a way to protect NVR from recessions.

Instead of dangerously leveraging the balance sheet to accumulate land for development, NVR lays down 10 per cent of the purchase price for an option on future development. This means the balance sheet isn’t highly geared, allowing the company to buy back three-quarters of its shares on issue over the past 20 years. That’s a remarkable feat for any company, let alone a homebuilder.

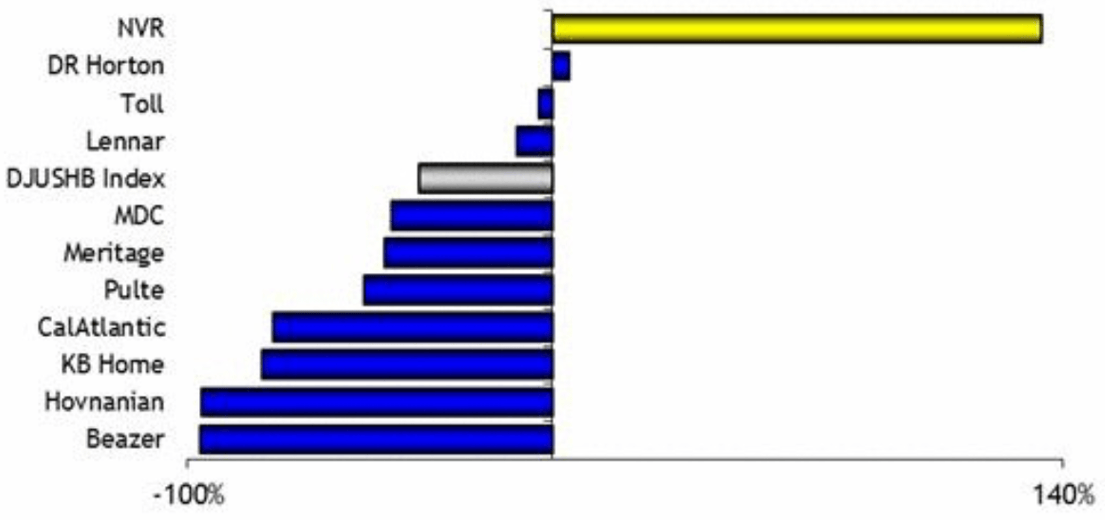

In 2009, NVR was the only listed US homebuilder to make a profit and post respectable shareholder returns through the GFC (see Chart 2). With US housing stock now reaching record lows, interest rates still low and the millennial population – the country’s largest ever – reaching a median age that suggests they’ll soon start having families of their own, the company is well placed to benefit from an increase in homebuilding. If housing doesn’t pick up, we expect the company to buy back plenty more shares.

Richard Liu

Richard Liu is the founder of Chinese online retailer JD.com. He’s fanatical about delivery times, the condition of the goods once delivered and eradicating fakes, which are a huge problem in China. In every way, he embodies the spirit of the chief executives in Thorndike’s book.

While JD.com’s larger rival Alibaba measures delivery times in days, JD.com measures them in hours, usually promising same-day delivery if you order before 11am. This incredible feat reflects huge long-term investments in warehouses and delivery fleets, which Alibaba has avoided to keep current profits as high as possible. It also required a culture change, in an industry not usually associated with caring much for the state of parcels to be delivered.

Over time, we expect JD.com’s delivery advantage to allow the company to expand its range of goods and take market share from Alibaba. But it requires Liu’s fortitude to sacrifice profits today for much higher profits tomorrow.

No guarantees

Usually, these types of remarkable chief executives have large stakes in the businesses that they run, but buying just any business with high insider ownership doesn’t guarantee high returns. The marriage of an honest and intelligent chief executive with decent assets is a great start, but you also need to pay the right price for the stock and potentially hang on for decades.

In an environment where revenue growth is hard to come by, we believe entrepreneurial managers are worth their weight in gold, as they adapt to keep their businesses growing. Our job is to keep finding more of these talented individuals to partner with so that your savings continue to grow alongside theirs.

Disclosure: Peters MacGregor Capital Management Limited holds a financial interest in JD.com, Liberty Broadband and NVR through various mandates where it acts as investment manager.

Leave a Comment

You must be logged in to post a comment.