Debt is a powerful weapon. It can build wealth or destroy it.

Almost a decade has passed since a swath of subprime mortgage defaults across the US kicked off the global financial crisis, highlighting the dangers of excessive debt. The world is now a different place, but in ways few could have imagined.

Meanwhile, Australia’s household debt has climbed to a record 185 per cent of annual household disposable income (driven partly by property booms in Sydney and Melbourne) compared with about 70 per cent in the early 1990s.

Is this a debt bomb set to explode?

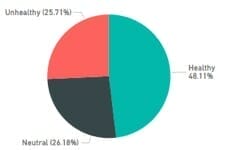

A new analysis of Moneysoft’s real-world client data shows there is cause for concern; slightly more than one-quarter of mortgages were classed as “unhealthy” because they had increased in size by at least 5 per cent over the history of the loan.

Just over one-quarter were “neutral” (loan balances were steady) leaving slightly less than half of all loans classed as “healthy” (the loan size had decreased by at least 5 per cent).

Chart 1: Mortgages under stress

Source: Moneysoft analysis of 1933 client mortgages (not including investment, business, commercial and personal loans) at December 2016. Mortgages analysed have at least six months of balance and transaction history and are more than $100,000 in value.

Just as alarmingly, this potential mortgage stress is concentrated among Australians with larger loans, who are potentially more vulnerable to interest rate rises.

Chart 2: Larger loans under pressure

Source: Moneysoft analysis of 1933 client mortgages (not including investment, business, commercial and personal loans) at December 2016. Mortgages analysed have at least six months of balance and transaction history and are more than $100,000 in value.

The top 10 per cent of the most leveraged Australian households now have an average debt-to-disposable income ratio of 600 per cent, the AMP.NATSEM Income and Wealth Report states. Also, middle-aged Australians have taken on significantly more debt as the cost of borrowing has fallen; the average debt-to-income ratio of 30- to 50 year-olds has climbed from 149 per cent to 209 per cent during the last 10 years.

Australians have become accustomed to low interest rates in recent years but two clear lessons to take from the GFC are that no one knows every risk lurking around the corner and markets can change quickly.

The election of Donald Trump as US president is proving to be a turning point. His plans to undertake vast spending programs and cut taxes are expected to boost inflation (and potentially growth), prompting heavy bond market losses in October and November.

This new equilibrium will ultimately affect Australia. Expectations of an official interest rate rise late in 2017 are now crystallising.

Reserve Bank of Australia data suggests that extra savings borrowers hold in home loan offset and redraw accounts would provide an average two-and-a-half-year repayment buffer at current interest rates, there is clearly a subset of borrowers who have used low interest rates to leverage up.

Many of these borrowers should act now to strengthen their household balance sheets.

The financial planning industry is heavily focused on the benefits of investing but effective advice is about more than generating returns. It also involves managing all forms of risk.

The cash flow generated by debt reduction can quickly outpace that from most investment returns when you consider the amount of risk (or level of savings) an investor would need to take on to produce a similar net result.

Debt has a role to play in wealth creation but it is a weapon that needs to be handled carefully, with budgeting – or we will all be left to pick up the pieces when the bomb explodes.

Leave a Comment

You must be logged in to post a comment.