The Government’s decision to scrap the proposed retrospective lifetime non-concessional contributions cap of $500,000 and maintain the current cap of $180,000 until 30 June 2017 provides a final opportunity to ramp up superannuation balances before a new, more restrictive, superannuation regime comes into force.

Michael Hutton, head of wealth management at HLB Mann Judd Sydney, says it’s more important than ever for people to start thinking about their superannuation early.

“Government changes in recent years have made the old approach, of topping up super in the last 10 years before retirement, virtually impossible.

“While we used to talk to clients about focusing on superannuation when they were in their fifties, we are now having these conversations when clients are in their thirties.

“It is increasingly difficult to put large sums of money into superannuation so people really need to a find way to put smaller sums in, more frequently, early in their working life,” he said.

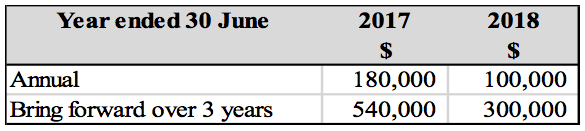

From 1 July 2017, the Government will introduce an annual non-concessional contributions cap of $100,000, or $300,000 brought forward over three years* (as shown in the following table). This will only be available to those with a superannuation balance of less than $1,600,000.

There is no such limit imposed on non-concessional contributions under the current system.

“This current opportunity to maximise non-concessional contributions under the current system represents a superannuation contribution opportunity of a magnitude not seen since the 2007 financial year, when the Government allowed everyone a “one-off” non-concessional contribution limit of $1 million,” says Mr Hutton.

“For those with more than $1.6 million in superannuation, this may be their last opportunity to make non-concessional contributions to their superannuation fund.

“On the other hand, those with little or no superannuation have the opportunity to make a substantial start on their retirement savings.”

Mr Hutton says that, as was the case in 2007, it is expected that more self-managed superannuation funds will be established as people look to make large contributions.

For example, a husband and wife could potentially have an extra $1,150,000 in super before 30 June 2017, by each making non-concessional contributions of $540,000 and concessional contributions of $35,000.

“Those without the cash to make the contributions may consider borrowing to do so. This is not normally recommended partly because the interest on the borrowings is usually not tax deductible, but in certain circumstances it may be worthwhile in order to take advantage of the current window of opportunity.”

Mr Hutton says that superannuation is still the best investment structure through which to save for retirement, despite the ongoing tinkering by successive governments.

“There is no other investment opportunity that allows 15 percent tax while accumulating; is tax free when paying a pension; has a strong investment structure and regulations; and provides asset protection,” he said.

The Government has confirmed that it will push ahead with the following restrictive superannuation measures proposed in the May 2016 Budget:

• reduction of the concessional contribution cap to $25,000

• limit of $1.6 million that can be transferred into pension phase

• removal of the tax exemption on superannuation funds paying transition-to-retirement pensions

• the reduction of the assessable income threshold resulting in concessional contributions being taxed at 30% rather than the usual rate of 15%, from $300,000 to $250,000

The Budget proposal to carry forward unused concessional contribution caps over five years for those with less than $500,000 in superannuation has been deferred, with the proposed commencement date moved to 1 July 2018.

Furthermore the Government has announced that it will not proceed with the Budget proposal to remove the work test for persons wanting to make contributions between the ages of 65 and 74.

“All these new caps and thresholds will add complexity to the superannuation system not seen since the days of Reasonable Benefits Limits and the superannuation surcharge.

“This unfortunately creates a lack of confidence in the system and discourages people from saving for their own retirement.

“However with good advice and careful navigation, our superannuation system will still provide exceptional wealth management benefits,” Mr Hutton said.

Leave a Comment

You must be logged in to post a comment.