Aged care is increasingly becoming a concern for older Australians and their families. Already more than one million Australians access aged care services across home services and residential care. With an ageing population these numbers are set to increase.

Higher rates of dementia and a greater range of care choices, as well as higher and more complex fee structures, are increasing the need for clients to seek advice. Financial advisers can no longer ignore aged care for clients.

Every adviser needs to develop a business solution that incorporates aged care advice. This does not mean every adviser needs to become an expert. But a more proactive role should be taken to help clients face issues so they can be better prepared and age with greater dignity.

Helping clients plan ahead

When an aged care need arises, clients and families are often in crisis. They may be faced with making quick decisions in a period of high stress, particularly if forward planning has been inadequate. This adds to family tensions and may result in ill-informed decisions.

Financial advisers have a responsibility to raise awareness by proactively raising issues before a crisis occurs. For clients and their families, peace of mind and a clear roadmap can make all the difference.

Financial decisions made throughout retirement (such as gifting, the creation of life interests or separation of assets in blended family situations) without consideration for aged care implications, may also result in adverse outcomes for clients.

|

Example: the need to plan ahead Arnold and Maggie (names changed) have been married for 20 years. It is a second marriage and their home (a retirement village unit) is owned in Arnold’s name. They have another $60,000 in bank accounts between them. Arnold lost mental capacity and moved into aged care more than 12 months ago. The home was an exempt asset and Arnold was assessed as a low-means resident. He paid the basic daily care fee and the government paid for his accommodation and the rest of his care. Maggie’s health has since deteriorated and it is now time for her to move into aged care. The home has been sold and used to pay for Maggie’s refundable accommodation deposit (RAD). But Arnold’s fee assessment now includes half the value of her RAD and he will be asked to pay higher fees to cover his accommodation and care. Arnold applied for financial hardship, but this has been denied. Planning and advice may have helped them to understand the range of options and impacts before the home was sold to gain more effective outcomes and reduce the financial stress on the family. |

The business opportunity

Care needs are generally greatest for clients aged over 70 but it is not just older clients who need advice. Decisions are often made by children or grandchildren, who are aged 45-70. Aged care conversations should be had with all clients of all ages:

- Older retirees – advice on care options and how to best structure finances to maximise value from the amount they can pay towards care costs

- Pre-retirees – help with setting retirement goals to incorporate the costs and implications of accessing aged care

- Younger clients – support to make decisions for parents or other older relatives and awareness of options available.

Not only does aged care advice create opportunities to add greater value to clients or to generate business growth, but it is also an important client retention strategy.

| Example: client retention

Ed is age 50 with $1.5m in funds under advice, mostly invested in an SMSF. His adviser offers a high touch service and annual revenue is approximately $24,000. Ed is a happy client and his SMSF is performing well. However, Ed has older parents and is increasingly spending time helping them on a daily basis. Eventually a decision is made to access aged care for his father. Ed is confused and is referred by a friend to an adviser who helped her with a similar scenario. Ed’s adviser has never had a conversation with him about aged care so he does not think to seek advice there. Ed is very relieved and grateful for the advice from the new adviser and starts to wonder what else his current adviser is missing. The first indication his adviser has of any issues is when he receives a letter from Ed asking to transfer all his business to the new adviser. Ed’s sister also engaged the new planner to review her retirement plans. Not addressing aged care cost this adviser at least $24,000 per year in revenue. It has also cost the potential to establish relationships with other family members. |

Ignoring aged care and not having conversations with younger clients can have a significant cost to advice businesses. How many clients are you willing to lose? And what would that cost your business? It is not just the lost revenue but also the cost of bringing on new replacement business.

A survey undertaken at the recent Financial Planning Association (FPA) national roadshow showed that of the more than 3000 attendees, 70 per cent of respondents have parents or grandparents over the age of 70. This is likely to resemble the client demographics within a typical financial planning business – highlighting the risk to advice businesses of ignoring aged care.

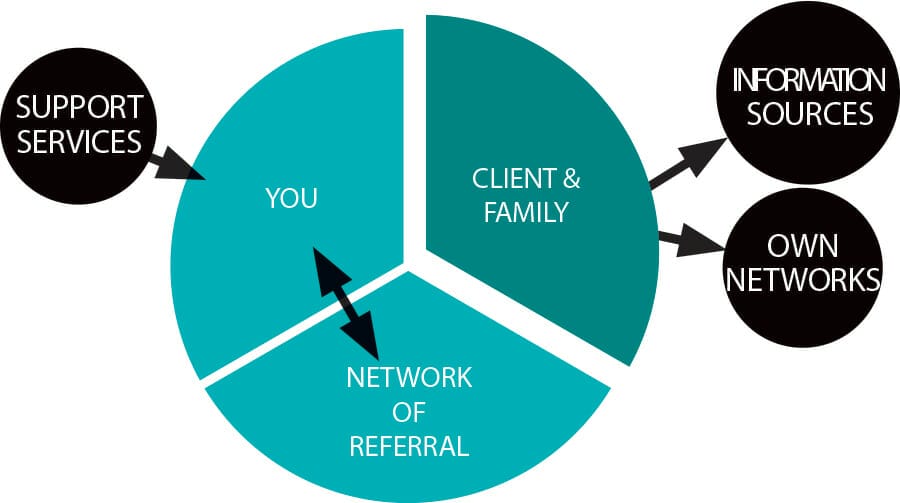

Incorporating advice into business

When deciding how to incorporate aged care advice into your business, think of it like project management, as demonstrated in the Aged Care Blueprint below.

The first step is to identify the actions and decisions that families may need to undertake. Then decide which parts will be included in your advice service offer, which parts will be referred to your network of partners and which parts will be handled by the family.

Following this Blueprint will allow the investment you make in your business to match the value it adds. It also provides a clear outline for how to support clients and add greater value to clients, their families and your business.

Leave a Comment

You must be logged in to post a comment.