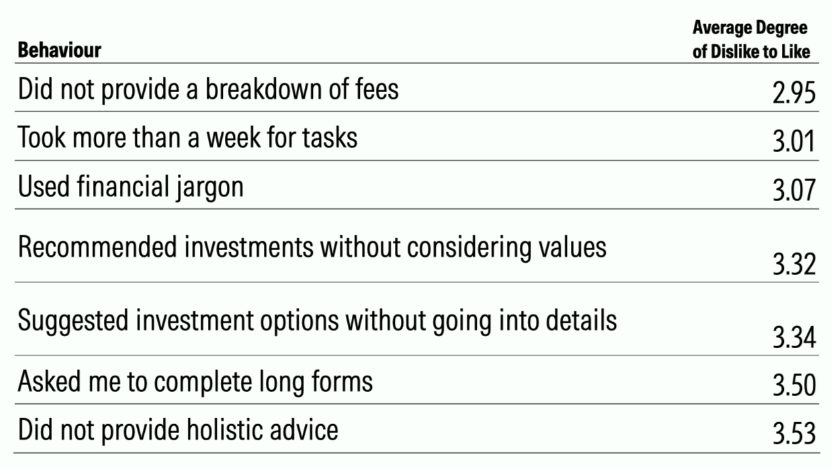

Not providing a breakdown of fees, taking more than a week to complete tasks and using excessive financial jargon are the top three “faux pas” made by financial advisers, research from Morningstar has uncovered.

In a presentation at the researcher’s investment conference in Sydney, Morningstar global head of behavioural insights Ryan Murphy said the value of understanding these friction points is important as it could otherwise result in a disengaged client – if the adviser relationship isn’t ceased.

Based on a survey of 400 households with an active adviser relationship, respondents rated on a scale of one to seven how much a particular adviser behaviour “irritated” them.

Murphy said this type of survey tends to skew towards positive responses, meaning a 3.5 average isn’t necessarily the neutral point.

“To see an average of 2.9 come out gets your attention,” Murphy told the conference. “This isn’t just a little bit of irritation on average, there’s quite a bit.”

Most ‘irritating’ adviser behaviours

Source: Morningstar.

Overall, Murphy said around three in four of those households believed advisers were exhibiting at least one of these “irritating” behaviours.

“When we went into this research, we thought there might be about one out of five, one out of four households that are expressing some degree of sufficient annoyance with their adviser, but this came as a surprise to us.

“It’s not 20 per cent, it’s close to about 70 per cent to 75 per cent of these households are saying their adviser is doing at least one of these things.”

Aligning expectations

Murphy said it should be a “wakeup call” for advisers who entertain any of these habits and there are solutions to rectify this.

“This is your practice, your lifeblood and you should have some better insights as to what is potentially irritating customers,” he said.

One of the longest tasks to complete is the production of the advice and Murphy said it was important to properly articulate the timeframe a Statement of Advice needed to be delivered.

“I don’t think it’s because you’re working too slowly – it’s a misunderstanding, a misalignment of expectations,” Murphy said.

“Clients don’t know how long these things should take. Can you put together an SOA for me in the next 15 minutes? Is that possible? Clients often don’t have an appreciation for how complex and long these things actually take, so that’s worth setting those expectations up front.”

Along with breaking down how fees are calculated, Murphy said there is value in having a conversation about the importance of the best interest duty.

“I know you all work under this standard and it’s required here in Australia which is outstanding, but just because we have that in the industry here, doesn’t mean your clients know precisely what that means,” Murphy said.

“It might be worth having a conversation to talk about what that is. This is a big driver of trust and having clients understand this and it’s also worth having a frank conversation about how you are compensated and to make sure that your recommendations are not compromised by ulterior motives and making that explicit.”

Avoiding overusing financial jargon is important, although Murphy conceded advisers are left with “the curse of knowledge”. However, it’s still incumbent on adjusting communication to fit client needs.

“It’s so hard as a deep expert for you to image not knowing all of things that you know, and it’s easy to forget the client is coming from such a different perspective,” Murphy said.

“Jargon is useful when talking amongst experts. It allows for very dense, compact communication, but talking to people outside of our domain of expertise can lead to a lot of confusion.”

Murphy said this is where AI can be useful, because it can be instructed to convert client communication as if it was being delivered to a 10-year-old, for example.

“I’m not suggesting you should talk to your clients like they’re 10,” he said.

“Rather, this is a stringent filter that can help reduce the complexity of sentence structure and avoid unnecessary verbiage and can even catch acronyms and other sort of things.”

Disengaged clients

The researcher found only 6 per cent of clients fire their financial adviser, but Murphy cautioned it’s worse to have a disengaged client rather than be fired by them.

“That doesn’t mean there’s 94 per cent of clients who are really engaged; there can be a gap in there and that’s what we’re trying to explore and better understand,” Murphy said.

“Just because a client is staying with you, isn’t the same thing as being engaged with you in the advice process. Clients often disengage from adviser’s practice instead of just ending the interaction entirely and this can have lots of bad consequences.”

Murphy argued disengaged clients also take up crucial resources from the practice. “These are some of those valuable things you have, and it would be a shame to waste them on clients that don’t really appreciate it,” he said.

“Disengaged clients don’t grow with you, the advice process stagnates and doesn’t become deeper over time.

“These clients who are disengaged are not out there advocating for you and your practice and we know from previous research this is a major source of value for practices as they grow and develop.”

Leave a Comment

You must be logged in to post a comment.