In the financial year ended June 30, the listed accounting and wealth group Count generated revenue of $91.5 million and reported earnings before interest, tax, and amortisation (EBITA) “before profit from associates” of $8.9 million.

Profit from Count’s associates for the year totalled $3.3 million. This contributed to a consolidated EBITA figure of $12.2 million and ultimately to a profit before tax of $8.9 million, and profit after tax of $7.5 million.

In other words, the profit contributed by its associate firms was equal to half of the company’s total reported profit after tax. This provides a neat example of why licensees such as (but not only) Count are increasingly keen to invest in the businesses they also provide services to.

At balance date, Count held interests in eight associate firms, in stakes ranging from 32.36 per cent to 49 per cent, and it shared in the profits of those firms accordingly:

| Entity | Count’s holding (%) |

Equity-accounted profit contribution ($) |

| One Hood Sweeney | 32.36 | 1,027,000 |

| Hunter Financial Services | 40 | 322,000 |

| OBM Financial Services | 40 | 231,000 |

| Rundles CountPlus | 40 | 252,000 |

| Rundles Financial Planning | 20 | 56,000 |

| DMG Financial Holdings | 30 | 359,000 |

| Southern Cross Business Holdings | 49 | 549,000 |

| WSC Group – Aust | 32.75 | 508,000 |

| Total: $3,304,000 | ||

| Source: Count Ltd Annual Report 2023 | ||

While investing in the business of advice (or accounting) is an option for those that have the capital to do it, it’s also increasingly common for licensees seek to share in the revenue of the first within their networks by moving to variable licensee fees.

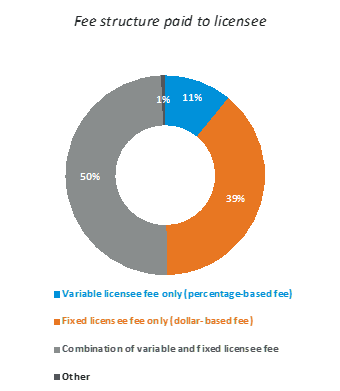

CoreData Research shows that fixed-dollar fees are firmly in the minority. Its latest data shows only four in 10 (39 per cent) of advisers pay a fixed-fee only. While only a small proportion (11 per cent) of advisers pay a pure variable fee, half (50 per cent) pay a fee made up of both fixed and variable components.

WT Financial Group’s 2023 investor presentation illustrates how this emerging approach to fee structures work in practice. The business derives revenue from five principal sources:

Base fees: all advice practices pay minimum base fees.

Practice revenue: the licensee retains a percentage of advice practice revenue.

User-pays services: advice praxtices pay for servives such as professional indemnity insurance, and advicetech

Licensee and adviser services: services for own-AFSL firms

B2C revenue: including advice, accounting and mortgage broking

WT told investors there was potential growth in base-fee revenue from repricing some legacy arrangements, and that “correct[ing] some legacy deals” and firm restructuring would underpin its practice revenue stream.

To justify higher (and increasing) licensee fees, and to demonstrate a commitment to helping their advisers’ businesses grow, licensees are developing new services to support the businesses of the adviser they authorise.

For example, Centrepoint Alliance’s 2023 annual report and presentation to investors showed that it was actively developing lending and managed account services, with 30 firms already participating and a further 27 in the pipeline, and an average of 45 leads a month.

Centrepoint said it had also secured a $10 million debt facility to support planned M&A activity. But its growth strategy also has a clear organic growth element.

The licensee said it had a strong adviser recruitment“pipeline, revealing it had held or was in conversations with 271 authorised representatives and 93 self-licensed advice firms. But the conversion rate from conversation to onboarding appears quite low: it was onboarding or had made offers to 15 authorised representatives (equivalent to 5.5 per cent of the pipeline) and six self-licensed firms (6.5 per cent).

Centrepoint booked a profit after tax of $6.3 million on gross reported revenue of $271.6 million, which included $239 million of advice fees and commissions generated by advisers, which flowed through the AFSL and which Centrepoint paid out to its advisers.

Leave a Comment

You must be logged in to post a comment.