The shadow financial services minister Stuart Robert reckons it would have been better for financial adviser education and professional standards to have been set by the industry itself rather than legislated by government.

Well yes, it’s easy to say that now, and Robert admits to the benefit of having 20:20 hindsight. But let’s not forget that a big part of why legislation was needed was because the industry had been given opportunity after opportunity to do exactly what Robert says he would have preferred, but infighting, vested interests, splinter groups and inconsistent (and sometimes incoherent) representations to Canberra ultimately left the government of the day with no choice but to step in.

Something had to be done and since the industry itself, represented by myriad associations, could not agree on what that should be it got what it got warts and all.

Once financial advice set out on a path towards professionalism there were certain things that were always and obviously going to happen, even if those things were unpalatable or intolerable to some advisers. There would be fallout and there would be individuals who couldn’t or wouldn’t complete the transition.

Professional Planner called that out at the start – it said consistently there was much more to being a professional than just claiming the title, wearing a smart suit and having a nice office. If the industry wanted genuinely to transition to a profession it would have to be prepared for both the extent of that transformation and the work it would require. It was going to be uncomfortable and messy. It would involve changes to individual behaviour and accountability, to business structures and to the nature of relationships within the system: between client and adviser, between adviser and licensee and – maybe most obviously – between product manufacturers, advisers and licensees.

But the point is, the debate about professionalism had gone around in circles for years, and it needed a circuit-breaker. That’s what legislation was – first the Future of Financial Advice (FoFA) changes, then the education and professional (including ethical) standards. It took away from the industry the option of continuing to obfuscate and delay and protect the status quo, which had been shown comprehensively to have failed consumers often enough to warrant being overhauled.

Yes, the legislation was imperfect; and yes, it needs to be reviewed now. But there is something there to be reviewed. We can see what has worked and what hasn’t and, therefore, what needs to be changed and how. If changes hadn’t been legislated in the first place, then it’s anyone’s guess how far along the professionalism path the industry would be today.

There’s broad agreement that the intent of the education and professional standards (including the Code of Ethics) was good and necessary, even if it was poorly implemented. And there’s emerging evidence that it’s dawning on the public that financial advisers are being held to higher standards than they used to be.

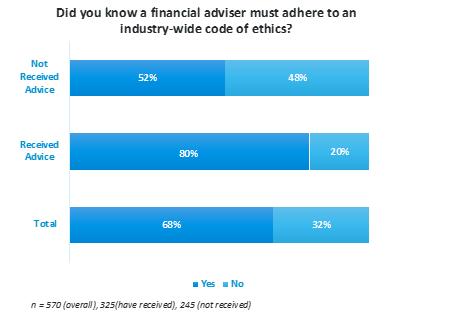

CoreData’s ‘Trust in Financial Services’ research in the second quarter of this year found that more than half (52 per cent) of people who’ve never even received financial advice now know that advisers must adhere to a Code of Ethics (it’s 80 per cent among individuals who have received advice); and for more than one in five of those people, the mere fact of adherence to the code increases their trust in financial advisers.

Let’s be realistic about the progress that’s been made and the changes that are needed from here.

We have a financial advice profession that is more difficult to get into today than it used to be and more difficult to stay in than it used to be – both positive developments and both in-line with the structures of a profession.

We have a Code of Ethics that for the most part works well, even if there is still some wailing and gnashing of teeth about conflicts of interest – again, a positive development and consistent with a profession.

We have emerging public awareness of the Code of Ethics, and higher trust in financial advisers as a result. We have other things as well, including a much healthier (from the client’s perspective) relationship between advisers and product manufacturers.

If this is an approach that has failed, give me failure any day. Yes, it can be improved, but name a piece of legislation – any legislation – that cannot be improved.

Professional Planner quoted Robert saying he’d rather the industry “self-regulate itself with the bodies coming together – the AFA and FPA coming together”, and that having “its own accreditation body of education or skills or experience would be a far better way of doing it”.

There’s nothing stopping the industry doing exactly what Robert says and creating a set of accreditation or education standards for practitioners above and beyond those required by law, if that’s what it wants to do. That’s ultimately what professions do anyway – they self-regulate (including taking disciplinary action against their own), they act in the public interest, they hold members to a standard of behaviour and competence that exceeds the bare minimum set by law and, in return, the members of a profession enjoy a privileged position in society.

All of that is terrifically good, and it’s what the industry said for years that it wanted. It’s fortunate that we didn’t have to hold our collective breath waiting for the start of the process to happen organically.

Simon Hoyle is head of market insight at CoreData.

Leave a Comment

You must be logged in to post a comment.