As the clock counts down to the deadline for the government’s Quality of Advice Review, new CoreData research shows there’s a high level of scepticism among financial advisers about whether the review will achieve the aims set out for it.

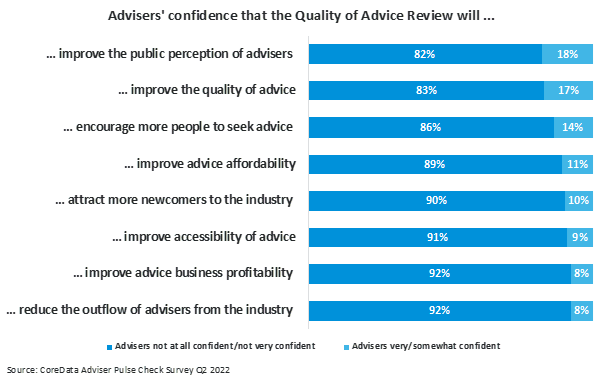

CoreData’s latest quarterly Adviser Pulse Check Survey shows that a significant majority (83 per cent) of advisers are not confident at all or not very confident that the review will improve the quality of advice.

But frankly, the quality of financial advice has never really been the major issue holding the profession back, despite the name given to the latest in a long line of reviews. The more pressing issues are the accessibility and affordability of advice. Both these things have taken a downturn as the cost of advice has continued to escalate.

Ironically, the declines in both affordability and accessibility have been driven in no small part by legislation designed to do precisely the opposite.

Remember the Future of Financial Advice (FoFA) reforms? Treasury’s website says the objectives of FoFA were to “improve the trust and confidence of Australian retail investors in the financial services sector and ensure the availability, accessibility and affordability of high-quality financial advice”.

FoFA did some good and necessary things. It didn’t make advice more affordable, and it didn’t lead to people flocking to advisers’ doors. But we digress.

A significant proportion of advisers (89 per cent) are not confident at all or not very confident that the review will improve advice affordability, and nine in 10 (91 per cent) are not confident at all or not very confident it will address accessibility.

That’s not to say the review won’t succeed in addressing both these issues, and more. It might, and it’s best to reserve judgement until we see what the review recommends and the factors it considered in making those recommendations.

It’s just that at this point of the process, the review doesn’t have the confidence of advisers. They’re overwhelmingly not confident that the review can achieve several other key outcomes for the profession either.

And that’s a shame, because around three quarters (73 per cent) of advisers strongly or somewhat support the review, so there’s no lack of goodwill within the industry for the review to succeed.

If review lead Michelle Levy makes the right recommendations and if those recommendations are accepted and implemented effectively by government, it could represent a great step forward for a professional that has perennially struggled to service more than around 15 to 20 per cent of the adult population.

Making advice more affordable and accessible would mean it could be offered at a price that doesn’t put people off seeking it, and offered to them at a time in their lives when it is likely to make a noticeable difference. And the more people who receive high quality advice and understand its benefits, the better off they will be and the better off the profession will be as these new experiences are discussed with families and friends.

Of course – as we discussed here a few weeks ago – increasing demand for financial advice is a fine objective, but there are clear issues around the supply of advice and the capacity of advisers individually to take on many more new clients.

But what a problem to have.

Leave a Comment

You must be logged in to post a comment.