The regulator’s update to Australian financial services licensees last week was a timely reminder that social media is a double-edged sword. It is an effective and cheap way to reach a significant number of clients (and potential clients), but there’s a fine line between that and wandering into a potential regulatory minefield.

ASIC basically advised both those who are active on various platforms, and any licensees they are associated with, to take it easy when it comes to the sort of information they push out on the socials. Anything that might be construed as financial product advice is a no-go zone.

As ASIC pointed out, it’s sometimes easy to stray into financial product advice, even unwittingly. But ignorance is no defence, and anyone found providing financial product advice on social media could face some strong penalties.

That’s not to say social media doesn’t have a legitimate place in the communication and marketing armoury of properly authorised financial advisers. It does, and many advisers use it very well to stay in touch with existing clients and as a way of establishing a presence with potential clients.

Social media is fine to use when sharing facts about a financial product (or class of financial product) and you constrain yourself to describing the features or terms and conditions of that product or class of product.

But the moment you enter the realm of making any sort of recommendation that someone invest in (or sell) a financial product or class of product, then you’re straying into dangerous territory. At the very least you need to be licensed or an authorised representative of a licensee, and that’s where social media finfluencers may come unstuck.

ASIC’s own research suggests almost three in 10 (28 per cent) people aged 18 to 21 follow at least one finfluencer, and of those that do, two-thirds (67 per cent) have changed their behaviour as a result of what that finfluencer has told them. On the face of it, that looks like a challenge to the traditional financial advice model.

But recent CoreData research suggests strongly that people are not going to turn to social media in any great numbers to seek financial advice, and that a greater challenge to financial advisers as a trusted source of advice and information is likely to come from a growing legion of websites and apps.

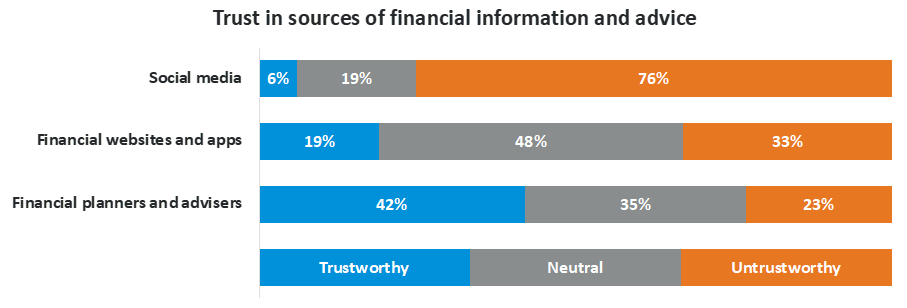

CoreData’s Trust in Financial Services Survey in the last quarter of 2021 confirms that social media simply lacks credibility when it comes to being a source of financial advice. Overall, more than nine in 10 consumers think social media is untrustworthy. Trust in social media peaks among those aged 30 to 39, but even then, fewer than two in 10 (17 per cent) say they trust it.

Fewer than one in 15 people (6 per cent) say they’d turn to social media for anything at all to do with their finances, even if they acknowledge there are elements of their financial situation they’d like to improve.

More than three-quarters (76 per cent) of consumers who have never received advice before say they do not trust information and advice about financial issues provided by social media influencers. Only 6 per cent say they trust it.

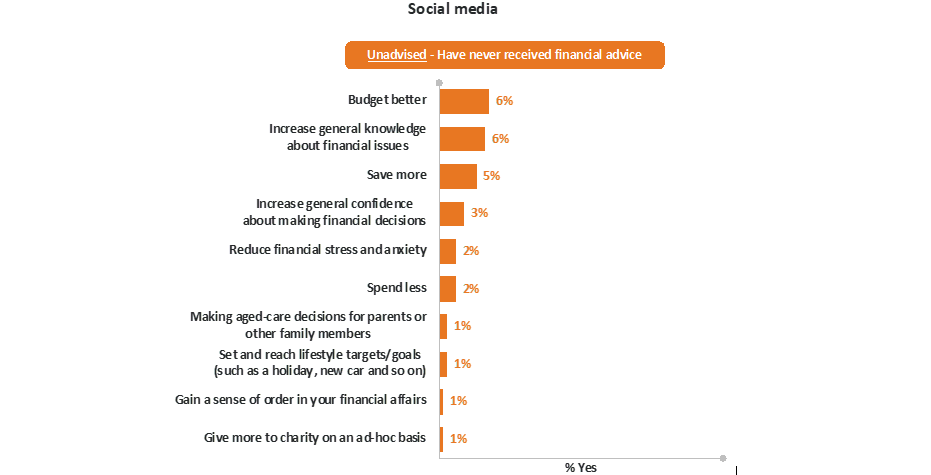

Those few consumers who would turn to social media would do so only for really simple things, like learning how to budget better, increasing their knowledge about financial issues, and getting tips on how to save a bit more.

Financial advice, on the other hand, is considered trustworthy by around half (51 per cent) of all consumers. Even four in 10 (42 per cent) consumers who have never received advice before still think information and advice about financial issues provided by qualified financial planners and advisers can be trusted.

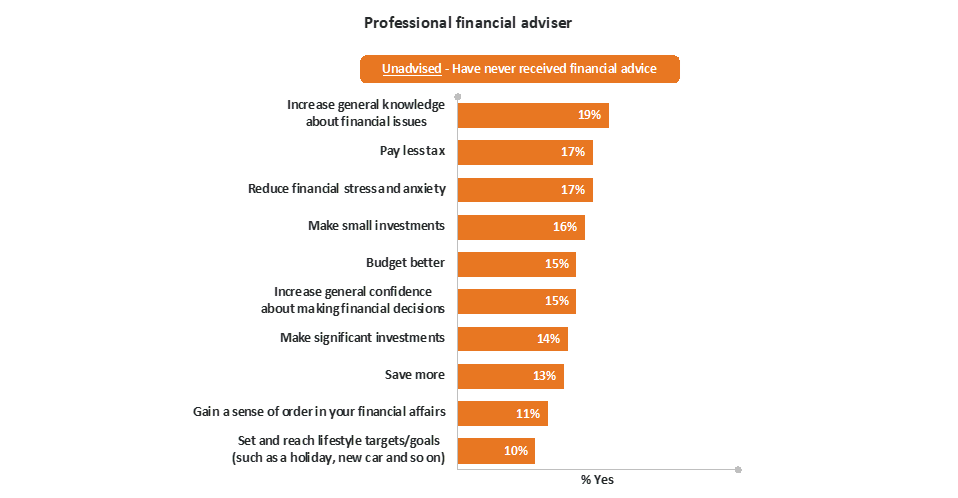

That means around seven times as many people say they trust information and advice from advisers as say they trust it from social media. Around one in five (19 per cent) of consumers who’ve never received advice before say they’d trust a professional financial adviser to help them with financial issues, and these are often more complex issues than consumers would turn to social media for help with. They include paying less tax, increasing confidence about making financial decisions, making investments, reducing stress and anxiety, and increasing their general knowledge about financial issues.

If financial advisers and social media influencers are at opposite ends of the trust and credibility scale, there’s a middle ground rapidly being occupied by a growing number of websites and apps.

These range in sophistication from simple front ends for funnelling money into portfolios of ETFs, call it advice and charge an asset-based fee; to apps and websites that are completely de-coupled from financial products and focus instead on improving a user’s financial health and wellbeing through paying down debt, maximising super contributions and having adequate life insurance – all for a flat fee or subscription.

These websites and their associated apps may prove in the longer run to be the bigger challenge to financial advisers.

In the minds of consumers, these digital providers potentially serve some of the same uses as advisers, even if fewer unadvised consumers say they would use them than would use advisers.

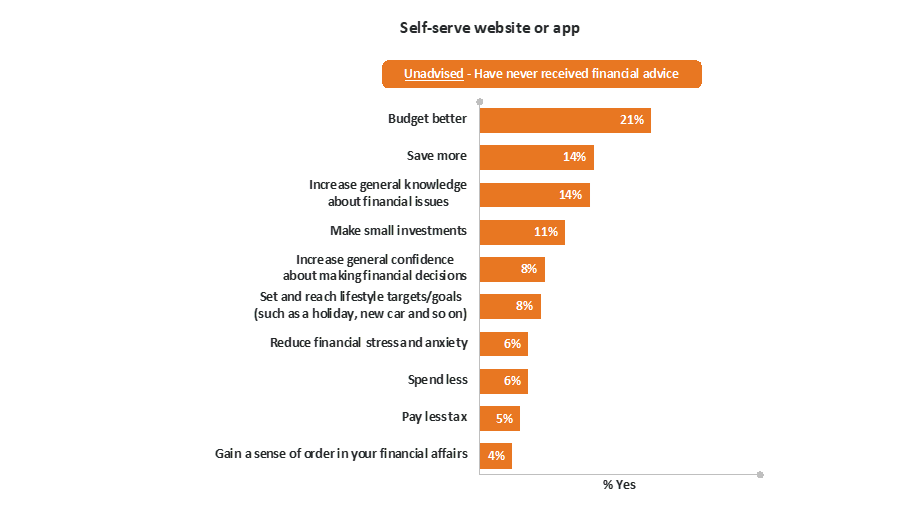

Around one in five (21 per cent) unadvised consumers say they’d use an app or a website to help them budget better, and around one in seven (14 per cent) say they’d use them to learn how to save more and increase their general knowledge about financial issues. Around one in nine (11 per cent) say they’d use apps or websites to make small investments.

Websites and apps are considered more trustworthy than social media, with around two in 10 (19 per cent) unadvised consumers saying information and advice about financial issues provided by financial websites or apps is trustworthy.

Significantly, however, around one in three (33 per cent) think the information and advice is untrustworthy, so even though they’re a mile ahead of social media finfluencers there’s still some distance to go before they’re in the same trust league as financial advisers.

What’s clear, though, is that the market for financial advice is fragmenting and even as access to advice declines as adviser numbers dwindle, digital alternatives are catching the eye of potential clients. It’s these alternatives that advisers need to keep closer tabs on. There may be opportunities for advisers themselves to co-operate with these providers and deliver relatively simple, low-cost services to a segment of the market not yet ready for full-scale financial advice.

While all this is going on, it’s interesting to see how the banks are faring. Having vacated the face-to-face advice business over the past two years, it might not have been surprising to see them start to try to serve their customers with a digital offering of some sort.

If that has indeed been their strategy, one might say it has had limited success. Around six in 10 consumers (59 per cent) do not even know if their bank offers a budgeting or financial management tool either as an app or in a website. About one in four (27 per cent) say their bank does but, of those, three out of four (75 per cent) say they do not use it.

Leave a Comment

You must be logged in to post a comment.