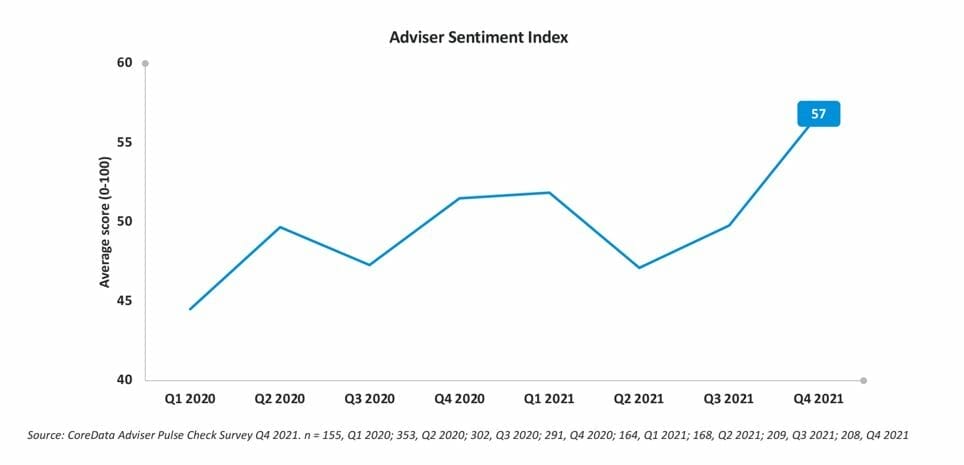

Here’s some good news to finish off what has been a long and in many ways challenging and exhausting year. CoreData’s Adviser Sentiment Index shows that financial advisers are feeling the best about the outlook for their profession and their businesses than they have at any time since we first started asking them back in first quarter of 2020.

At a level of 57, the index has never been higher. It suggests that the fog of COVID-19, exam deadlines and the disruption of other regulatory changes may be lifting.

CoreData’s statistical hardheads always remind me to be wary of a single quarter’s numbers, so it’s with guarded optimism that I bring you the latest index results. But it’s a better to be talking about the outlook getting brighter than it is to be reporting another gloomy quarter.

CoreData’s statistical hardheads always remind me to be wary of a single quarter’s numbers, so it’s with guarded optimism that I bring you the latest index results. But it’s a better to be talking about the outlook getting brighter than it is to be reporting another gloomy quarter.

So it’s also with guarded optimism that I can tell you the proportion of financial advisers who think the outlook for the financial planning profession itself will be worse in three months’ time has fallen significantly from last quarter. In Q3 2021, more than four in 10 (43.5 per cent) advisers thought the outlook for the industry for the next three months was somewhat or significantly worse; in Q4 the proportion was fewer than three in 10 (27.9 per cent).

It’s tricky to pinpoint a specific event that may have sparked this improvement; it may just be that after all this time of living with change, the attendant disruption has simply become background noise for advisers and advice practices, and that there’s head space to think about the future and where opportunities lie and where growth may come from.

It could also be that the clean-out of the industry that has taken place has pared it back to a smaller core of advisers who are able and willing to adapt to the new world of professionalism, educational standards and ethics and who see a bright future as a consequence.

Of course, it could be something else altogether. Maybe the stellar performance of the Australian sharemarket over 2021 is feeding adviser optimism. The S&P/ASX200 Index is up 12 or 13 per cent over the past year, so you never know. Or maybe it’s just the possibility of lockdown restrictions ending that made everyone irrationally exuberant.

Whatever is driving it, more than two-thirds (68.8 per cent) of advisers say current business conditions are good or excellent, up from fewer than six in 10 (59.8 per cent) who said the same thing last quarter. Almost three-quarters (72.1 per cent) of advisers forecast revenue growth for the next 12 months of 10 per cent or more, up from 61.2 per cent who made the same forecast in Q3.

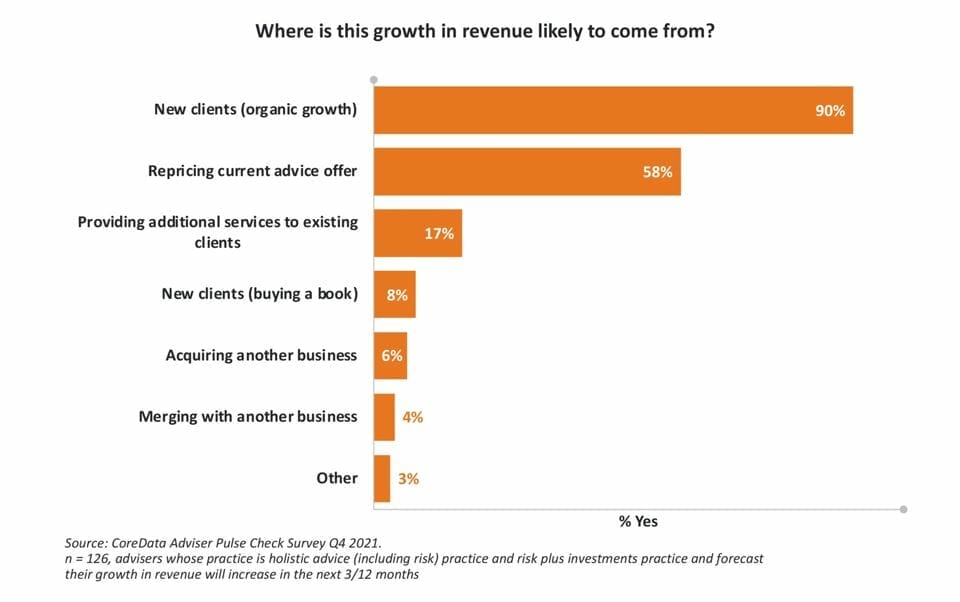

As always, growth is most frequently expected to come from organic growth in client numbers, with a fair bit of repricing of advice services, and a smattering of providing additional services and growth by acquisition.

CoreData’s Q4 Adviser Pulse Check Survey was in field at a time when advisers and licensees were being hit with multiple new rounds of regulatory change, including the much-maligned design and distribution obligations (DDO) and breach reporting requirements.

CoreData’s Q4 Adviser Pulse Check Survey was in field at a time when advisers and licensees were being hit with multiple new rounds of regulatory change, including the much-maligned design and distribution obligations (DDO) and breach reporting requirements.

Already reports are filtering through of licensees being forced to report breaches to ASIC because of incredibly trivial issues like clients being charged $20-odd in fees because an advice service fee wasn’t switched off exactly on a specific date.

It can’t only be advisers and licensees who are jack of this sort of regulation; the regulator itself could quickly be swamped with trivial issues required by law to be reported to it, at a time when we really do want its attention focused on the things that really matter.

Even so, those developments clearly haven’t dampened sentiment and we approach the end of 2021 on a bit of a high. Goodness knows we need one (even though, at the time of writing, it’s more than a month until year’s end so there’s still time for the wheels to fall off).

What unfolds in the first quarter of 2022 and beyond remains to be seen, but CoreData will be out there again, asking advisers what they think and how they’re feeling.

We’d love to hear from you when we do.

Leave a Comment

You must be logged in to post a comment.