In survey after survey financial advisers tell us two things. Well, they tell us a lot more than two things, but there’s two things in particular we’ll focus on here. One is that the number one source of business growth in the coming 12 months will be new clients; and the other is that one of the biggest impediments they face in growing their business is the capacity to onboard new clients.

At first glance that seems contradictory, but closer consideration suggests it is not. It’s not only possible but seems increasingly to be the case that new clients will drive growth, and at the same time onboarding new clients is becoming more protracted, time-consuming and increasingly costly.

Onboarding clients is becoming “harder, longer and more expensive”, as one adviser in CoreData’s most recent Adviser Pulse Check survey perfectly put it, mostly as a result of increased regulatory requirements, some imposed by the actual law itself and some imposed by specific licensees. Most advisers have a prospect-to-client conversion rate of about one in three, and that’s regardless of how many clients the adviser’s practice currently has.

About 70 per cent of small practices have a one-in-three conversion rate, as do about 74 per cent of medium practices, and about 80 per cent of large practices.

And it typically takes about three months from an adviser first meeting a prospect to them becoming a new client. In this context we define “becoming a new client” as being when they are first invoiced or charged for advice.

Small firms tend to take a bit longer to onboard a new client – around a quarter of them take three months or longer, compared to about 15 per cent of medium firms and 13 per cent of large firms. That may reflect the smaller firms’ capacity for holding meetings: irrespective of practice size it typically takes two to three meetings to convert the prospect to a client, suggesting larger firms hold the prospect meetings closer together.

The small number of meetings might reflect the fact that for well over half of all advice practices, irrespective of size, the primary source of new clients is referrals from existing clients, so these prospects are warm and generally well qualified.

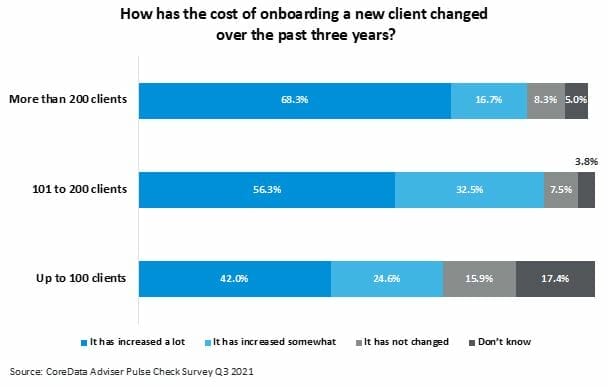

But we start to see more significant divergence of experience in how much the cost to onboard a new client has changed in the past three years. More than two-thirds of large practices say costs have increased “a lot” in the past three years, compared to about 56 per cent of medium firms and less than half of small firms.

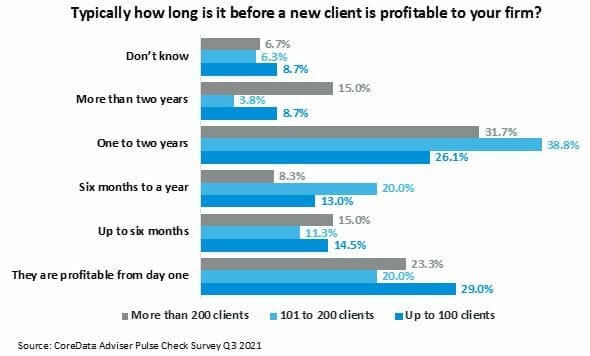

It typically takes up to two years for a new client to become profitable to an advice firm. While around two in 10 medium and large advice firms say new clients are profitable from day one, and around three in 10 small firms say the same thing, they’re far from a majority.

It typically takes up to two years for a new client to become profitable to an advice firm. While around two in 10 medium and large advice firms say new clients are profitable from day one, and around three in 10 small firms say the same thing, they’re far from a majority.

Around 15 per cent of large firms say it takes them more than two years to turn a profit on a new client. Between 6 per cent and 8 per cent of all firms say they do not know how long it takes a new client to become profitable.

And we see some of the reasons for this in the fact that no more than half of advice practices of any size charge a fee for initial advice that covers the cost of onboarding a new client – 50 per cent of large firms say they cover the cost, along with 47.5 per cent of medium firms and 46.4 per cent of small firms.

Advice practices need to respond to these forces and trends. The obvious response to raise advice fees, and it’s true that in the past 12 months there’s been a general repricing of advice services across the industry, with more to come in the year ahead.

Few advisers take pleasure in turning prospective clients away, and there’s a new, emerging approach for how they can avoid having to do that altogether. Some are starting to explore alternative service packages for clients whom they are unable or unwilling to charge a fee that will cover the cost of onboarding or make the new client profitable more quickly.

Sometimes these clients can be the offspring of existing clients, with whom an adviser wants to maintain a good relationship in anticipation of the offspring becoming a suitable client at some point in the future – through, say, an inheritance of wealth.

It’s a sort of “advice triage” service, or a service to make a prospect “advice-fit”. These services can be offered at low cost, without the provision of personal advice to the client.

They keep the client in the advice practice’s orbit and generating fees until the client reaches a stage where onboarding them as a full-service client, or at least as a client being offered personal advice, can be both profitable to the practice and of genuine value to the client.

They can be client-driven investment services or platforms, budgeting and financial management services – whatever the advice practice perceives to be of value to and suitable for a prospective client at their particular stage of financial life before they can be regarded as suitable for onboarding.

Making advice more affordable and accessible to more people is a noble and desirable aim. But the rising cost of advice seems to work against this objective, and so it seems inevitable that new, innovative and relatively low-cost “pre-advice” services must come into the mix.

Leave a Comment

You must be logged in to post a comment.