Research out of the US shows financial advisers are far happier than the average person, but that sense of joy is tempered at certain points linked to revenue generation, the role they play at work and the amount of time they have away from the job.

Ultimately, US adviser and blogger Michal Kitces concludes, rising revenue can increase well-being to a certain point ($1.5 million USD, as it were), but the key for “happy growth” among advisers is maximising revenue per client.

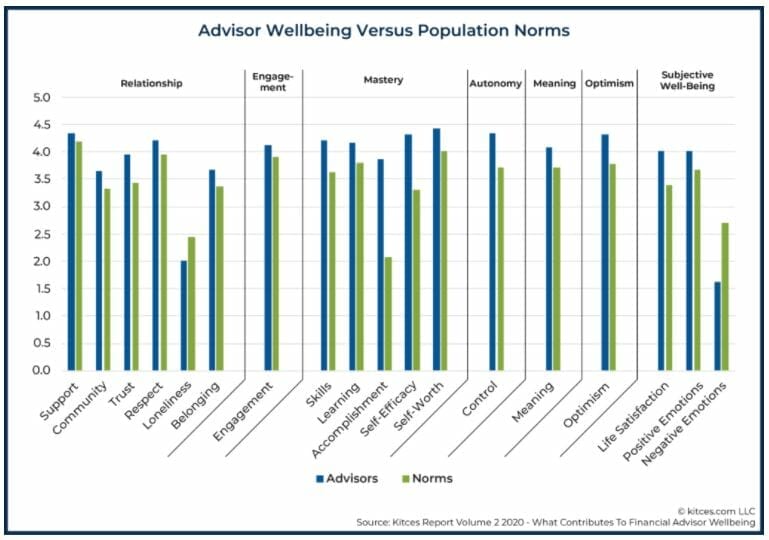

“Relative to general population norms, financial advisors score above average on every subscale of wellbeing in the CIT,” the research report states, referring to a well-known positivity measure called the Comprehensive Inventory of Thriving.

The CIT contains 18 different ‘subscales’ that address well-being in areas like relationships, mastery, meaning and self-worth. US advisers outscored the general populous in every one, and by a significant margin on accomplishment and self-efficacy.

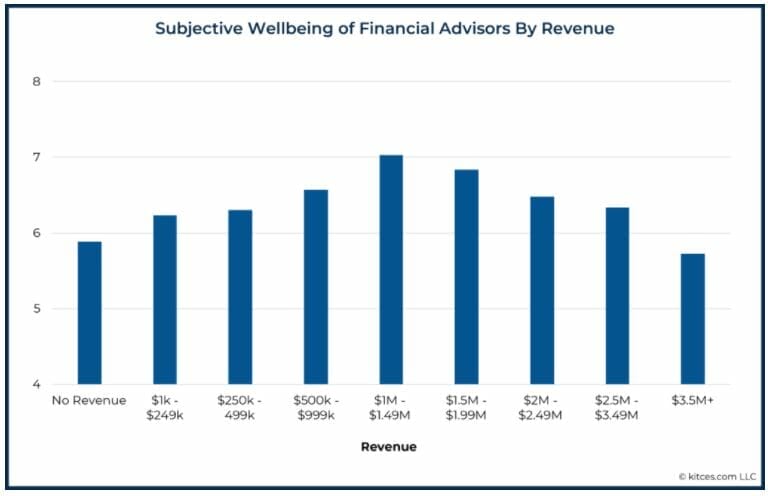

Adviser well-being increases as income increases, the research continues, but the same doesn’t hold true with revenue despite the two being linked.

Adviser well-being increases as income increases, the research continues, but the same doesn’t hold true with revenue despite the two being linked.

“Our research shows that once revenue crosses $1.5M (USD), subjective well-being gets steadily worse as revenue continues to grow,” it states. “In fact, not only does wellbeing cease to rise above $1.5M of revenue, but by the time advisory firms reach $3.5M+ of revenue – typically associated with $500M+ of assets under management – advisor wellbeing is lower than it ever was, even in the earliest days when advisors have the fewest clients and least revenue and the most early stage growth stress.”

Capacity walls

While adviser well-being generally goes up in line with revenue increases up to $1.5M(USD), Kitces and co-author Meghaan Lurtz note that even with elevated levels of well-being, the journey to happiness is marked with regular drops in well-being that are linked to capacity.

Advisers get happier as they succeed, but that happiness comes in waves that taper off as advisers gather more revenue but with the same amount of support. When more staff are hired or systems are upgraded, the well-being levels shoot straight back up again.

“As revenue grows to advisor capacity thresholds, well-being declines because the firm reaches its time-intensive capacity limitations,” the report states, “followed by a rebound in advisor wellbeing as staff are eventually added, and the capacity pressure is relieved to grow to the next tier.”

The key point, it says, is that adviser happiness doesn’t simply rise steadily as revenue increases because the capacity of the business and the adviser’s free time are also inextricably linked to well-being.

An unfulfilling position

So why does adviser well-being peak at a certain revenue point before declining irretrievably?

In short, it’s because successful advisers scale up and hire other advisers.

“At that point, the founding advisor’s role is no longer about meeting with and serving clients at all. It’s about managing other advisors to meet with and serve clients. For which the founding advisor must spend more time and receive (relatively) less incremental income,” the report says.

As the team grows the amount of time required to manage that team grows, “…which also means the founding advisor is spending less and less time serving clients… the one thing that they most wanted to do when they started the firm.”

The job advisers love and are good at, in this context, has been replaced by a role managing staff and business budgets.

“The personal gratification gleaned from those close relationships with clients, and even the way financial planners may have been able to structure their day around clients, is now gone, and that is a difficult and often unmotivating, possibly fairly unfulfilling position to be in…”

The key to ‘happy growth’

For advisers to have their best chance at enjoying well-being through their professional career, the Kitces report concludes that maximising revenue per client (as opposed to revenue) should be the focus.

Higher fee paying clients naturally take more time to service, he says, yet the foundational elements of advice – meeting with clients, preparing for meetings etc – remain comparable for much higher revenue.

“The key to ‘happy growth’ is not just adding more clients, but specifically increasing revenue per client to allow advisors to do their most rewarding work,” the report states.

Of course, the report’s premise is a generalisation in itself. Not everyone follows the same happiness pattern, and some advisers enjoy the transition to management. The point being made by the Kitces team is that advisers should do what makes them happy and control their own outcomes.

“Because in the end, we all have our own motivators from which we derive our happiness and wellbeing. The real key to success is not to follow any one specific prescription for success. It’s to get clear on our own definition… and then focus relentlessly on pursuing that vision.”

*Find the full article Lifting Advisor Wellbeing By Focusing On Time And Income Over Revenue Alone here

Leave a Comment

You must be logged in to post a comment.