If a career in financial services doesn’t work out for Paul Barrett then he could seemingly make a decent living as a chippie: he’s hit the nail on the head with his recent column about the affordability of financial advice.

Barrett argues that life, and finance, are complex and therefore financial advice is complex and has a price tag to reflect this. Rather than looking for ways to reduce the price of advice, the industry should revel in the complexity of the issues it solves for its clients and be unashamed about the cost of its services.

Of course, cost is half the equation. The other half is value. If consumers perceive value in something they will pay for it. But if they can’t perceive value, they’ll focus on the only number they can, which is the price.

Part of the problem the financial advice industry faces, and in fact has always faced, is that individuals often don’t fully appreciate the value of advice until they have experienced it for themselves.

They can listen to other people talking about how much advice has helped them (and often they’ll follow a friend or relative’s referral to an adviser), and they hear the industry and advisers talking about how advice changes lives, but there remains no substitute for first-hand experience.

Partly that’s because advice is, perhaps above all, a service and largely intangible. It’s also because sometimes the benefits of advice don’t manifest until some years down the track, once a strategy and a plan has had time to do its thing. It’s difficult for a consumer to attach value today to something they might not get for a few years from now.

Certainly, advice can solve some immediate issues, just as a medical practitioner might fix an immediate problem, or a lawyer might make a pressing legal issue go away, or an accountant or tax agent might save you a few bucks on this year’s tax return.

In the True Value of Advice Research Report, IOOF and CoreData went some way to demonstrating what advised clients value in advice and what unadvised individuals would value in advice, if only they were to seek it out.

In parallel research, CoreData has also found some evidence to suggest that once a consumer is on the advice path they have a reasonable tolerance for price increases.

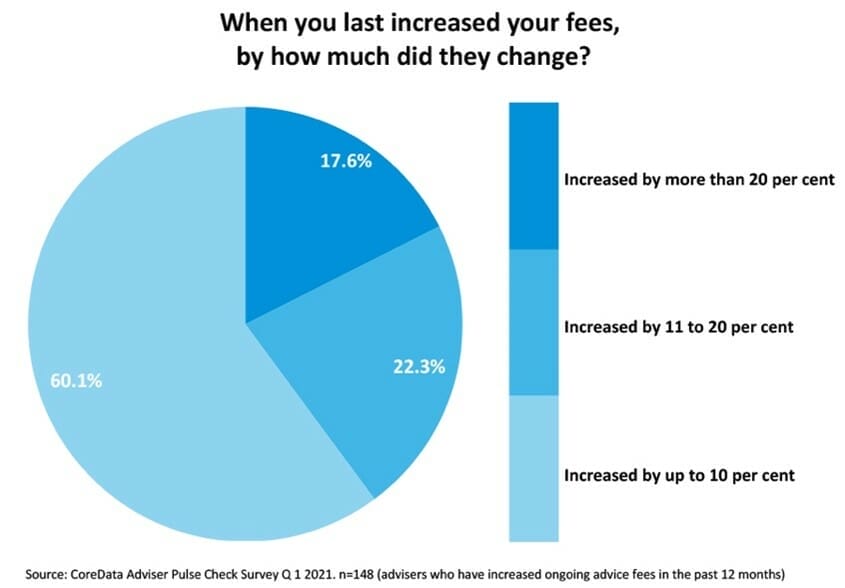

In the first quarter of 2021 we asked advisers how recently they had increased their fee for initial and ongoing advice. Around half (52.0 per cent) had increased their fee for initial advice within the previous six months, and around half (47.4 per cent) had increased their fee for ongoing advice. A further one in five had increased their fees (17.8 per cent for initial advice and 20.4 per cent of ongoing advice) in the previous six months to a year.

But that’s not the end of it. Almost half (46.7 per cent) plan to increase their initial advice fee in the coming six months and around one on three (30.9 per cent) plan to lift the fee within six to 12 months. Around half (46.1 per cent) plan to increase their fee for ongoing advice and around a third (30.3 per cent) plan to increase the fee in the next six to 12 months. The repricing of financial advice is well and truly on – and the increase being reported in come cases are not trivial (these increases are over and above any adjustments made for inflation).

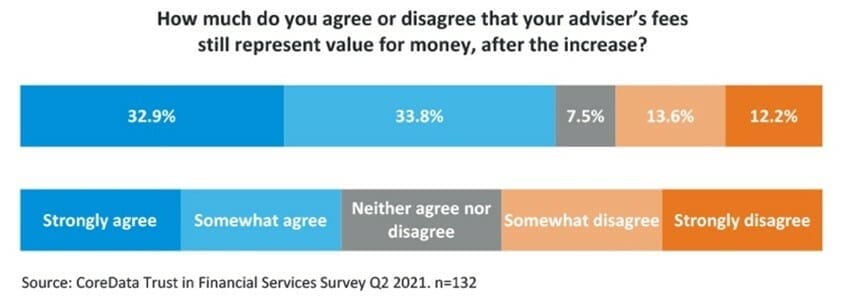

But so far, there’s little evidence emerging that consumers are starting to thing advice is too pricey. Again, this is likely to be because advised consumers understand the value of advice, and when their adviser increases the cost most of them continue to think they’re still getting value for money. A caveat here is that we received responses from only 132 advised consumers whose adviser has increased the fee they charge in the past year, so it’s a small sample. But it’s an interesting indicator nonetheless.

We often hear figures within the industry bemoaning the fact that not enough people currently receive advice, and wringing their hands over what can be done to lower the cost to encourage more people to take it up.

We often hear figures within the industry bemoaning the fact that not enough people currently receive advice, and wringing their hands over what can be done to lower the cost to encourage more people to take it up.

But Barrett’s column reveals an alternative perspective, partly that of an economic rationalist and partly that of someone whose livelihood depends on advice businesses being profitable. There’s nothing wrong with either of those perspectives.

We know financial advice cannot be delivered to every Australian. There will always be some who simply do not see the need for it, those who prefer to do it themselves and, yes, those what will never see sufficient value in it.

Barrett says the number of individuals who pursue careers in other professions, specifically law and medicine, don’t only do so because of TV programs like Grey’s Anatomy or Suits, it’s also because these professions are well paid, and practitioners can make an excellent living while also making a big difference to other people’s lives. But shows like these also reflect the fact that professions enjoy a privileged position in society. So, eventually, should financial advice, once all the pieces of the professionalism puzzle are in place.

The only TV series I can think of, off the top of my head, that has a financial adviser as its main protagonist is the Netflix series Ozark. In this show (spoiler alert) the adviser, though a series of unwise decisions by his former business partner, ends up putting his expertise to work running a casino to launder money for a drug cartel.

Maybe that’s not the best example.

Leave a Comment

You must be logged in to post a comment.