It’s often said that clients of financial advisers should be allowed to choose for themselves how they pay for advice. The client-choice argument is often advanced in support of asset-based fees. In the current environment, where asset values have plunged, client portfolios have shrunk in value and advisers’ incomes have declined, it’s an issue worth revisiting.

It’s true that advisers whose principle source of revenue is a fee calculated on the value of client funds invested have “skin in the game” and share their client’s interests in generating positive investment returns. It’s also true that asset-based fees are easy to calculate and to collect.

Even so, to say the primary attraction of an asset-based fee is that the adviser shares the client’s interest in generating positive investment returns suggests that advisers who charge in other ways don’t have the same interest. It also suggests these advisers who don’t charge asset-based fees don’t face a risk to revenue if they provide poor investment advice; that argument has been weakened by the fact that it’s never been easier for clients to opt out of receiving advice services if they’re not satisfied.

Asset-based fees place the viability of an adviser’s business at the whim of the markets, and it’s debatable whether exposure to a market event that could wipe out an adviser’s business is actually in the long-term interests of that adviser’s clients. Calculating the price of advice according to the value of a client’s portfolio ignores the intrinsic value of advice itself.

And the financial advice industry desperately needs advice itself to be regarded as valuable if the industry is ever to be regarded as a profession.

What consumers say they want

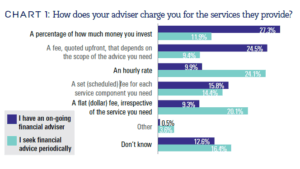

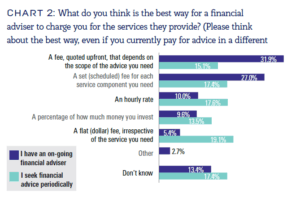

But in any case, CoreData’s research suggests that if you do let consumers choose how they pay for advice, not many of them will choose an asset-based fee. Earlier this year we asked financial advice clients how they currently pay for the advice they get, if they know (Chart 1 – below); and how they would prefer to pay for advice, if they have a preference (Chart 2 – below).

Around three in 10 (27.3 per cent) clients who have an ongoing relationship with an adviser

currently pay a fee based on a percentage of the funds they have invested. Yet fewer than one in 10 (9.6 per cent) of those same clients say that’s how they would prefer to pay.

By far the preferred method of paying for advice is a fee, quoted upfront, that depends on the scope of the advice they need – almost a third (32.7 per cent) of people who already have an adviser say they would prefer to pay this way.

As many clients (10.0 per cent) would prefer to pay an hourly fee for advice as would prefer to pay a percentage of the money they invest. It should also be noted at around one in eight (12.6 per cent) of clients with an ongoing advice relationship do not know how they currently pay for the advice they receive; and a similar proportion (13.4

per cent) of them don’t know how they’d prefer to pay for advice.

As an aside, when CoreData asked people who do not currently have an adviser but are looking for one, fewer than one in 10 (8.1 per cent) said they’d choose an adviser based on the adviser’s promise of generating high investment returns.

This result undermines the argument for an investment-based advice value proposition; and if an investment-based value proposition is unappealing to consumers then it’s likely that asking them to pay for such a value proposition is likely to be just as unappealing.

Working out how to charge for advice as a professional service, rather than as the result of how much money clients have, is not rocket science and it’s not breaking any new ground to suggest that’s the way the industry should go. It is how other professional services firms already work.

When we determine the cost of our services we don’t link it to the ‘wealth’ of the client we’ll be working with. It makes no difference the process of costing out a piece of work whether the client is small or large, wealthy or relatively resource constrained.

Value the service, not the sale

For a professional services firm, which is what financial advice practices aspire to be, the value of the service is not derived from the wealth of the client, but from the education and experience of those working in the firm, and from the quality of service. Firms with better educated and qualified and more experienced advisers, delivering consistently high quality services, ought to be able to charge more than firms whose advisers are less experience and less highly qualified.

That means linking the value of the services a practitioner sells to the practitioner themselves, not to their clients’ portfolios. For any given service, the cost is calculated with reference to the adviser’s skills, experience expertise and qualifications – and it doesn’t matter if the client’s portfolio is worth $100,000 or $100,000,000.

If a hundred-million-dollar client pays more for advice it should be because the service they need is more complex or more extensive and demands a more skilled or experienced adviser, not because they invest more money per-se.

Financial planning is currently undergoing a critical transition and moving away from its roots as a sales-based occupation to one that sells professional services.

The transition is partly being driven by more enlightened members of the advice community; partly by regulation framed to address critical advice and behavioural failures of the past; and partly by the appalling publicity dished out by the Hayne royal commission.

Transition is often painful. But it’s not as painful as failing to change and evolve and sliding, unmissed and unlamented, into oblivion. Financial advisers are in the enviable position of being able to seize control of their destiny and make the transition work.

Financial planning’s reinvention depends on it adopting the practices and structure of a profession. Its practitioners have a clear choice. They can simply repeat the practices and behaviours of the past in the hope that something will change – that somehow it will suddenly capture the public imagination and people will flock to advisers’ offices in droves.

Or they can seize an opportunity and turn it into something different, and something valued in its own right. But that means letting go of some of the traditional ways of doing things and embracing change. And foremost among those is making it clear to consumers that financial advice is a professional service and that it should be valued as such.

Leave a Comment

You must be logged in to post a comment.