The financial planning industry routinely makes sense for its clients out of complex, convoluted and arcane taxation, social security and superannuation legislation. Adopting a new, industry-wide code of ethics for itself, therefore, should not be an unsurmountable challenge. Whatever struggles the industry is going through to adopt the new code should be worth it, given CoreData research shows that the impact on public trust in financial advice will be strongly positive.

FASEA’s Code of Ethics is designed to underpin and raise standards of professional and ethical behaviour. It does not replace or override the law. FASEA’s Financial Planners and Advisers Code of Ethics 2019 Guidance document explicitly states that the law takes precedence over the code if complying with the code would cause an adviser to break the law.

In all other scenarios and situations, the code is designed to allow a financial planner to exercise individual judgement on how best to deal with a client or a client’s situation, while also operating within the requirements of the law.

In essence, the code of ethics is asking financial planners to start to think like professionals. That may be the crux of the issue – in a world of tick-a-box compliance, it is new territory for some advisers and for some licensees, and it could help to explain the bamboozlement in certain quarters.

All professionals rely on experience, expertise and intellect to guide them through potentially tricky ethical situations with clients. They have worked out over many years how to do this, what’s acceptable and what’s not, often by consulting and collaborating with peers and colleagues. That’s the journey that the whole financial planning community is now embarking upon. It is part of the shift in thinking and behaving that financial planners signed up for when they decided they wanted to be treated and thought of as professionals.

“As with every profession, there is allowance for differences of professional opinion on how the ethical rules of the profession should apply in a particular case,” FASEA’s guidance says.

“Doing what is right will depend on the particular circumstances and requires you to exercise your professional judgement in the best interests of each of your clients” [emphasis added].

The guidance

Perhaps the code and guidance are proving a little difficult to assimilate because complying with a code of ethics doesn’t necessarily lend itself to simple yes-or-no answers. Nor can it be easily addressed by a prescriptive guide to compliance, the kind that advisers have grown up with and are used to. In many situations, the answer to the “best” course of action under the code will be: “it depends”.

All professionals inevitably encounter situations where a code of ethics appears to be at odds with the law, or where a code imposes behavioural conditions that are new or unexpected or at odds with historical commercial practice. That much is to be expected as professional behaviour and standards permeate the financial planning industry. Other professions cope with it.

Where FASEA’s guidance might have gone awry or caused confusion and concern is when it seeks to modify or change the impact or intent of an ethical standard.

A submission by the Financial Planning Association (FPA) on the code sums this up nicely and makes a lot of sense in an environment where sometimes the commentary borders on the non-sensical. As you’d expect, the FPA supports a code of ethics, having had one of its own for decades already. But it points out that FASEA can’t use its guidance document to try to modify the effect or intent of a legislated standard, because the guidance document itself has no legal standing. The code of ethics has been established by legislative instrument and the FPA says the guidance document “sits outside the legal powers bestowed on FASEA for setting the standards of the code of ethics”.

“It is important that codes and this code in particular raises trust, raises standards and protects consumers. It is therefore inappropriate for FASEA to introduce new requirements into the code via its guidance,” the FPA states.

And whether an adviser complies with the ethical standards in the way the guidance document suggests is doubly irrelevant, because even if FASEA were included to look kindly upon an adviser relying on its guidance, FASEA doesn’t actually monitor advisers’ compliance with the code anyway. That will be a new body that the government has yet to create, name, fund or staff.

Consumers like it

The FPA’s summary of the objectives of the code of ethics is correct. All of the education, professional and ethical standards developed by FASEA are designed to improve trust and confidence in the financial planning industry.

At the end of 2019 CoreData conducted its latest quarterly trust survey. Unsurprisingly, trust in financial advice has improved only minimally: in Q4 the trust score stood at 42.4 per cent*, up from 41.3 per cent the quarter before, and still some way below the 60.5 per cent figure predating the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

At its current rate of improvement it will take something in the order of four and a half years to get back to its pre-royal commission level, and that’s assuming there are no further setbacks along the way.

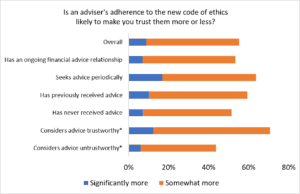

There may be a quicker way. In the same quarterly survey, CoreData asked respondents about their attitude towards a code of ethics. Almost nine out of 10 (85.9 per cent) of respondents say they didn’t know financial advisers are now legally required to comply with an industry-wide code of ethics. However, more than half (55.2 per cent) say they would trust advisers somewhat or significantly more if advisers were required to comply with a code of ethics.

As the below chart shows, the proportion of people who say they’d trust advisers somewhat or significantly more was broadly consistent irrespective of whether the individual has an ongoing advice relationship has previously received advice but doesn’t anymore or has never received advice. It seems to have the greatest impact on individuals who receive advice periodically.

*The trust score is calculated as the percentage of respondents who rank their trust in financial advice as a six on a scale from zero to 10, where zero means “no trust” and 10 means “total trust”. In the chart, “untrustworthy” is respondents who assigned a trust ranking ranging from zero to five, inclusive, and “trustworthy” means respondents who assigned a trust ranking ranging from six to 10, inclusive.

Furthermore, more than four in 10 (43.6 per cent) of people who say they do not currently trust financial advisers say they’d trust advisers somewhat or significantly more as a result of compliance with a code of ethics. And more than seven in 10 (70.9 per cent) people who already trust advisers say they would trust them even more.

So while there may be some consternation about the operation of the code, and advisers’ compliance with it, these results tend to suggest it’s worth persevering with, and promoting the existence of the code to the wider community.

Now it’s up to individuals

A code of ethics is a clear illustration of how ultimate responsibility for conduct within a profession lies with individual practitioners. In a financial planning profession, responsibility for behaviour and conduct devolves to individual advisers and is taken out of the hands of the entities – licensees and employers, basically – that have historically governed so much of how advisers behave and work.

“You have the primary obligation to regulate your own behaviour to comply with the code,” FASEA’s guidance says.

“You have a fundamental, personal, professional obligation to understand and to adhere to your ethical obligations under the code. You cannot outsource this responsibility to your employer, or your licensee, or any other person.”

Elsewhere FASEA’s guidance says each individual adviser must “be ready to give an account of how they have interpreted and applied the code in specific situations”.

“You may demonstrate engagement with the code by discussing the various case studies and your own experience with your professional peers and being willing to be challenged on your judgement,” it says.

“Discussion of the standards within the profession and with the public is encouraged and assists to demonstrate a willingness to meet the public’s expectations for the profession.”

In other words, a financial planner will be well on their way to meeting their obligations under the code of they can demonstrate that they’ve engaged with peers and colleagues to discuss issues and how to address or resolve them and can, if called upon, explain coherently why they did something in a particular way.

Among other things, if it weren’t already obvious, the introduction of the code makes it clear that anything a licensee wants an adviser to do must be ignored by the adviser if doing it will cause a breach of the code, unless the requested action is a legal requirement.

If any person or entity asks or tells an adviser do anything that will cause them to breach the code of ethics, let alone break the law, the adviser must refuse. On that issue, at least, there are no ifs and buts.

Leave a Comment

You must be logged in to post a comment.