In November in Canberra, the Profession of Independent Financial Advisers (PIFA) held its 2019 symposium, attended by the principals of around 30 financial advice firms that conform to the Corporations Act Section 923A definition of “independent”.

These are firms that do not receive commissions (or rebate them in full to the client), including on life insurance; do not charge asset- or volume-based fees; and have “no ties to product manufacturers” which may influence their actions or advice.

There aren’t many advice firms or licensees that meet this definition. Most fall foul of one or more of the forms of remuneration or structure that disqualify them from legally using the term “independent” to describe themselves or their services. The definition of independence is interesting and has been the subject of debate in the industry before. The government has agreed with the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry that advisers must give retail clients a statement explaining why the adviser is not independent, impartial and unbiased, before the adviser provides personal financial advice, unless the they are allowed to use those terms under s923A.

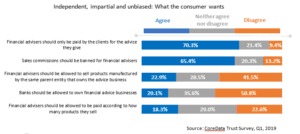

Characteristics of independence, impartiality and lack of bias are among those that consumers say they want in financial advisers (see chart below). But this is only one of the interesting things about PIFA and its members, and not even the most interesting one. In May this tiny association, headed by its president Daniel Brammall (pictured), formally lodged an application to establish a professional standards scheme.

Among other things, but the one most often spoken about, a professional standards scheme allows members to cap their civil legal liability. But it is so much more than that. It would establish, beyond reasonable question, financial advice as a profession.

The Professional Standards Councils (PSC), a group of independent statutory bodies which through the Professional Standards Authority (PSA) assess and approve applications for professional standards schemes, says schemes are “legal instruments that bind associations to monitor, enforce and improve the professional standards of their members, and protect consumers of professional services”.

That’s what a professional association does

The PSC’s statement is a clear articulation of what a professional association should be set up to do, and it reflects what the financial planning industry has been craving for so long. That PIFA has even made an application is testament to the unwavering commitment of the leadership and members of PIFA (formerly the Independent Financial Advisers Association of Australia), or IFAAA.

It’s not by coincidence that you’re reading this article in a publication called Professional Planner. It’s the first word that’s the important part of the name, and the publication was created because not all that long ago the idea of establishing financial advice as a profession was thought of as a terrific idea.

Professional Planner thought it was a good idea, too, but also recognised that not everyone (in fact, hardly anyone) in the industry really understood what creating a profession would require. It would take more than just nice offices, nice clothes and even behaving professionally (whatever that actually meant) towards clients. It would entail restructuring the industry, including setting higher education and ethical standards. It would require the the nexus between product and advice to be dismantled, leaving advice as a professional service as distinct from being a distribution function; and it would require a mechanism to enable members of the profession to monitor and police their own members (some call this self-regulation).

To use the jargon, financial advice would need to conform to the same cognitive, normative and organisational conventions that other professions conform to. This could not be fudged, and a profession could not be created just by claiming loudly enough and often enough that financial planning was one. It plainly was not, and it had work to do.

Hate to say ‘we told you so’, but …

A decade down the track what’s taking place within the advice industry is almost exactly what Professional Planner said would need to happen before a profession could be established. There was no particular genius to the insight; frankly, if a bunch of journalists and publishers understood it then it ought to have been painfully obvious to everyone in the industry. And since financial advice is not the first occupation to start the trek down the path to professionalism there was already a trail to follow, with easy-to-read signposts along the way, and a clear destination. In that respect it wasn’t a difficult publication to edit.

But along the way the profession lost its way. For every two steps forward, there was one step back. Some of the vital changes needed to create an environment where a profession could take hold had to be pushed onto the industry from outside – that is, by legislation and regulation – rather than emerging organically.

The industry couldn’t wean itself off product commissions or demonstrate unequivocally that it acted in the best interests of clients, so the Future of Financial Advice (FoFA) laws were introduced. It remained far too easy for individuals without the necessary education and ethical standards to get into the industry, and so the Financial Adviser Standards and Ethics Authority (FASEA) was born. And the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services industry drew an unimpeachable picture of the shoddy practices the industry continued to engage in, even as it claimed to be a profession. All of these things could and should have been tackled by the industry itself. But they weren’t.

And now, some are starting to question whether the goal of professionalism is still worth it at all. That’s what we infer they are doing, because it really can be nothing else when the creation of a profession hinges on successfully achieving the very changes they want to stop, circumvent or scale back.

The advisers in the box seat

So while the industry and its various associations continue to circle the drain on professionalism, PIFA has done a Bradbury (Olympic speed skating gold medalist Stephen Bradbury was MC at the PIFA November event). If PIFA is successful in establishing a professional standards scheme – and there is considerable work still to be done to get there – it will transform the nature of financial advice. Its members will be recognised as being in the vanguard of professionalising an industry that for decades seemed immune to being professionalised.

But it’s not going to be easy. PIFA will need to demonstrate to the PSC that it has the resources and infrastructure to operate effectively and discharge its obligations under the scheme, which are many and onerous. And this brings us to the issue of scale: PIFA is tiny. Its website lists 52 members (although other independent advisers exist who are not members). It is dwarfed by the Financial Planning Association of Australia (FPA) and even by the Association of Financial Advisers (AFA). How it funds what it needs to do with such a small membership base remains to be seen.

The key criteria for becoming a member of PIFA revolves around independence, and so few practices meet the legal definition that membership will inevitably remain small.

Recognising this, PIFA has introduced a new membership category. An adviser can join PIFA as an associate member, making a statement of intent to transform their advice business to comply with the Corporations Act definition of independent. Even though PIFA has developed resources and guidance on how to do that, it will continue to be a slow build.

Perhaps its lack of scale will be an advantage at this early stage, allowing PIFA to retain a commitment to the ideals and principles of independence and professionalism. A tougher test of its focus may arise when or if its membership expands significantly, and more divergent views and priorities come to the fore.

After all, it’s the perceived need to cater to all manner of views, opinions and vested interests, often espoused by a minority of members who are out-of-touch with the changing environment, that has played such a large part in holding other associations back from pursuing a full-on professionalisation agenda.

Leave a Comment

You must be logged in to post a comment.