It has been said the financial planning industry is suffering from reform fatigue, and that a seemingly endless stream of inquiries, reports and legislative changes has knocked the stuffing out of the industry and its practitioners.

Indeed, a significant proportion of advisers believes the recommendations of the latest inquiry, the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, simply go too far, new CoreData research has found.

It’s probably no surprise advisers feel this way, having already been buffeted by the Future of Financial Advice reforms, the Life Insurance Framework, Financial Adviser Standards and Ethics Authority education, ethics and professional standards, and umpteen other bouts of prodding and poking. The response is understandable.

What is striking in the new research, however, is how the attitudes of advisers and consumers differ.

While 45 per cent of advisers think the royal commission’s recommendations go too far, about 40 per cent of consumers think the recommendations don’t go far enough.

While 45 per cent of advisers think the royal commission’s recommendations go too far, about 40 per cent of consumers think the recommendations don’t go far enough.

There is a clear public desire for reform and for the financial services industry to be cleaned up in accordance with the royal commission’s recommendations as quickly as possible.

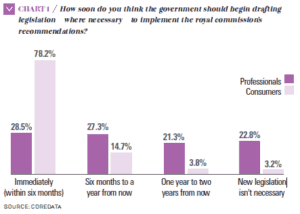

The research, based on responses from 403 professionals and 343 consumers, shows the public’s desire for rapid change differs dramatically, too. When asked how quickly the government should legislate, where necessary, to give effect to the royal commission’s 76 recommendations, about 29 per cent said immediately (which we defined as being within six months) and about the same number said within six months to a year. Roughly a fifth said one

to two years from now. On the other hand, more than three-quarters of consumers want legislation immediately.

This desired pace of change appears to be consistent with the finding that the proportion of consumers who think the inquiry’s recommendations will lead to significant improvements for them is twice as large as that of financial advisers.

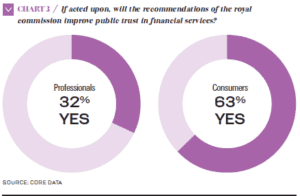

About 63 per cent of consumers say that, if acted upon, the recommendations of the royal commission would improve public trust in financial services. About the same proportion of advisers say the recommendations won’t improve trust – but on this issue, advisers are simply wrong. When you ask the public if they will trust financial services more, and they say they will, then by definition, public trust will improve.

About 63 per cent of consumers say that, if acted upon, the recommendations of the royal commission would improve public trust in financial services. About the same proportion of advisers say the recommendations won’t improve trust – but on this issue, advisers are simply wrong. When you ask the public if they will trust financial services more, and they say they will, then by definition, public trust will improve.

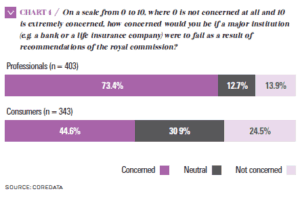

The public is also happy for the government to forge ahead full speed, and damn the torpedoes. Almost three-quarters of consumers say the inquiry’s recommendations should be adopted in their entirety, irrespective of unintended consequences for the institutions involved. A quarter of consumers say they would not be concerned if a major institution – a bank, for example, or a life insurance company – were to fail as a result of an inquiry recommendation.

While more than 45 per cent of consumers would be concerned if a major institution were to fail, it’s a significantly smaller proportion than the 73 per cent of advisers.

So what does all of this mean?

Trust in financial planning, in particular, declined from just over 60 per cent* at the beginning of 2018 to a low point of about 35 per cent in the third quarter of 2018. It bounced modestly in the fourth quarter of 2018, but in the first quarter of 2019, fell away again to about 36 per cent.

The people whose trust the industry needs to win back say the recommendations of the royal commission will help restore that trust; they are not particularly concerned about the potential impact of the recommendations on individual institutions or on the economy more broadly; and they want the changes to be made quickly.

But there’s a level of skepticism among consumers about whether the recommendations will make it through the next stage of the process intact.

But there’s a level of skepticism among consumers about whether the recommendations will make it through the next stage of the process intact.

Just under half of consumers think the recommendations will be watered down to suit the institutions, and a slightly smaller proportion believe they’ll be watered down to suit political objectives.

While we saw public opinion towards the royal commission change over the course of 2018, with the proportion of people agreeing with the statement that “at a cost of $75 million the royal commission is a waste of taxpayers’ money” declining from 42 per cent to 24 per cent, the major parties’ attitude towards reform will directly influence some voters at the ballot box.

Leave a Comment

You must be logged in to post a comment.