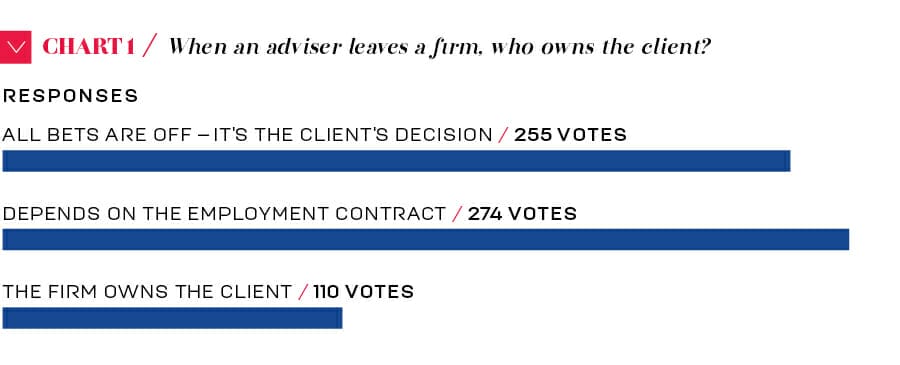

The question of client ownership is an easy one to answer, strictly speaking. The client owns the client and they have every right to direct patronage and loyalty as they see fit.

Yet in some cases they don’t get the chance.

Restraint and non-solicitation clauses in employment contracts can preclude clients from following advisers who leave a firm, leading to complicated commercial arrangements or, worse, contentious legal battles.

Charmian Holmes, solicitor director at The Fold Legal in Brisbane, calls it “a bit of a vexed question”.

“At law, there’s actually no ownership at all, and no such thing as owning a proprietary right to a client,” Holmes explains. “The only way a firm can hope to retain the custom of a client when an adviser leaves employment is to prevent the adviser from soliciting business from that client.”

Holmes says that while non-solicitation agreements are built into “about 98 per cent” of adviser employment contracts these days, disputes about who owns the right to service clients still regularly escalate into legal battles. She says there is an “amazing amount” of case law looking at these clauses in the context of financial planning, as firms will often seek an injunction to stop an adviser going after a client base. “These disputes are very, very common,” she says.

FIRMS CHASING WATERFALLS

How well a non-solicitation contract prevents an adviser from accepting work from a client depends on “the nature of language” used in the restraint clause and “the ability of the firm to enforce those terms at law”, Holmes explains.

Displaying contractual rigor means showing that the period of restraint is “reasonable for the protection of goodwill of the business”, Holmes says. Just how long is ‘reasonable’ for an adviser to be under restraint is a source of contention. To make sure firms are protected, Holmes says, agreements need to have stipulations that “cascade” or “waterfall”.

“There’s a real artform to these clauses now,” she explains. “They’ve got what’s called cascading restraints…You might start with 18 months and [the court] might say, ‘that’s not enforceable, it’s 12’. If that’s not enforceable, it’s nine, and if that’s not enforceable it’s six months.”

It is important for all financial services firms to keep their restraint clauses up to date with current case law developments. Part of that is staying abreast of what the courts generally believe is appropriate.

“The [longest] restraint you can really expect to impose on an employee is about 13 months,” she estimates. “If people are trying to include a fixed restraint period of two years, it won’t survive under scrutiny in the court. It’s got to be a cascading timeframe, with some [other, shorter times as options] to give the court some choices, because you’re better having something than nothing.”

Holmes says that while there have been “a few developments” in the last three years, “there hasn’t been a significant shift in the court’s view on what is a reasonable restraint period in the last two years”.

Sarah Abood, chief executive at Profile Financial Services, agrees that excessively punitive restraint agreements are a waste of time.

“Some of them have restraint clauses that couldn’t be enforced, seeking Australia-wide restraints for five years and so on – there’s no way the courts would uphold that,” Abood says. “If there is a contract in place with no waterfalls and the court takes the position that the clause is too harsh, then it just gets struck out and the employer gets no protection.”

LIKE A DIVORCE

Contractually, employers need to look at more than just restraint clauses for protection.

Much like in a divorce, Abood says, when a planner leaves a firm, the relationship is generally “not quite as strong as it used to be”. She says a robust employment contract should make it absolutely clear what happens if an adviser leaves, including buyout agreements.

“It makes much more sense to agree on these sorts of things early,” she says.

Commercial agreements whereby an adviser or their new firm will ‘buy’ selected clients from their former firm are common, she notes.

“When planners have joined Profile, we’ve been able to negotiate an arrangement where we basically support the planner in buying out their restraints on those clients,” she explains. “We say, ‘Look, these clients are really rusted on and they want to continue working with the adviser, can we have a commercial conversation about waving the planner’s restraint on these particular clients?’ ”

These deals are essential because trust is hard won between clients and professionals, and both parties benefit from maintaining the relationship. Paul Tynan from Connect Financial Service Brokers says, “If they’ve got a good relationship with the individual, they’ll follow the individual.”

Buyouts are also important because it can be difficult for clients to understand why, through no fault of their own, they may be prevented from following their adviser. If an agreement isn’t made, a frustrated client could leave both parties for another firm, which is a lose-lose-lose outcome.

The cost of buying a client varies but Tynan says prices have started to drop for “the first time in 20 years over the last six months”, due to restrictive upcoming adviser education standards and the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which will probably recommend an end to grandfathered commissions.

While client books have typically been sold at multiples of 2.8 to 3 times annual revenue, Tynan says this is now down to “2.5 or 2.6 times”.

SHADES OF GREY

Talk of buying and selling clients, while necessary, is uncouth and reflects poorly on advisers. Any discussion that refers to people as if they were chattel is demeaning, says David Simon, principal adviser and founder of Integral Private Wealth.

“You can’t treat customers like commodities or livestock, to be traded like cattle,” he says.

Simon’s perspective is rare. Prior to starting Integral, he was at Westpac’s BT from 2000 to 2015, rising to become its top adviser in Australia. His original employment contract was a generous one – only three months of non-solicitation – and by the time he left BT, he had an extremely profitable book of clients. However, instead of “taking the easy route” and poaching the clients after three months, Simon volunteered to buy the entire book.

He admits he could have saved himself “seven figures plus”, but felt he needed to pay respect to the relationship he had with his former employer.

“I was morally obliged to compensate the bank,” he says, “because I wouldn’t have met those clients if it wasn’t for Westpac.”

FIRMS MUST MAKE THEIR CASE

Despite this, Simon calls himself a “complete hypocrite” because he believes advisers should have every right to take clients with them if advice practices don’t do enough to retain them.

“I think it’s incumbent upon the firm,” he says. “If one of my advisers were to leave Integral and the client left with them, I would feel responsible.”

He argues it is the responsibility of firms to make clients feel like they are part of a community and that they have a relationship with the firm not just the adviser. He says chief executives and practice leaders need to make clients feel like they are part of a family not just “looking at reports and making sure people are paying their fees”.

“You’ve got to be present,” he says. “The [chief executives] need to make themselves known by hosting functions and meeting with the people who make up the community around them.”

Profile’s Abood agrees and says it’s “not great to have pure key-person dependence”.

“The deepest and closest relationship a client has is probably with their adviser and that’s appropriate,” she continues. “But doing a great job, as a business, of presenting a broader team is important.”

The non-solicitation period gives an incumbent firm the chance to show clients that the service they value comes from not only the adviser but also the people and systems behind them. By nurturing more than one relationship with the client, she explains, “you at least have a chance to slow down a client’s decision to leave and introduce another planner”.

When an adviser does leave, Abood says, firms need to “get on the front foot” by acknowledging the situation, reintroducing the client to the team and introducing another adviser – all while being respectful of the previous planner’s position.

“If all they’ve heard is that their planner is leaving, and then they’ve heard nothing for weeks, then they’re far more likely to say, ‘Oh well, I guess I’ll be looking elsewhere,’ ” Abood says.

‘PURIFY MY SOUL’

When an adviser leaves a firm, the stakes can be incredibly high for both parties. A new job for an adviser is often predicated on a promise to bring over clients, with financial bonuses on the line. For firms that borrow money to buy a book of clients from another business, half of that book can walk out the door with the exiting adviser, while the debt remains.

Aside from contractual restraints and the will of the client, the adviser’s ethical reasoning is the only determinant when considering who owns the client.

Integral’s Simon was compelled to buy his book from Westpac out of respect and a sense of duty. He’s only half-joking when he says, “I guess I had to purify my soul.” But not every divorce is that cordial and firms need to do everything they can from both a legal and business perspective to ensure the client wants to stick with them.

“It depends on the individual ethics of the adviser,” Holmes says. “Some of them will say [the former practice] should have protected itself better, and they’ll be opportunistic about it. Others might say, ‘This is not the right thing for me to do.’ ”

Leave a Comment

You must be logged in to post a comment.