After an extended period of above-average volatility on Wall Street – and at home – during 2018, it seemed prudent to check the extent to which this has affected my volatility forecasts and, in turn, my preferred asset allocation between the ASX 200 and the S&P 500.

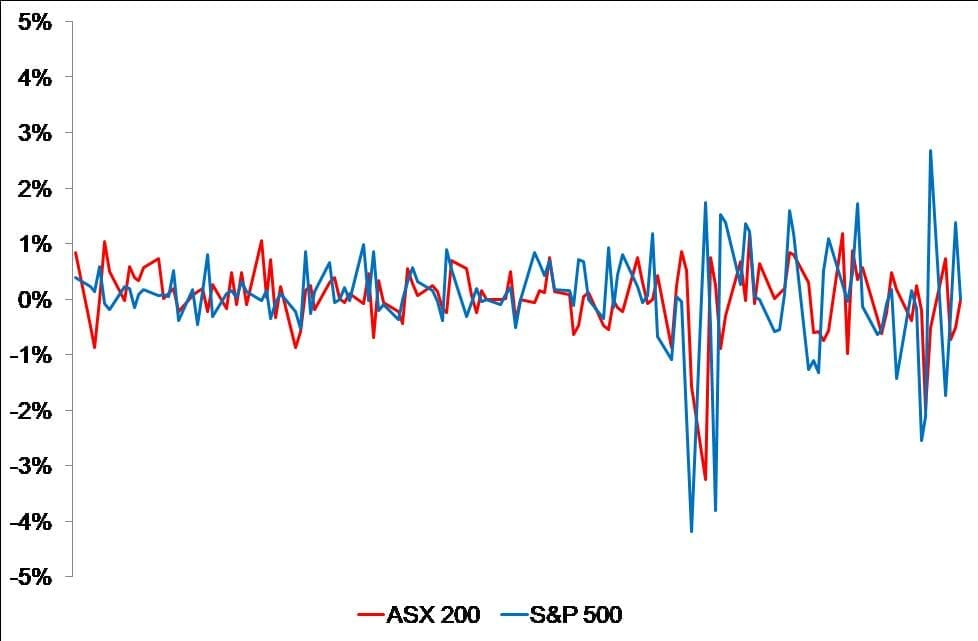

Up until February this year, markets had been particularly quiet, as can be seen in the chart. The recent increase might be attributed to a combination of factors – including changes in US inflation forecasts, the new Fed chairman, and President Donald Trump’s trade tariffs. The increase in ASX 200 volatility might simply be a flow-on from Wall Street.

Chart: Daily total returns – Oct 1, 2017 to Mar 29, 2018

Source: Thomson Reuters Data Stream

In general, there can be long-term shifts in the level of volatility or short-term clusters of volatility around some slow-moving long-term level. It is too early to tell for sure which type of volatility change we have just been experiencing. My ‘machine learning/AI volatility forecasting methodology’, which I have employed for more than 15 years, has an opinion. In the table, I reproduce forecasts of volatility and returns from my article six months ago, alongside the new estimates. The total returns forecasts are based on surveys of broker forecasts of dividends and earnings – and include an estimate for franking credits for the ASX 200.

Table: ASX 200, S&P 500 and portfolio annualised expectations (%)

Source: Thomson Reuters Datastream & Woodhall Investment Research

In spite of all of the political shenanigans, my volatility forecasts for the S&P 500 have risen, over a six-month period, only from 10.1 per cent to 11.6 per cent. Both are below the long-run average of 12.5 per cent. The ASX 200 volatility forecasts have increased from a very low 7.5 per cent to a low 9.5 per cent, which also compares favourably with its long-run average of 12.5 per cent. My ‘machine-learning volatility forecasting model’ dismisses recent behaviour as a short-term volatility cluster.

The signal from the noise

The returns forecasts for both markets have improved by about the same amount for the rolling 12-months-ahead horizon. The gains on the price index for the S&P 500 have been racing ahead of those for the ASX 200 but the gap narrows if you include dividends and franking credits. Our current forecasts of dividends (excluding franking credits) are 4.8 per cent for the ASX 200 and 2.1 per cent for the S&P 500. Only investors in the ASX 200 can receive franking credits, which amount to about 1.3 percentage points, bringing the so-called grossed-up yield on the ASX 200 to about 6.1 per cent.

Because the correlation between the total returns on the two indices is quite low – about 0.2 – there can be big gains from diversification. The maximum-Sharpe ratio portfolio, from a mean-variance analysis of the forecasts, produced a weighting of 60.5 per cent for the ASX 200 in October. The resulting expected total return and volatility for the portfolio were then 11.5 per cent and 6.7 per cent, respectively – assuming a constant US-Australian dollar exchange rate.

Over the last six months, the optimal weight for the ASX 200 has drifted down to 57.5 per cent from 60.5 per cent. The expected portfolio return has improved from 11.5 per cent to 13.5 per cent, with the expected portfolio volatility increasing from 6.7 per cent to 8.1 per cent.

Since the evolution of a strategic asset allocation involves attempting to strip out the signal from the noise, it is not too surprising to find the weight for the ASX 200 has moved only three percentage points.

Currency hedging

An investor must also make a strategic decision about how much of the currency exposure to hedge. Forecasting currencies is notoriously difficult. With our dollar somewhere around its average since the float in 1983, I prefer to hedge about half of the currency risk. I do this by holding equal amounts of IVV and IHVV, which are the ticker codes for two iShares exchange-traded funds listed on the ASX. IOZ is my current preferred (iShares) ETF for the ASX 200. If our dollar approaches the 70 cent level and below, I might increase the relative holding of the fully hedged IHVV ETF. Inversely, if our dollar heads back towards parity with the US dollar, I might decrease that relative exposure.

As it turned out, my October analysis would have produced an actual annualised return of 6.9 per cent (excluding franking credits) with a volatility of 11.9 per cent. Not quite what I predicted but February and March did throw up some left-of-field events. Over the last six months, IOZ, IVV and IHVV had realised volatilities of 10.1 per cent, 15.7 per cent and 18.8 per cent, respectively, so the portfolio’s realised volatility compares favourably. However, it should be noted that IOZ underperformed its benchmark by about two percentage points, while IVV exceeded its benchmark by about three percentage points. It is almost impossible to predict these temporary deviations of ETF returns from those of their benchmarks.

Leave a Comment

You must be logged in to post a comment.