When a surprise royal commission into the financial services sector was announced, commentators speculated that financial planning might escape the wrath of the commissioner. Their claims were largely based on the fact that planning has been subject to several inquiries in the last decade, which have led to several implemented reforms, including the Future of Financial Advice.

At the opening of the inquiry in Melbourne last month, however, assisting counsel Rowena Orr made it clear financial planning and the wealth industry were squarely in the frame as an “early focus” of the commission. Next month, the second round public hearings will focus on financial advice.

In the words of Orr at the initial public hearing: “Australians engage financial advisers to improve their financial position, to achieve their aspirations, and to plan for their future. Clients repose trust and confidence in their financial advisers. It is important that their trust and confidence is well placed.”

She acknowledged the numerous inquiries and reforms into financial advice, such as the 2009 Parliamentary Joint Committee on Corporations and the Financial Services Inquiry into Financial Products and Services in Australia, but said the commission provides the chance to assess the success of those changes.

The assisting counsel also made specific reference to the large players that license the bulk of financial planning practices in Australia. She noted that at the time of the inquiry’s report, there were about 18,000 financial advisers, about 8000 planning practices and 160 dealer groups, and the largest 20 dealer groups made up about half of the market. Further, 85 per cent of advisers were either employed by a product manufacturer directly or were operating under one as an authorised representative. Orr said she was seeking an update of the figures to confirm how the market has changed since the 2009 report.

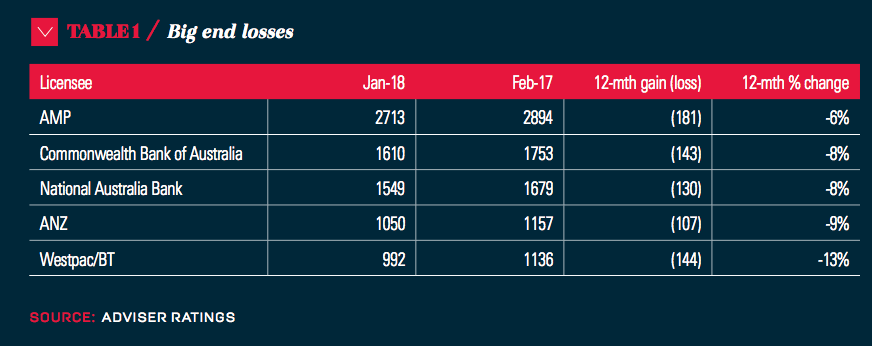

The big end of town

Analysis by Adviser Ratings, provided to Professional Planner, shows the big four banks, AMP and IOOF still have a major foothold, licensing 8900 of the advisers in the Australian market as of January 2018.

However, where those numbers have declined for each in the last 12 months, with the exception of IOOF, they’ve grown 2 per cent. Westpac/BT lost 13 per cent of its licensed advisers, ANZ lost 9 per cent, Commonwealth Bank and National Australia Bank each lost 8 per cent, while AMP lost 6 per cent.

The legitimacy of the large licensee model is under renewed scrutiny, thanks to a report the Australian Securities and Investments Commission released in January this year, which highlighted that bias for in-house investment products was rife, while a significant proportion of advice does not demonstrate compliance with best-interests duty.

The report in question, Financial advice: Vertically integrated institutions and conflicts of interest, looked at the approved product lists (APLs) of the two largest licensees from each of the top five institutions (AMP and the big banks).

It found that even though APLs had far more external products (79 per cent) than in-house products (21 per cent), more than two-thirds of client funds (68 per cent) were invested in in-house products. ASIC examined the investments over two periods – July 1, 2014 to February 28, 2015 and January 1, 2017 to March 31, 2017 – and did not find a significant difference between the time periods.

It found that in three-quarters of the files examined, the adviser had not demonstrated compliance with best-interests duty, particularly in relation to looking at the client’s existing financial products and individual circumstances. In 10 per cent of those files, ASIC determined the client would have been “significantly worse off” as a result. Reasons they would have been worse off included a loss of insurance benefits and an increase in ongoing fees.

The regulator’s report states: “The high level of non-compliant advice, combined with the high proportion of funds invested in in-house products, suggests that the advice licensees we reviewed may not be appropriately managing the conflict of interest associated with a vertically integrated business model.” It also notes, however, there have been some improvements in licensee monitoring of advice processes since post-FoFA surveillance began in 2013.

A question of licensing

The ASIC report has reignited questions about whether the institutional licensing model can effectively monitor financial advisers or if the template itself needs to be remade.

CoreData principal Andrew Inwood says the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry will impel the banks to shield their short-term revenue, which means their wealth arms will probably become collateral damage.

“The banks have to decide which part of the business they’re going to protect,” Inwood says. “They can’t protect everything…If you indulge in short-term thinking, wealth is not an important part of the business. They’re acting rationally in the face of that pressure.”

Inwood says when planners see that trend, they start to self-license. “That’s also a really rational response; they want to do the best job for their customer,” he says, which means moving away from the reputational damage and potentially curtailed product choice.

However, it does not guarantee the best outcome for the client, Inwood adds. “The economic risk to the customer starts to change. If you’re licensed by the big six, there’s a big asset behind you. You don’t have that if you’re [self-licensed].”

From the planner’s point of view, as self-licensing takes hold, the ecosystem will start to change, Inwood argues. Planners will have to start to look for new sources of revenue and that could mean, in effect, taking on the role of a fund manager, he says. Another implication for planners is the loss of the “network effect” the big six offer, which Inwood says will result in new players fostering a sense of community and collegiality within the advice community.

CoreData’s analysis shows the number of smaller licensees is indeed on the rise. Its analysis of ASIC data showed 460 new licensees were listed in 2016 and 2017, more than double the 219 in 2014 and 2015.

Meanwhile, a recent Professional Planner poll found close to half of respondents were either self-licensed or planning to become self-licensed (48 per cent at time of publication).

An ‘inevitable’ shift?

Paul Tynan, chief executive of Connect Financial Services Brokers, describes the shift to individual licensing as “inevitable” in an age when financial advice is becoming a profession and responsibility is shifting to the individual adviser. He says individual licensing would remove legacy problems, such as client ownership issues and APLs linked to institutions that might create biases.

Tynan also agrees the banks have a short-term horizon, which makes them a poor match for the long-term planning market; however, he notes that, from a practical point of view, having ASIC oversee six entities rather than thousands of individuals is certainly easier, which has led to the status quo remaining. What gets lost in this discussion, however, is the consumer.

“Individual licensing provides better transparency for the consumer,” Tynan says. “And when planners leave one of the big six, they change.”

He says he has seen dozens of planners become self-licensed and it renews their focus on doing what they entered planning to do – serve their clients’ best interests. “The biggest lie that’s been circulating is that it’s too hard to run your own licence,” he says.

Leave a Comment

You must be logged in to post a comment.