Super funds are on notice to think more carefully about how many financial services industry representative

bodies they support.

The regulator is focused on ensuring all expenditure is truly in members’ best interests, and some say fewer voices would communicate industry interests more clearly in Canberra. These factors point to a building case for mergers among some of the dozens of associations.

In December, the Australian Prudential Regulation Authority issued a warning to super funds that every dollar they spend must be carefully considered and justified as contributing to outcomes in their members’ best interests. This includes how much financial and other support is poured into the plethora of industry bodies and associations.

Professional Planner publisher Conexus Financial’s ‘back of the envelope’ calculations indicate more than $100 million a year of super fund members’ money is supporting industry associations.

APRA’s current discussion paper, Strengthening Superannuation Member Outcomes, notes super funds should “adopt sound governance and business management practices commensurate with community expectations”. The paper calls on funds to “move beyond a focus on just meeting minimum prudential requirements in order to meet these expectations”.

While the paper does not explicitly single out spending on representative bodies, it states that rigorous decision-making processes on all expenditures enable funds “to respond to these challenges without compromising the outcomes provided to their members”.

The Minister for Revenue and Financial Services, Kelly O’Dwyer, gives an even clearer signal, telling Conexus that “given the superannuation industry has the privilege of managing the compulsory deferred wages of millions of Australians, the government is concerned with ensuring that funds spend members’ money only in the best interests of their members, including where that expenditure is on involvement with industry representative bodies”.

Some argue the financial services sector is grossly over-represented by associations and representative bodies. There are more than 30 (see table, page 16). Some are focused on lobbying, others on continued education or professional networking.

All are vying for the money, time and attention of industry participants.

Tallying the cost

Putting a dollar value on the amount of members’ money that flows into supporting the industry body machine each year is tricky. Some bodies do not publicly disclose the relevant financial reporting; and some association membership fees are borne by funds, while others are paid by individuals.

Another complicating factor is the question of how far along the value chain to consider these costs. For instance, most retail wealth managers pay dues to the Financial Services Council, while their parent companies also fund the Australian Banking Association. Likewise, while the industry bodies servicing the advice sector were once quite detached from the super fund sector, this line is now blurred, as big funds now employ a number of advisers.

That said, analysis by Conexus Financial suggests it might be a conservative estimate to say at least $100 million a year is flowing into industry bodies servicing the superannuation industry.

The Association of Superannuation Funds of Australia (ASFA) pulled in $13.8 million last financial year, while the Financial Services Council (FSC) collected $8.7 million.

The Australian Institute of Superannuation Trustees reports on a calendar year basis, and its 2017 accounts were not yet available at the time of writing. However, AIST generated revenue of $9.1 million in 2016 and Conexus estimates it raised about $9.2 million in the year to December 31, 2017.

Industry Superannuation Australia (ISA) does not publicly release its financial reports but was forced to reveal to a Senate Economics Committee hearing in October that its revenue for the previous financial year was $21.7 million – a seemingly modest sum in the context of its massive ‘fox in the henhouse’ television campaign, launched in March 2017.

The Australian Council of Superannuation Investors (ACSI) reported $3.9 million in revenue in the financial year ended June 30, 2017, while the Fund Executives Association Ltd (FEAL) raised $900,000.

The Financial Planning Association (FPA) reported revenue of $13.5 million for the period. Meanwhile, the Self-Managed Super Fund Association (SMSF Association) collected $6.2 million and the Association of Financial Advisers (AFA) brought in $5.1 million.

Collectively, the nine associations listed above − ASFA, FSC, AIST, ISA, ACSI, FEAL, FPA, SMSF Association, and AFA – garnered about $82.9 million of support from the retirement industry last financial year. And that’s before we even consider membership dues paid to the other 20 or so industry bodies.

Less-visible costs

Of course, in the context of a $2.3 trillion superannuation industry, $100 million is a drop in the ocean. Leakage to industry association fees is absolutely dwarfed by the investment fees paid to fund managers. But just as funds have been forced to respond to pressure to bring down investment fees in recent years, they are now under increased pressure to reduce other business costs.

Rice Warner chief executive Michael Rice says that in addition to the direct cost of funding the associations, there are many “less visible add-on costs that arise”, including executive and staff time spent traveling to and attending multiple events throughout the year.

This is before even considering money and time dedicated to industry education, training and conferences produced by a number of commercial suppliers – including Conexus Financial, publisher of Professional Planner.

Doubling up

O’Dwyer’s words demand that super funds consider carefully which associations they back, how much they spend and why, and challenge the associations and industry bodies to prove their value and demonstrate they are worthy of continued support.

For years, there has been consistent debate within the industry about whether it can, and should, continue to support multiple bodies in light of the potential for duplication of activities – including multiple major events – and compromises to the industry’s advocacy and efforts to develop broadly supported policy proposals.

Former ASFA chief executive Pauline Vamos, who is now chief executive of governance research and engagement firm Regnan, says overlap of activities arises from the inevitable “scope creep” that occurs after a body is established.

“Having multiple groups that focus on specific and even time-limited issues can be very worthwhile,” Vamos says. “But once a body is established, it is often hard to close it − as we see with many committees, for example.”

Vamos says history has shown the super industry is in agreement on “about 90 per cent of issues”, but where there is not consensus “there is often violent disagreement”.

“So, let’s focus on the areas where we do agree. Have one body focus on getting the detail right on the issues we agree on,” she says. “More than once, I saw good policy debate and regulatory outcomes undermined because others around the table did not have the expertise in that area.”

Vamos says the super industry is potentially putting its social licence to operate at risk if it can’t demonstrate an ability to move quickly and cohesively to self-regulate and lift standards.

She points to the Insurance in Superannuation Voluntary Code of Practice, released late last year, as one example of a good initiative that simply took too long to execute, due in large part to the number of stakeholders involved.

“It [the code] took a lot longer than it should have,” she says. “We are not practised enough on establishing best-practice standards. There were also far too many derailments with SuperStream negotiations and the Standard Risk Measure. We could not even agree on the purpose of the system.

“I am not sure we understand what this makes us look like to external stakeholders, including the community. We are a long way off any kind of self- or co-regulation [and] I think this is something we should try to change.”

Contradictory voices

Another former head of a financial services industry association, who spoke to Conexus on condition of anonymity, recalls the process of lobbying the government as being like “taking a ticket at the deli counter”.

Ushered into the minister’s presence through one door as other association representatives left through another, association representatives didn’t know what had been said to the minister before they arrived, and didn’t know what would be said after they left. It was a disconcerting process and it was clear that the message an association was seeking to get across was at risk of being directly contradicted or diluted by myriad other voices clamouring for attention on the same issues.

“You have to rely on [a minister’s] ability to work through that,” the former association head says.

KPMG partner Paul Howes, a former Australian Workers Union national secretary and former AustralianSuper deputy chair, says the existence of multiple organisations representing different industry interests is “a reflection of how politicised superannuation has been since the day it was invented”.

But Howes says super funds, whether retail, industry or self-managed, have more issues where they’re united than where they disagree. Where there is unity – for example, on defining the purpose of superannuation – he says justifying the existence of multiple associations is difficult.

“In terms of policymakers, when I was an industry fund trustee and union leader and lobbied government on issues around superannuation,” Howes says, “one of the frustrations of the government, at that time, was the lack of a clear, united voice from the industry on these major reforms.

“ASFA does a very good job of trying to provide that [single] voice, but unfortunately the number of associations doesn’t necessarily benefit the debate as a whole.”

One senior political staffer, also speaking on condition of anonymity, agrees that it is a perennial source of frustration for elected representatives covering the super sector that there are so many different industry associations to hear from. This is complicated by the fact that some of the larger industry bodies are often hamstrung by internal conflicts: “Large bodies that incorporate several different voices in the industry, some of which are competing against each other, can end up being able to say nothing,” the staffer says.

The case for association rationalisation was highlighted in December last year, when Industry Funds Forum (IFF), a group representing the chief executives of 18 industry funds, merged into AIST.

IFF executive officer Chris Matthews tells Conexus Financial that he increasingly found himself attending the same meetings and events as the other association representatives, and it was “becoming a bit of a challenge” to differentiate IFF from other representative bodies.

He says IFF wanted to avoid duplicating work being done elsewhere. “We would often start a project, and then stop it because someone else was doing it,” Matthews explains.

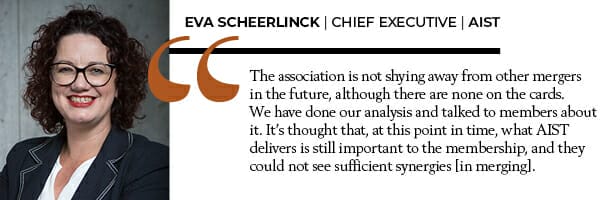

AIST chief executive Eva Scheerlinck says the institute is not shying away from other mergers in the future, although there are none on the cards.

“We have done our analysis and talked to members about it,” Scheerlinck says. “It’s thought that, at this point in time, what AIST delivers is still important to the membership, and they could not see sufficient synergies [in merging].”

Scheerlinck says associations must constantly reinvent themselves and stay relevant. She says AIST was created because “ASFA wasn’t necessarily delivering everything” that AIST’s members need. While ASFA seeks

to represent all APRA-regulated super funds, including the bank-owned and other retail funds, AIST solely represents the non-profit funds sector.

Competition for ideas

Many fund executives and staff perceive benefits in being active participants with more than one industry organisation.

First State Super chief executive Michael Dwyer sits on the boards of both FEAL and ASFA, for example; while HESTA chief executive Debby Blakey sits on the boards of FEAL and AIST.

Dwyer says his involvement in two associations allows him to make contributions to the industry in different ways. “As a director of ASFA, I can help shape thinking about the big issues for our industry at a macro level. Through FEAL, I can support the individual executives who are the current and emerging leaders of our industry,” he says.

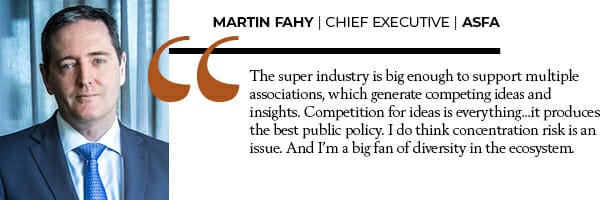

ASFA chief executive Martin Fahy says the super industry is big enough to support multiple associations, which generate competing ideas and insights.

“Competition for ideas is everything. It produces the best public policy,” Fahy says. “I do think concentration risk is an issue. And I’m a big fan of diversity in the ecosystem.”

In fact, he sees room for more associations across the wider financial services industry, saying that when it comes to representation of the banking sector, the Australian Banking Association “looks like a monopoly”.

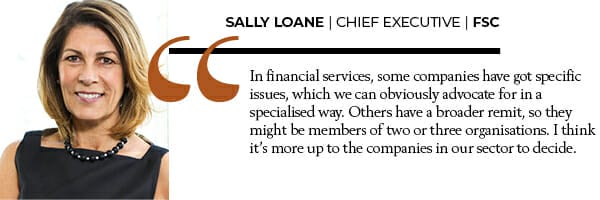

FSC chief executive Sally Loane says the financial services industry broadly, and the superannuation industry more specifically, is not unusual in supporting multiple associations.

In her previous role, Loane was director of media and public affairs for Coca-Cola Amatil and she notes there are eight organisations representing different interests within the beverages sector. Loane recalls an attempt to establish an association-of-associations for the beverages industry that failed because a single body could not represent

the interests of all participants. She believes the same is true in financial services.

“Some companies have got specific issues, which we can obviously advocate for in a specialised way,” Loane says. “Others have a broader remit, so they might be members of two or three organisations. I think it’s more up to the companies in our sector to decide.”

Niche remits

FEAL chief executive Joanna Davison says that as long as individual associations remain relevant to their respective members and are not duplicating the work of other associations, they will continue to receive support. But she does not discount the possibility of rationalisation in the future.

“[Would] it mean [our members] are all professionally developed and they’ve reached a point where they don’t need us? That would be good,” Davison says. “Maybe one day FEAL won’t be needed. But I don’t know when that will be –

I cannot foresee a time when we’re not.”

ACSI was established in the early 2000s to share among its members the cost of corporate governance as super fund investors began taking a more active, and activist, ownership approach to investments. At the time, associations did not adequately address these issues.

ACSI chief executive Louise Davidson says its mission is “so distinct from the purposes of those other organisations, it makes sense for it to be separate”.

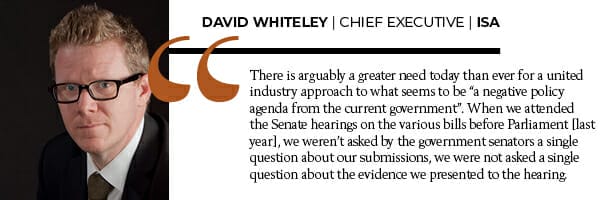

ISA chief executive David Whiteley says there is arguably a greater need today than ever for a united industry approach to what seems to be “a negative policy agenda from the current government”.

“When we attended the Senate hearings on the various bills before Parliament [last year], we weren’t asked by the government senators a single question about our submissions, we were not asked a single question about the evidence we presented to the hearing,” Whiteley says. “We were asked about our funding, about our staff numbers and about the cost of sponsoring Game of Thrones [on Foxtel].”

He says that on big-picture issues and those fundamental to the longevity of the system – such as increasing the super guarantee, ensuring the tax system is fair and equitable, and the evolution of retirement income products − the sector “tends to work quite well together, even where there are differences of opinion”.

Calls to consolidate

The question of whose interests are being served will continue as long as there are multiple associations and the potential for overlap in activities and the inefficient use of resources as a result.

Rice Warner’s Rice says he would support amalgamation among the major super industry associations, arguing multiplicity of bodies makes it “very difficult for the industry to lobby government”.

“If there were one voice in super, I think it would strengthen the industry in a number of ways,” he says.

Former ASFA chief Vamos says how to address this “has been discussed” within the industry.

“But we need an open and honest conversation on what we are trying to fix and agree on. “Are we about what is best for the community, or about what is best for us, or a particular sector?”

Leave a Comment

You must be logged in to post a comment.