A seismic shift is happening in the wealth-management industry. CoreData research shows adviser movement from the large institutions to independent licencees is real, accelerating and meaningful to the entire industry.

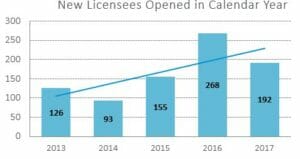

Based on ASIC data, a total of 219 new licensees were established in 2013 and 2014. In 2016 and 2017, however, the two-year total jumped to 460.

There are several drivers behind the shift to independence: closer scrutiny from ASIC; clearer adviser accountability; and the divestment from banks of their wealth businesses, because it’s just too hard.

Increased scrutiny distracting advisers

In January this year, the Australian Securities and Investments Commission released its report on vertical integration. Focusing only on the banks and AMP, it found that 75 per cent of super advice provided between 2014 and 2017 failed the best-interests duty obligations.

The increased scrutiny from ASIC on institutional advice practices is taking its toll on even the best of advisers. Understandably, institutional licensees are becoming increasingly risk averse and more demanding of their advisers’ standards of advice.

Sure, advisers working within independent practices need to comply with the same laws. But it’s easier in a structure that has fewer inherent conflicts, and when your licensee isn’t bearing down on your every move. You are set free to serve your clients’ needs and build your practice.

Buck stops with advisers

Today, working for an institutional licensee presents more risks to advisers than benefits. Banks have strong brands and customers are attracted to safety from a relationship with a large institution. But, as ASIC’s findings show, it’s hard for advisers to comply with the best-interests duty within the vertically integrated model. And that’s a problem for the licensee, but it’s also a problem for the individual adviser.

Advisers are coming to the realisation that the best-interests obligations sit with them, not their licensee. Even if they comply with their licensee’s business practices and their professional code of conduct, they can still breach the law. The buck stops with them.

Banks divesting from wealth

All four large banking institutions have been divesting from wealth management over the last couple of years. Since 2016, all the big banks have sold either their insurance arms, their investments businesses, or aligned dealer groups – in the case of ANZ, all three.

At the same time, industry super funds have been ramping up their advice businesses to retain funds under management.

Pretty soon, the vertical integration conversation and its inherent conflicts will feature new players. It will involve the super fund advisers, not the bank planners.

Other implications

The shift in the wealth-management sector will cause advisers to disperse, which will lead to a rethink of distribution strategies for product providers. Previously, salespeople were able to meet with a handful of institutional licensees and they were able to reach most advisers in the country. For fund managers, platforms and product providers, it’s only going to get harder.

In fact, for platforms and product providers, we’ll see the value proposition change. Increasingly, technology and the user experience, for both planners and customers, will become the differentiators.

The good news is that consumers will benefit. Sure, the advice independent planners provide may be different to what comes from those working at institutions, but that’s neither here nor there. In reality, the outcomes may or may not be better.

Of far greater consequence is the fact that more Australians will access advice. They’ll access it because they value independence. And even though the super funds are vertically integrated, they are still really well liked and trusted by the community.

So, more Australians will get the benefits of advice. They will engage more with their money, make better financial decisions, and have confidence that they can spend today and still be secure in the future.

Jason Andriessen is the director of consulting at CoreData Australia.

Leave a Comment

You must be logged in to post a comment.