Superannuation industry groups have proposed to Treasury a raft of policy changes to promote equity in retirement, including revisions to the assets test, gender gap reporting and compulsory super payments for parents on leave.

The Self Managed Super Fund Association has called on Treasury to repeal policy changes to the assets test for the age pension that kicked in a year ago, citing unintended consequences in a low-rate world.

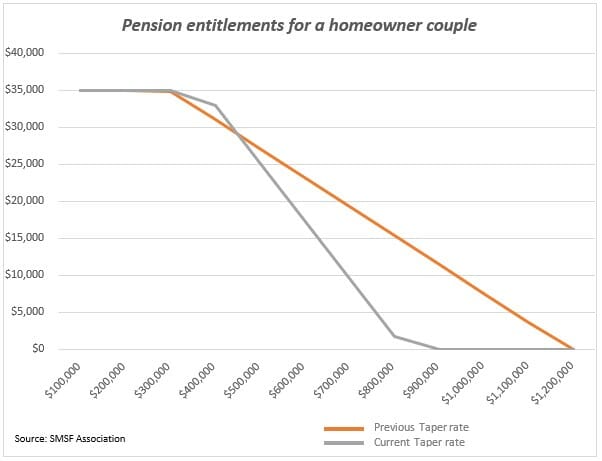

In a pre-budget submission to Treasury, the peak body for SMSFs stated that last year’s changes to the taper rate for the assets test disproportionately penalise middle-income earners with a superannuation balance between $500,000 and $800,000. According to the submission, the sharper taper rate, which falls off at an equivalent rate of 7.8 per cent, creates a “black hole”, meaning having assets within this range actually causes people to be worse off in terms of income.

This is an especially important issue, the report states, “in a low-interest rate and low-investment return environment.”

The rule changes have manifested as “an unfairly high effective marginal tax rate on superannuation assets that are in excess of the asset test free amount”, the submission states, discouraging middle-income earners from saving more within super for retirement.

As shown in the chart, the SMSFA cites the ‘homeowner couple’ taper rates as an example to illustrate how the current rates follow a much less gradual decline than the previous rates. Whilst those with low super balances and those with balances over the cut-out point have every reason to invest, pre-retirees have a far weaker incentive to do so if their balances are within or approaching this band.

The SMSFA is calling for a complete repeal of the assets test in its current form, in favour of a single deeming rate that presents “a more appropriate and simpler mechanism to integrate superannuation and age pension means testing”.An October 2017 report by the Association of Superannuation Funds of Australia (ASFA) states that the average superannuation balance at the time of retirement in 2015-16 was $270,710 for men and $157,050 for women.

“A deeming rate can be adjusted to accommodate current economic conditions (e.g., the current low-yield conditions confronting retirees) and can provide a far more suitable phase out rate than the assets test taper,” the submission states. “This would avoid the ‘black hole’ effect.”

The document also exhorts the government to increase the superannuation guarantee (SG) to 12 per cent sooner than the existing target date of 2025. The submission argues this is far too delayed and proposes bringing the timetable forward at least two years, as shown here:

July 1, 2019 – 10 per cent

July 1, 2020 – 10.5 per cent

July 1, 2021 – 11 per cent

July 1, 2022 – 11.5 per cent

July 1, 2023 – 12 per cent

“An increased SG rate will reduce the population’s reliance” on the age pension, the paper asserts. “We also note that during previous increases in the SG rate, there was no detrimental impact on the economy.”

This view was shared by the Australian Institute of Superannuation Trustees (AIST), which suggested in its own submission that increases to the SG recommence from July 1 this year. The AIST stated that increasing the rate to 10 per cent in 2018, and then in increments of 0.5 percentage points, would get the SG to 12 per cent in 2022.

This year’s pre-budget submissions showed a clear thematic push by industry-related entities for changes to the SG and more accommodation for the superannuation of women.

The AIST proposed several measures to improve super for women, including SG payments for paid parental leave and a publicly reported schedule of the disparity between men’s and women’s balances. Advocacy group Women in Super also suggested both these measures.

The Financial Planning Association backed SG payments on paid parental leave and on carers’ payments.

“This is consistent with the fact that employees are paid SG on other types of leave, such as sick leave, annual leave and long-service leave,” the FPA’s submission stated. “It would build a direct link in the system between payment for caring work and superannuation contributions.”

Another matter of concern for industry stakeholders was the application of the age pension.

The AIST called on Treasury to rule out the proposed increase in the pension’s qualifying age to 70, whilst National Seniors called for more flexibility for senior workers, such as increasing the Work Bonus to $10,000 a year to allow age pensioners to continue working.

Professional Planner’s annual Post Retirement Conference will be on March 21, 2018. The one-day event will help advisers transition their clients to retirement. To read more or to register, click here.

Leave a Comment

You must be logged in to post a comment.