Australian banks have had a dream run since the recession in the early ’90s, but with every interest-only loan that’s processed, the risks within Australia’s banking system increase.

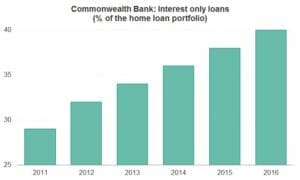

By way of example, 40 per cent of Commonwealth Bank’s current Australian loan book is interest-only. While the split between owner-occupiers and more speculative investment loans across CBA’s entire book is 63 per cent/33 per cent, Westpac has acknowledged that the majority of its interest-only loans are investment loans and we expect it’s no different for Commonwealth Bank.

With Commonwealth Bank’s investor loans as a proportion of total loans increasing from 31 per cent to 37 per cent since 2015, it’s easy to see why property prices are increasing rapidly, despite muted rental growth, and why many borrowers are ill prepared for falling property prices or higher interest rates.

If you believe the Reserve Bank of Australia can still lower rates to help protect borrowers, bear in mind that banks are already increasing rates to protect their margins and dividends. No doubt many borrowers are also bank shareholders relying on their dividends to repay risky investment loans, showing one of many dangerous circularities within Australia’s housing boom.

If and when problems eventually emerge, the RBA will probably lose further control of borrowing rates due to our big banks’ reliance on overseas wholesale funding. In the event of a crisis, foreign lenders that are vital to Australia’s prosperity will demand higher interest rates to protect themselves from a falling Australian dollar and the weak economy. Borrowing rates could easily increase despite any moves made by the RBA.

Looking offshore

For contrarian investors prepared to look beyond our sunny shores, there are banks listed abroad that might offer safer prospects in surprising places.

Say what you will about America’s recovery since the GFC, but it has been far superior to that of Europe. Barely a year ago, the US banks were a great opportunity. Their share prices declined rapidly as investors feared a slump in global growth. What the market was overlooking was the fact that their capital ratios had never been as high, and their loan books were shipshape, as risky borrowers have been unable to get loans since the GFC.

Litigation due to mis-sold mortgage securities prior to the GFC were also dealt with, risky trading operations had largely been closed and the regulators had succeeded in turning the banks into the safe, utility-like businesses that they should be. Historically cheap valuations measured by price-to-book ratios made them an exceptional opportunity.

In contrast, the European economy has been a basket case. Unemployment has remained stubbornly high due to austerity measures, with demoralising numbers of youth unemployed. Strict European Union rules preventing governments from financially supporting their banks have also delayed an economic recovery, until now.

Un nuovo corso

Late last year, Italy’s largest bank, UniCredit, completed a €13bn rights offering. On December 23, the Italian Government somewhat bent European Union rules and announced a €20 billion fund to help recapitalise the country’s weakest banks. Germany’s troubled Deutsche Bank, once the largest in the world measured by assets, has also announced an €8 billion rights issue.

Finally, Europe is getting serious about recapitalising banks to stimulate its economies. You can’t have weak banks and expect a strong economy, given their crucial role in extending credit to businesses and individuals.

Sticking with the Italian example, the country’s economy is showing signs of improvement, which is reflected in the recent share price performance of its banks. Non-performing loans are falling, and in many cases, they’re well covered by provisions. Ongoing cost cutting is also helping increase earnings.

Yet despite clear evidence that the European banking system is the safest it’s been in more than a decade, with many banks reporting increasing profits with sensible plans to raise return on equity over the next few years, many still trade at book value or less and offer attractive dividend yields. Should interest rates eventually increase, then bank share prices would probably emulate the rapid increases the US banks recently experienced.

European Union

The big difference between the US and European banks, however, is a potential break-up of the European Union. The recent vote for the status quo in the Netherlands’ general election supported our investment in ING Group, which is free of legacy-GFC issues and pays a 4.3 per cent dividend yield.

Under a worst-case scenario where the European Union dissolves, the respective governments will be free to support their banks. Longer term, it could also produce superior economic outcomes for many struggling countries. The successful recovery of Iceland has shown that starting from scratch can be a long-term strategy superior to prolonging the seemingly inevitable, like the economic tragedy that is Greece.

You’d think all Europe’s banks were a disaster from reading the media headlines. But if you analyse individual names, and their current profitability and prospects, you reach a much different conclusion.

With the Australian banking sector the riskiest it’s been in at least 27 years, Europe potentially in the sweet spot of an economic recovery, European banking profits increasing and set to benefit from any increase in interest rates – in contrast to Australia’s banks – now’s the time to consider your exposure to Australian housing. It’s been an amazing ride, but as a smart investor once told me, if you’re going to panic, panic early.

Nathan Bell is head of research at Peters MacGregor Capital Management.

Disclosure: Peters MacGregor Capital Management Limited holds a financial interest in ING Group through various mandates where it acts as investment manager.

Leave a Comment

You must be logged in to post a comment.