Much of the conversation about the superannuation reforms relates to reducing pension balances to a person’s transfer balance cap, resetting the capital gains tax cost base for investments and making last-minute contributions before the caps drop on

July 1. However, little genuine consideration has been given to which pensions should be fully or partially commuted to accumulation phase or withdrawn from the fund as lump sums.

Anyone with pensions valued at more than $1.6 million on June 30, 2017, will need to work out which pension or pensions should remain in retirement phase or be commuted in full or in part, so that total pension values are within the person’s transfer balance cap. This may sound relatively simple; however, for some it can have implications if a pension is intended to be paid to a particular dependant beneficiary or each pension consists of different taxable and tax-free components. For anyone 60 or over, considering the taxable and tax-free components may appear irrelevant, as most superannuation pensions they receive are not taxed. However, they do become important on the death of a fund member, if a benefit is paid to an adult child of the member who is at least 18 years old. In these cases, the taxable component of a death benefit paid to the adult child is taxed at 15 per cent, plus Medicare. Nevertheless, it is possible to reduce or avoid the amount of tax payable by the adult child with a bit of planning.

As a general rule, a person’s transfer balance cap from July 1, 2017, is $1.6 million, which is the maximum value of pensions that can be transferred to retirement phase after that time, including the value of pensions that were already in place at July 1, 2017. It is possible for a person to have a higher transfer balance cap if they receive a defined benefit pension, because of the restrictions placed on receiving lump-sum withdrawals. Defined benefit pensions include many public service pensions, lifetime and life expectancy pensions as well as market-linked income streams. Transition-to-retirement income streams (TRIS) are excluded from being measured against the $1.6 million transfer balance cap, as the income earned by the fund on investments that support a TRIS will be taxed at 15 per cent from July 1, 2017.

Let’s consider someone who is drawing one account-based pension from their fund, which has a balance of more than $1.6 million on June 30, 2017. In that case, the pension must be reduced, so that the balance of the pension is no more than $1.6 million by June 30, 2017. Any amount in excess of $1.6 million is required to be transferred to accumulation phase or withdrawn from the fund as a lump sum, otherwise a tax penalty will apply. The taxable and tax-free proportions of the pension remaining in accumulation phase will be the same as those that were calculated at the

time the pension commenced.

Case study

For someone drawing more than one account-based pension, the total value to be counted against their transfer balance cap on July 1, 2017, must be reduced to $1.6 million, otherwise the tax penalty will be imposed. For estate planning purposes, it is important to consider which pension or pensions should be retained or commuted, in full or in part, to reduce the value of amounts counted against the transfer balance cap to $1.6 million.

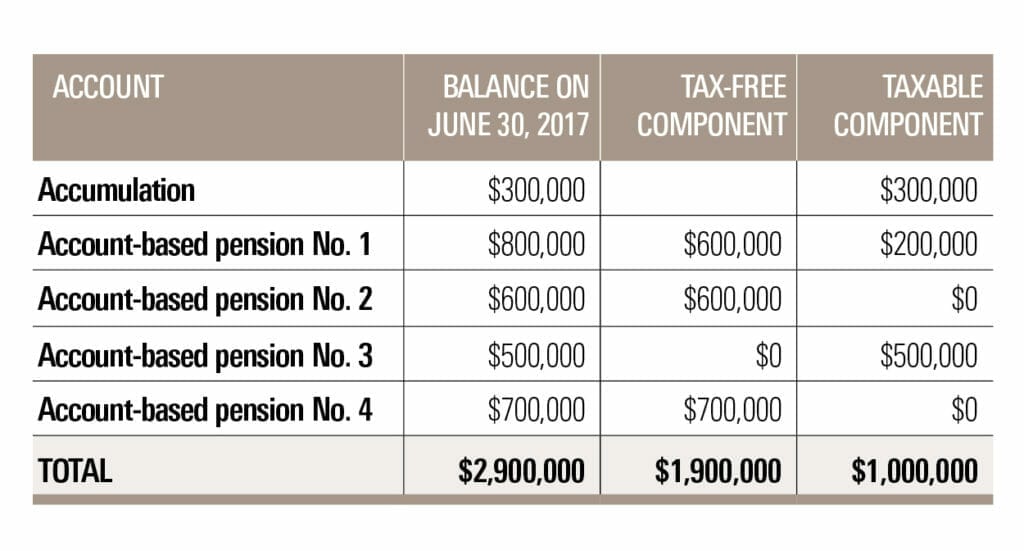

This can be illustrated in the case of Rod, who is 67, single, permanently retired, has an amount in accumulation phase and is drawing the following account-based pensions from his SMSF:

The total value of Rod’s account-based pensions is $2.6 million, which means he must reduce the balance of his pensions in retirement phase by $1 million to get the balances within the $1.6 million cap by July 1, 2017. If this does not take place, Rod will be subject to a tax penalty on the excess.

Let’s assume Rod decided to commute the pensions with the highest tax-free component to get the value of his pensions to $1.6 million. This would leave account-based pensions 1 and 4 in retirement phase and account-based pension 2 would be partially commuted, to leave a balance of $100,000. The remainder of account-based pension 2, $500,000, as well as account-based pension 3, would be commuted and transferred to accumulation phase or withdrawn from the fund as a lump sum.

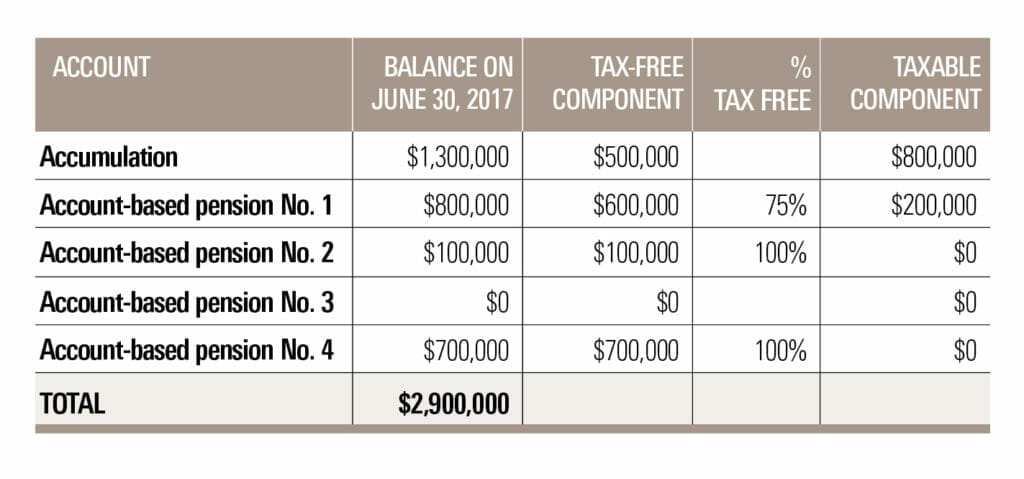

After commutation, Rod’s pension and accumulation accounts in the fund would be:

If Rod was to retain the pensions with a 100 per cent tax-free component, on his death, irrespective of the balance the pension may have grown to, they would continue to retain their tax-free component.

For example, if the value of account-based pension No. 4 was to increase to $1 million and was paid to his adult children, the whole amount received would be tax free. This would provide a much more tax-advantaged position than if account-based pension No. 4 was retained in retirement phase, because it consists of a 100 per cent taxable component. Any amount that may provide a death-benefit lump sum to an adult child would be taxed at 15 per cent plus Medicare.

In contrast, the tax position of amounts transferred to accumulation phase and paid out as lump sums determines the taxable and tax-free components in a different way to pensions. With pensions, the taxable and tax-free components are calculated as a proportion of the amount used to commence the pension and these proportions remain constant throughout the life of the pension. However, amounts in accumulation phase have the dollar amount of any tax-free component fixed and the taxable component is increased by investment earnings arising from the taxable and tax-free components.

Urban myths

In relation to transferring amounts from retirement phase to accumulation phase to stay within the $1.6 million transfer balance cap, a number of urban myths seem to have developed.

Urban myth 1: Amounts transferred from retirement phase to accumulation phase can’t be withdrawn from superannuation. This is incorrect. Any amount used to provide an account-based pension must have met a condition of release of retirement after reaching the person’s preservation age or age 65, whichever is earlier. Meeting either of these conditions of release means the benefits are totally non-preserved and can be withdrawn from superannuation any time.

Urban myth 2: A minimum percentage of the amount in accumulation phase must be withdrawn from the fund each year. This is incorrect. Only account-based pensions and transition-to-retirement pensions require a minimum set percentage to be paid each year. Where defined benefit pensions are paid from the fund the amount required to be paid annually is determined through an actuarial valuation.

Urban myth 3: Only one pension can be paid from retirement phase. This is incorrect, as there is no limit to the number of pensions that can be paid from the fund. There may be valid reasons for commencing a number of pensions, possibly due to the taxable and tax-free components of each pension.

Urban myth 4: Any pension balance in retirement phase must be reduced to $1.6 million each year. Again, this is incorrect. The value of the relevant pension measured against a person’s transfer balance cap occurs at the time an account-based pension commences from July 1, 2017, or on the amount supporting account-based pensions on June 30, 2017. Different rules apply to the valuation of defined benefit pensions that are based on the annual pension and a special valuation factor.

Urban myth 5: The amount a person is permitted to have in superannuation is limited to $1.6 million. There is no limit to the amount a person is permitted to accumulate in superannuation. However, the value of pensions measured against a person’s transfer balance cap for amounts in retirement phase is not permitted to exceed $1.6 million (which is subject to indexation).

Anyone who is likely to have more than $1.6 million in superannuation at June 30, 2017, needs to be aware of the changes to the contributions caps, the $1.6 million transfer balance cap, and resetting the CGT cost base. They also need to consider the possible estate planning impacts of retaining pensions in retirement phase and determine which should be fully or partially commuted to accumulation phase or drawn from the fund altogether. Of course, the urban myths that have grown up around the $1.6 million transfer balance cap and how amounts in accumulation phase are treated remain merely myths and should be ignored.

Leave a Comment

You must be logged in to post a comment.